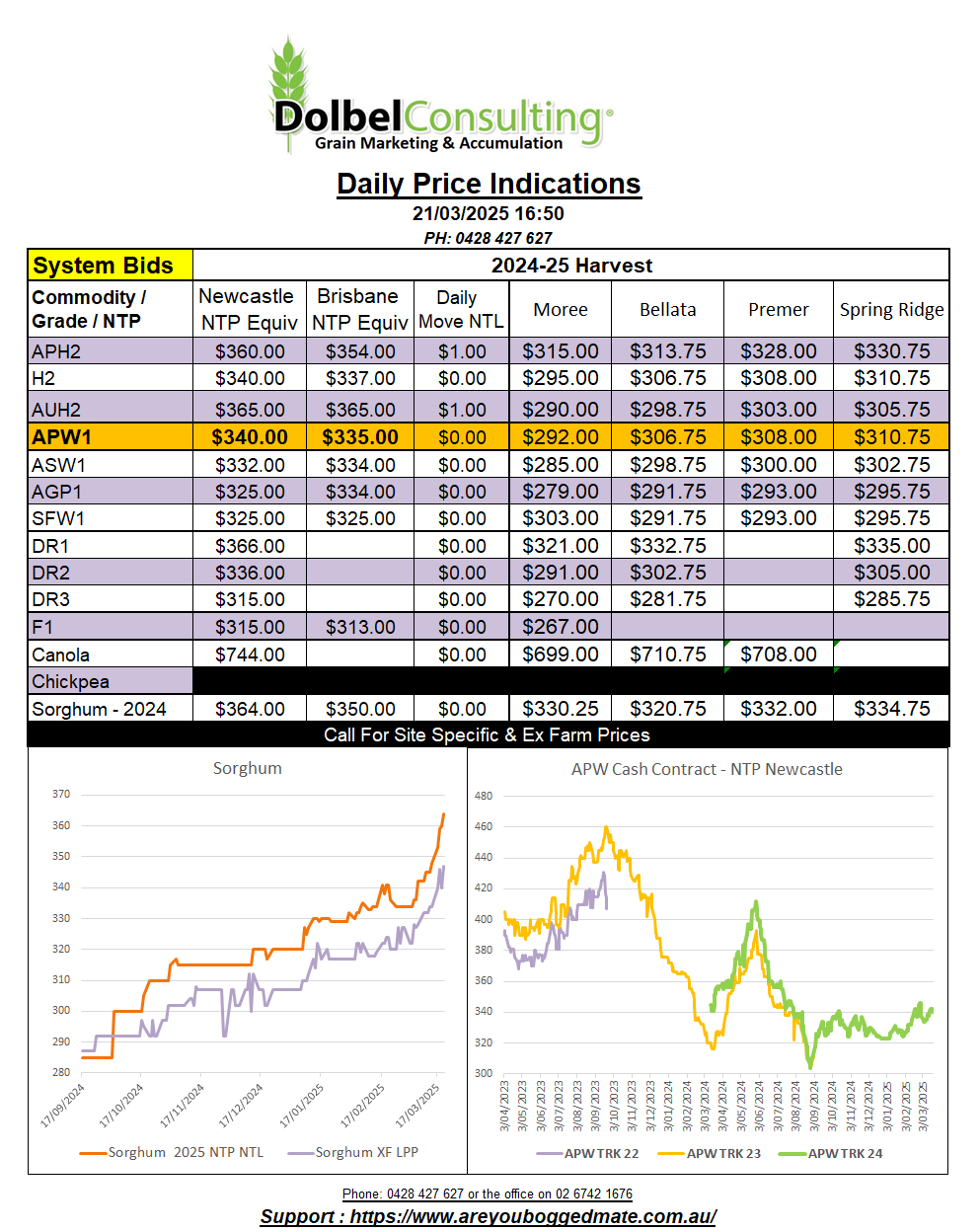

21/3/25 Prices

In global grain futures Chicago corn and soybeans closed a smidge higher. Nearby corn was the better of the mix, moves there rolling across to better cash values FOB for sorghum out of the Gulf too. Sorghum values C&F China, although a little higher, did not follow the move in US FOB values dollar for dollar.

Nearby Paris rapeseed gained €5.75 but looking through the outer month contact closes were mostly flat to lower, the Feb 26 slot shedding €1.50 / tonne. Winnipeg reversed the firmer trend it had set on M/T/W and shed values across all months, nearby back C$11.50 and the Jan25 slot closing C$10.30 / tonne lower. The firmer close in Chicago beans had little impact on a foundering Canadian canola market. Palm oil offered little influence, gaining just 3MYR/t (AUD$1.07/t) in the May slot.

The weaker AUD goes a long way to countering the push lower in nearby Chicago SRWW futures. The May SRWW slot shedding roughly AUD$3.64/t while the weaker dollar countered this by roughly AUD$2.35/tonne. Still a plausible net negative influence today.

Looking at world cash wheat values from the major exporters we see HRWW out of the US Pacific Northwest conversion, compared to yesterdays conversion, is back roughly AUD$2.37 / tonne, that’s taking the weaker AUD into account. The day to day change in the Canadian spring wheat conversion out of the PNW is roughly -AUD$0.78 / tonne. The biggest mover appears to be FOB Ukraine. The day to day conversion difference for Ukraine milling wheat is up roughly AUD$9.58/ t and the Russian milling wheat day to day conversion comparison is up just over four Aussie dollars.

French milling wheat values in AUD compared to yesterday are relatively flat while the Argie comparison is up AUD$1.40.

The US market appears to be discounting the winter kill scare, but weekly crop ratings as of April 7th will shed a better light on US wheat.