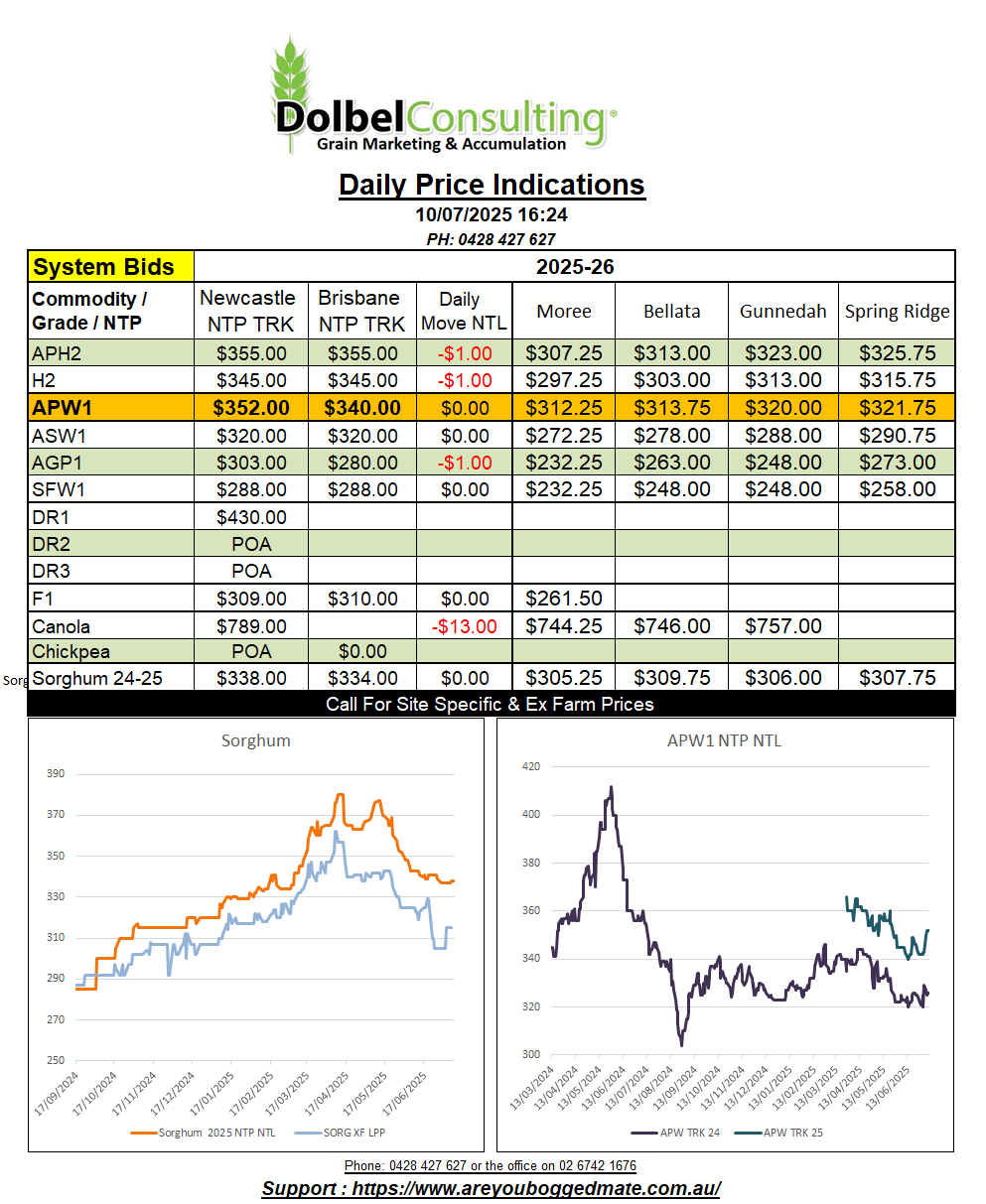

10/7/25 Prices

Looking around the world this morning there’s no big moves in anything that should have a major impact from a fundamental or cash price perspective. This leaves much of the impact on price today up to variations in local and cross currency exchange. The AUD is at 65.35 as I write, not a lot of variation from late yesterday. Over the last 12 hours the AUD set a low of 65.17 and a high of 65.45 not long after setting that sessions low. There’s not a lot of unannounced news to currently push the AUD one way or the other, apart from reactions to the red mans tariffs.

The RBA blew a few of the speculators out of the water leaving local rates unchanged earlier in the week. The punters, well those paid to print at least, appeared to be weighing in heavily on the side of a reduction in Aussie rates. This had the AUD down for a short while but it quickly recovered once the decision to hold rates was public.

This leaves demand the main driver of international values, particularly wheat, in the mid to long term. With winter wheat harvest progressing quickly all around the world, and 60% (52% 5 yr avg) of the North Dakota spring wheat crop now in head, there’s less and less from the production side of the fence to influence prices. Quality maybe, which may have a small impact on volume, but generally speaking the world is feeling fairly comfortable about wheat supply at present.

Demand changes from production issues with importers will be the key now, nothing new there.

Looking at production from the major importers will help us understand the potential change, if any, in import requirements, basic S&D stuff. Last year China imported roughly 4mt of wheat, well back on the 2023-24 tonnage of 13.64mt. In 23-24 China produced 136.59mt of wheat. Currently the USDA have them pegged at 140.1mt in 24-25, with imports of 6mt. Attached is the latest data from FAS. The data would tend to learn towards affirming the USDA expectations. A dry spring may have pruned yields in some Chinese provinces, but overall the crop should be OK. The Middle East + N.Africa + Nigeria demand is 58.33mt, +2.53mt on last year. SE Asian demand is 30.6mt up1.42mt on last year.