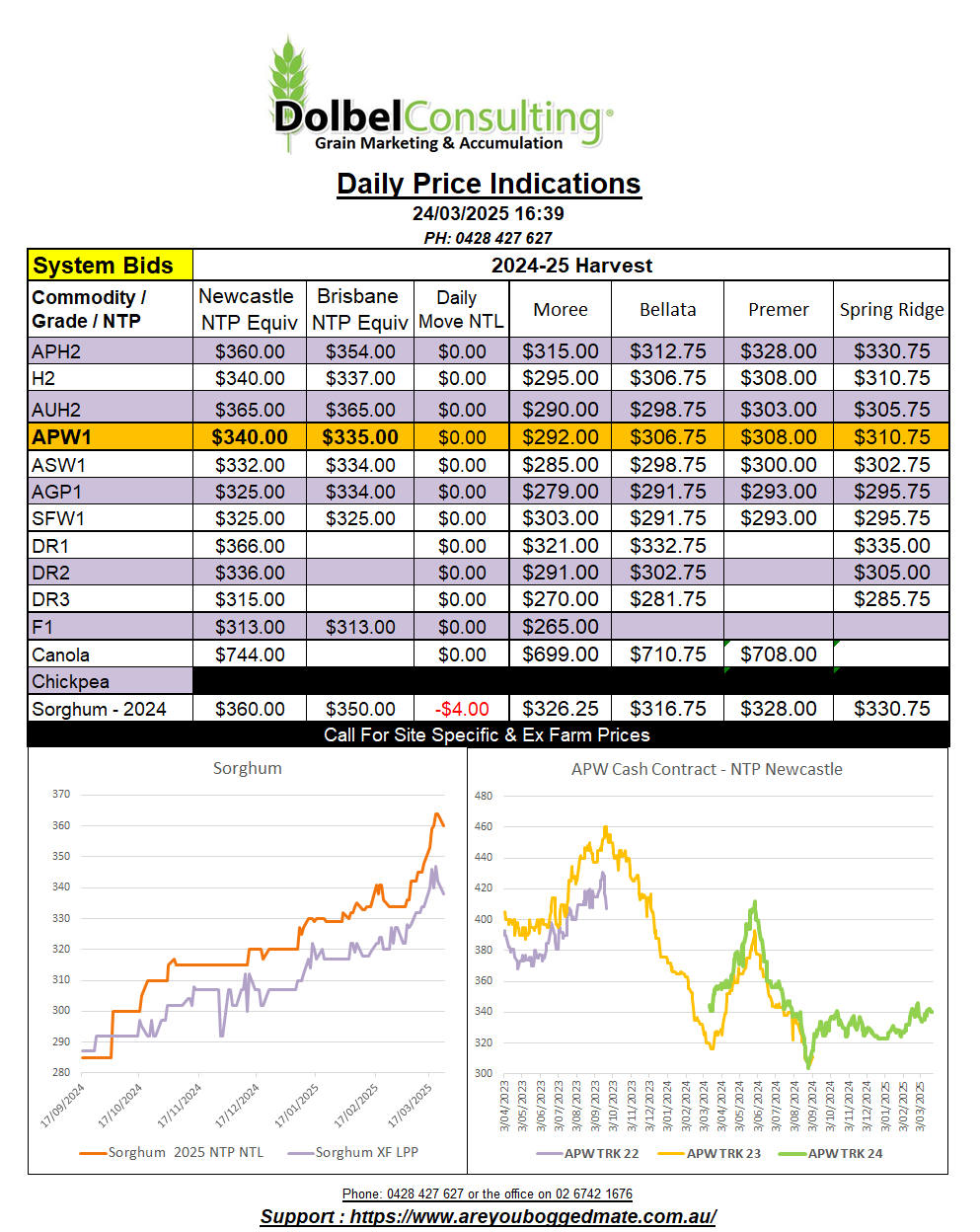

24/3/25 Prices

International grain futures consolidated last night, US wheat futures were generally flat to a smidge higher while corn and soybeans pushed lower. The move in soybeans weighed on Winnipeg canola, not that Winnipeg canola doesn’t have enough to worry about at the moment. The Jan26 slot for Winnipeg canola futures closed C$2.30 / tonne lower, Paris rapeseed futures in the Feb26 slot were back €0.25 / tonne. The weaker AUD was able to counter the push lower in most futures values last night.

World cash wheat values were mixed, but when comparing most of yesterdays conversions to an Asian consumer price and then back to an Aussie port equivalent with this mornings conversions, we see the AUD has countered much of the potential downside. This does expose the market to more potential downside if currency improves next week and grain values do not, but as for now the dollar is helping a great deal.

As it stands this morning, when considering the weaker AUD, most exporter wheat values are AUD$2.00 to AUD$3.00 higher when converting to USD C&F consumer and back to an AUD/ tonne price here.

Argentine sorghum was up US$5.00 / tonne. US / China tariffs helping both Argie and Aussie sorghum find technical support if not fundamental support. The AUD will play a nice roll in sorghum price conversions on Monday. US FOB values were mixed, some higher, some lower when converted. The Chinese index value was lower, even with the weaker AUD, but generally the sorghum / corn bundle is a smidge firmer, again mostly due to the decline in the AUD.

The UK based International Grains Council forecast world wheat ending stocks to fall to 259mt, a multi year low. This compares to 285mt in 22/23 if you need a benchmark. Production is high, estimated at 807mt, but this is beaten by demand at 813mt. Wheat stocks held by the major exporters is pegged at 61mt, just 1mt lower than 24/25. https://www.igc.int/en/markets/marketinfo-sd.aspx