21/7/25 Prices

The international wheat market seems to be trying to set a seasonal low. With buyers like Algeria picking up over 1mt of wheat during the week it may be signalling that the demand side are sensing the seasonal low is close, or in, and it’s time to put the hand in the pocket.

The trade continue to suggest that with harvest progressing quickly past the 50% complete mark across northern hemisphere, that the price driver going forward will be from the demand side, not so much the production side.

I’m not 100% convinced this is all we have to drive prices just yet, but I agree it will be the biggest influence, not the only influence.

Argentina, Australia and Canada all have a long way to go before their production can be considered secured, or in the case of Canada quantified. These three countries are three of the 6 biggest wheat exporters in the world. Reductions to production in any of these three will reduce exportable stocks.

As a percentage of available export stocks a 5mt production reduction from these three could be as little as a 1.31% reduction of available export supplies from the major exporters. That’s not huge percentage of supply but may represent a fall in ending stocks of just under 10%, that’s worth taking note of.

This does tend to back up that demand is the key going forward, but the thing that may help trigger demand sooner rather than later, is a reduction to production in any of the top six exporters. Argentina and Australia having the longest to go before harvest.

Rainfall in Argentina over the past 14 days has been good, the major wheat regions have seen 15mm to 100mm, the Pampas region of BA seeing the heaviest falls and the better yielding regions of Cordoba and Santa Fe seeing very useful falls. Canada has also seen a few good falls over the last 14 days but reading grower comments on social media confirms that recent storms have been very hit and miss. Those picking up 20-30mm seeing their crops at least stabilising, while those missing a drink continue to watch their crops deteriorate. In cases getting walked out of the field as beef, not grain. Australia is a real mixed bag this year. Parts of SA and VIC continue to be dry, getting joined by parts of the CW of NSW, generally though, conditions are not dire.

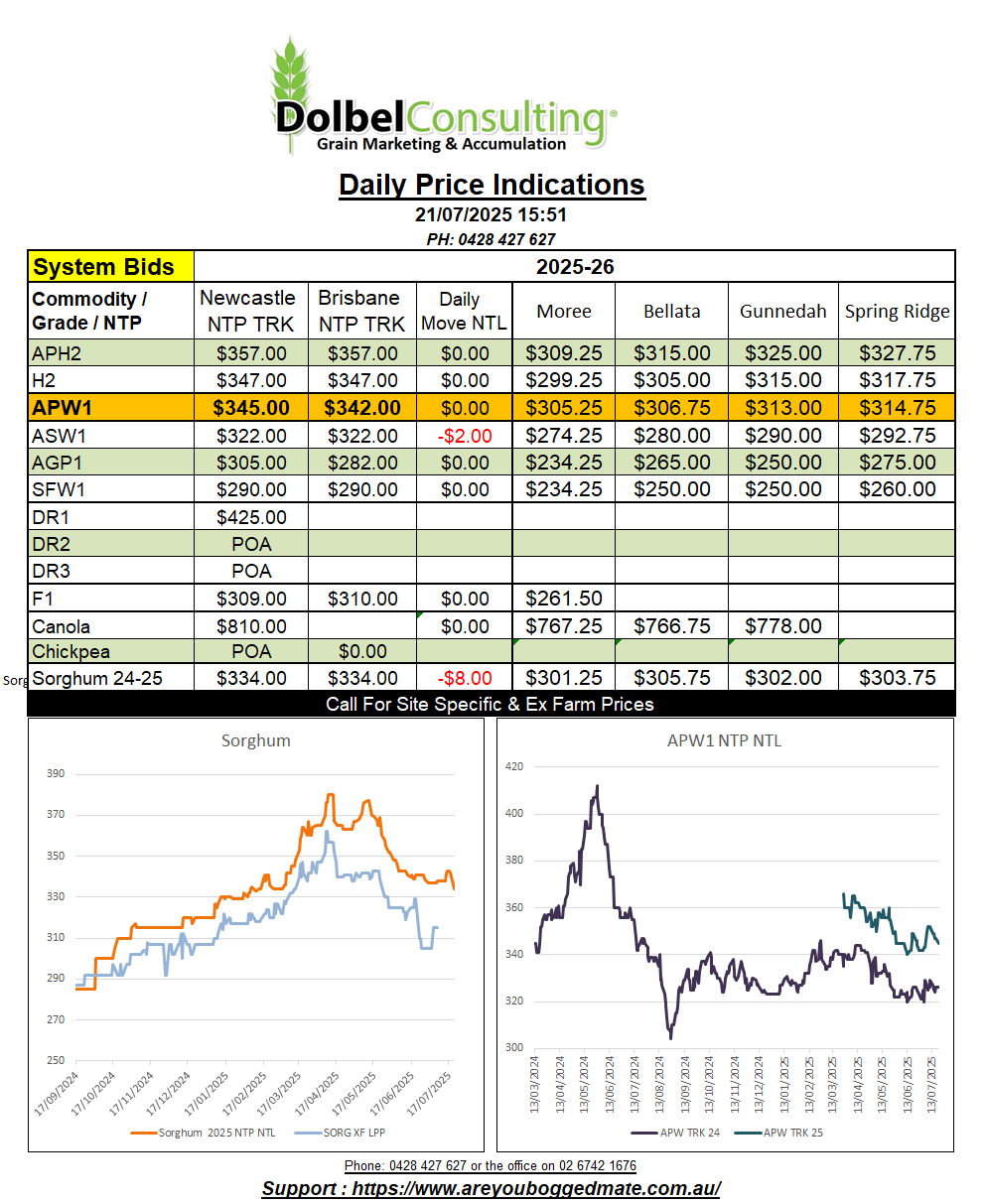

The sorghum market, particularly the track side, pushed a little lower Friday after recovering somewhat during the week. Track sorghum is suffering from a few different ailments at present. One being volume on the demand side. Most major players in the bulk export market executing from either NAT or Carrington, appear to be covered. There’s more volume on the sell side than the buy side from the trade too. One large exporter trying to swap out of system stock, converting it to ex farm stock when the money works.

The problem with system ownership continues to be how hard it is to execute from where the trade want it to be executed from and when it needs to be executed. This isn’t a new problem for the trade. Last year we saw some large export orders almost entirely filled by farm gate to port execution. This year was no different. This is leading to fewer major buyers willing to bid for track sorghum, not ideal, and may continue to be a feature of this market in the long term.

Sorghum on the track shed a dollar yesterday, Werris Creek silo bid $315 and offered at $320 from the grower, trading late in the day at the bid, the trade well aware of the lack of alternative buyers as positions for most buyers now appear to be covered.

The box trade were still there at $320 ex farm LPP, but were reluctant buyers at this number, limiting tonnage on the bid. If the Downs market softens, then execution of existing box orders may move to the Downs. I’m not 100% convinced this is a longer term move though, winter cereal harvest will start in QLD in 60 days or so.

New crop wheat basis to Chicago improved yesterday, absorbing the fall in US values. Overnight US futures moved higher, countering yesterdays lower close.