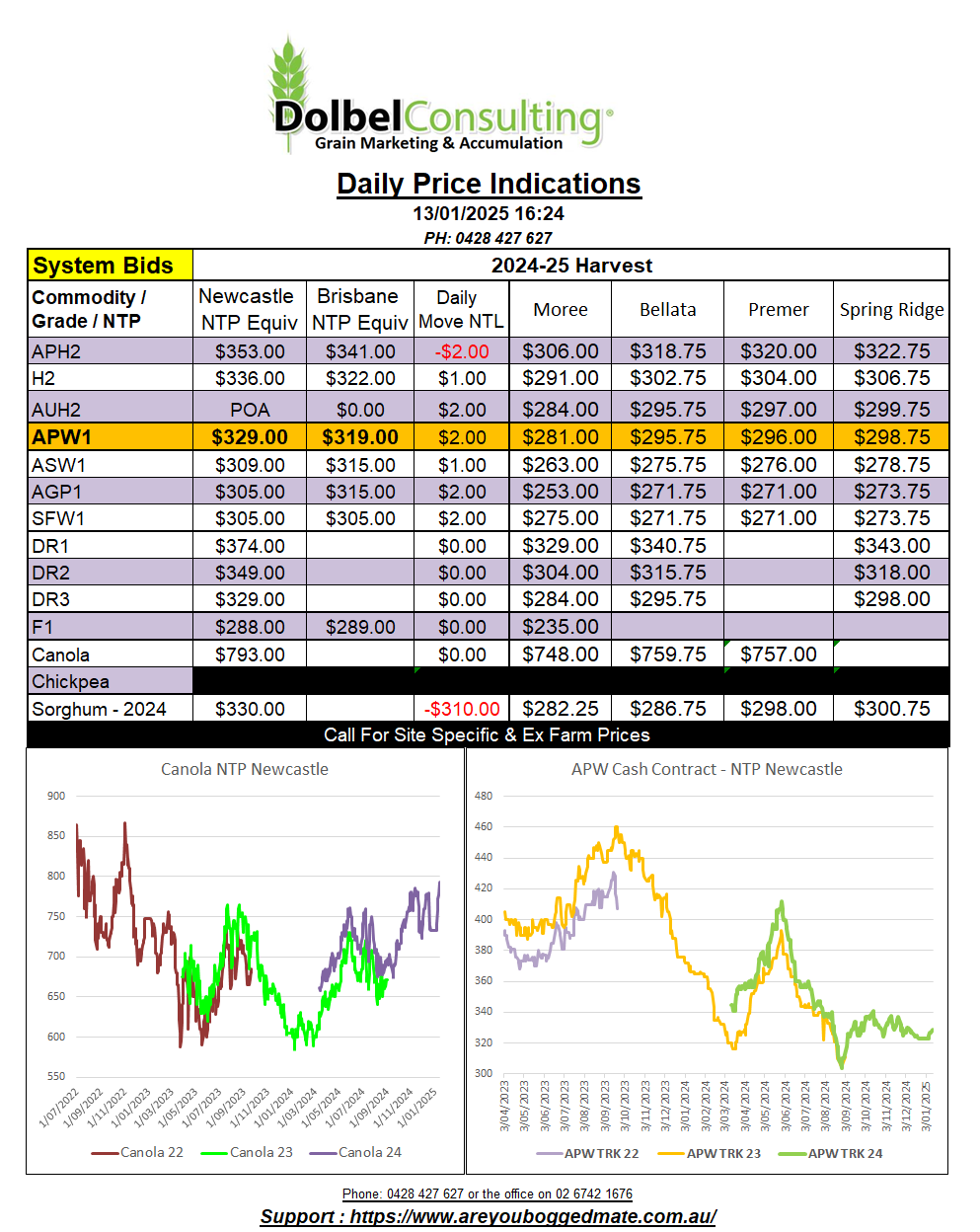

13/1/25 Prices

The USDA January World Ag Supply and Demand Estimates report, WASDE, held some surprises for the corn and soybean markets. Average US corn yield estimates were reduced to 179.3 bpa (11.254t/ha) that’s well below the average trade estimate of 182.7 bpa, prior to the reports release. The USDA also lowered demand but the net result was a slight reduction in carry out.

The reduction spurred the corn market life, nearby corn futures at Chicago jumping 14.5c/bu (AUD$9.28/t) by the close. The move higher was reserved for the old crop contracts though. New crop corn futures did close in the green, but only by 3.25c/bu in the December 25 slot.

The rally in corn helped drag US FOB sorghum higher and C&F China values. Combine these minor moves in US sorghum with the declining AUD and the FOB value for US sorghum rallied by roughly AUD$4.00 to AUD$4.50 / tonne when compared to yesterday FOB conversion.

The USDA also reduced soybean yields and world ending stocks. This lit a fire under the bean market at Chicago. The strength in soybeans rolled across both the Winnipeg canola contract and the Paris rapeseed contract, the later closing €9.75/t higher in the May25 slot. Winnipeg saw sharp gains, the Jan25 and March25 contracts closing C$16.70 higher, Jan26 also moved C$17.30 higher.

Wheat futures closed mixed, SRWW lower, while milling wheat’s were a smidge higher. There was no fires lit under wheat in this month WASDE. World production was increased 290kt to 793.24mt and lower estimates for usage saw the USDA increase carry out by 940kt to 258.82mt. Not what we need to see if we are targeting a sub 30% S:U ratio for price movement higher. The main move was in major exporters carry out. This was increased by 1.32mt, the exact opposite of what one would have liked to have seen. Russian exports were reduced 1mt but production was left unchanged, net result +1mt carryout.