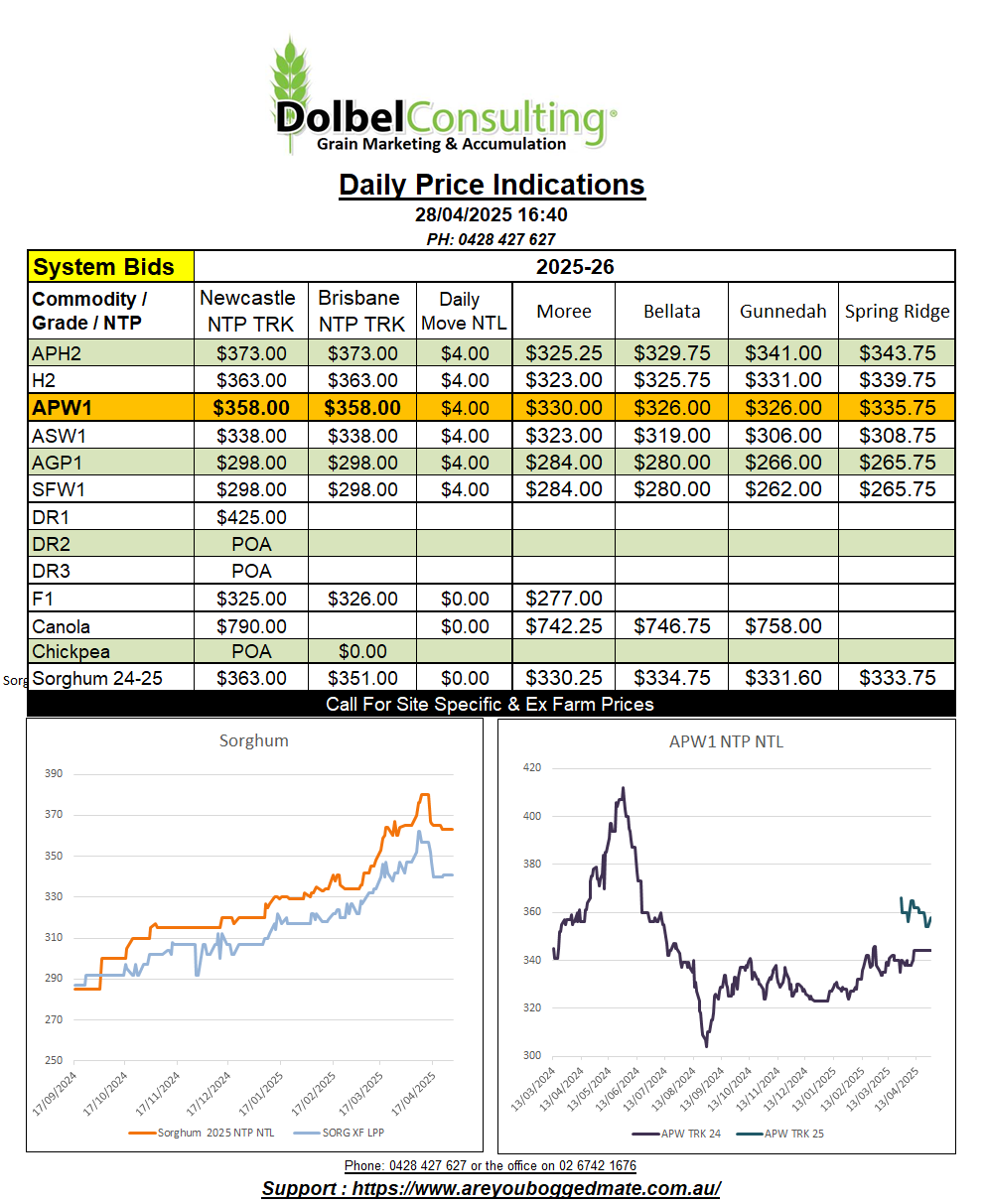

28/4/25 Prices

International futures and cash markets were generally sideways to a little firmer overnight. Outer month Chicago corn futures closed in the red, the consensus there being that US acres are more likely to increase than decrease.

Rainfall over the last 7 days in the US has been good across the corn belt, and the major soybean regions. The hard red winter wheat belt has also picked up some good moisture. Too much across some parts of eastern Oklahoma, Texas and SW Missouri though.

The US forecast is calling for more of the same in that area, which may result in some planting delays in the south for the summer crops. Sowing progress had been good in the south though, so there’s no real concern at the moment. Further rainfall across the HRWW belt should also improve the crop condition rating there as the wheat moves into heading and filling grain.

Conditions across the Canadian Prairies are mixed, many parts of southern Saskatchewan are seeing 200%-300% more rainfall than average. It sounds like a lot, but this time of year isn’t usually that wet, so the actual 14 day totals are only 20-30mm. Further towards central and northern Saskatchewan and northern Alberta, the main canola growing regions, is becoming much drier than average though. Probably worth keeping an eye on and may also help explain the slight uptick in Canadian canola values over the last week.

Europe is also a mixed bag, the north of France remains a little drier than average, while the SE of France is a little wetter, but not much. Germany is shaping up a lot better now after some nice rainfall over the last 7 days. SW Poland also picked up this rain, while the NW of Poland missed the bulk of it. Conditions across all of Ukraine have become hot and dry, very similar to the conditions now being experienced across the Volga Valley in Russia. This too is worth keeping an eye on over the next 30 days. Still in Russia we see the major spring wheat regions receiving good rainfall. Spring wheat usually makes up around 25-30% of the Russian wheat crop. Argentina continues to see good rainfall, a nice contrasts to the last couple of seasons for them.

As there were no domestic markets to report on yesterday, and Thursday’s markets were flat, we’ll play a game. This time of year I’m often asked what I think the value of new crop grains will be. It’s a big call, we don’t know the production potential of the northern hemisphere, and much of the winter crop in Australia is yet to make it out of a bag. All the same forecasting continues to be very important when deciding what to sow.

So without any major reason why I’ll tell you what I think, but in doing so I would like you to let me know what you think. To make it interesting I’ll put a $250 gift voucher at Enchanted On Conadilly on the line. The person who gets the aggregate value of these six commodities the closest to the actual aggregate value on the 1st of December wins. The person who gets the closest to each individual grade / commodity will also get a nice beverage delivered in time for Christmas.

Stu’s guesses: APW1 NTP NTL – $341, SFW1 XF C-LPP $322, BAR1 XF C-LPP $292, CAN1 XF C-LPP $723, CHKP1 XF C-LPP $720, DR1 XF C-LPP $420.

There you go, at this time of year it’s not much more than the roll of a dice, but it’s just game, a multi million dollar game for many.

World sorghum and corn values that funnel down into my sorghum price index show an avg AUD$1.15 / tonne net increase in value. The AUD has done nothing and international sorghum values are flat to a smidge firmer. Dalian corn futures and US FOB Gulf corn values are probably lending more support to this index than they should today. Stem nominations, plus estimates, still show bulk export demand at 640kt, gov total export projections are closer to 2.1mt.