22/7/25 Prices

US, Canadian and Russian wheat values were generally lower last night. Cash prices from all three major exporters across most grades shed value. In the US and Canada the fall in cash values tracked similar moves lower in the futures markets. Spring wheat out of the Pacific Northwest slipped roughly AUD$4.00 to AUD$5.00 per tonne compared to yesterdays conversion comparison into the Asian markets. White wheat values were generally flat to firmer out of the PNW.

The USDA weekly crop progress report was out after the close in the futures market. Week on week the corn condition rating was unchanged at 56/18 = 74% G/E versus 57/17 = 74% G/E last week. Around 14% of the US corn crop has entered the dough stage.

The US national soybean condition rating was back 2pts to 68% G/E. Around 26% of the US bean crop is setting pods, bang on the average.

28% of the US sorghum crop is in head, 17% now colouring. 7% of the Kansas sorghum crop is in head. The condition rating for US sorghum declined 1pt week on week, slipping to 68% G/E. This is still very good and much of sorghum crop has ample, if not excessive moisture in some locations.

US winter wheat was 73% harvested, 1pt above the 5 year average harvest pace, just the very north and Nebraska lagging behind the average. Spring wheat was rated at 52% G/E, back 2pts on last weeks rating. This is still a good rating, and with 87% of the US spring wheat crop now in head it would take a serious weather event to downgrade their crop this year. The N.Dakota durum crop remains in very good condition, last week rated at 72% G/E.

Weekend storms across the Canadian Prairies have done more good than harm. This might be argued by some who did see the odd patch of hail across S.Saskatchewan take out some spring wheat and durum fields. The storms also produced falls of 10-40mm of rain with some heavier isolated falls. Although this rain is unlikely to add yield to crops it will stop any further decline.

Conditions in the US will become hot across the HRWW belt and the western corn belt this week. The first real heat this summer, but not concerning.

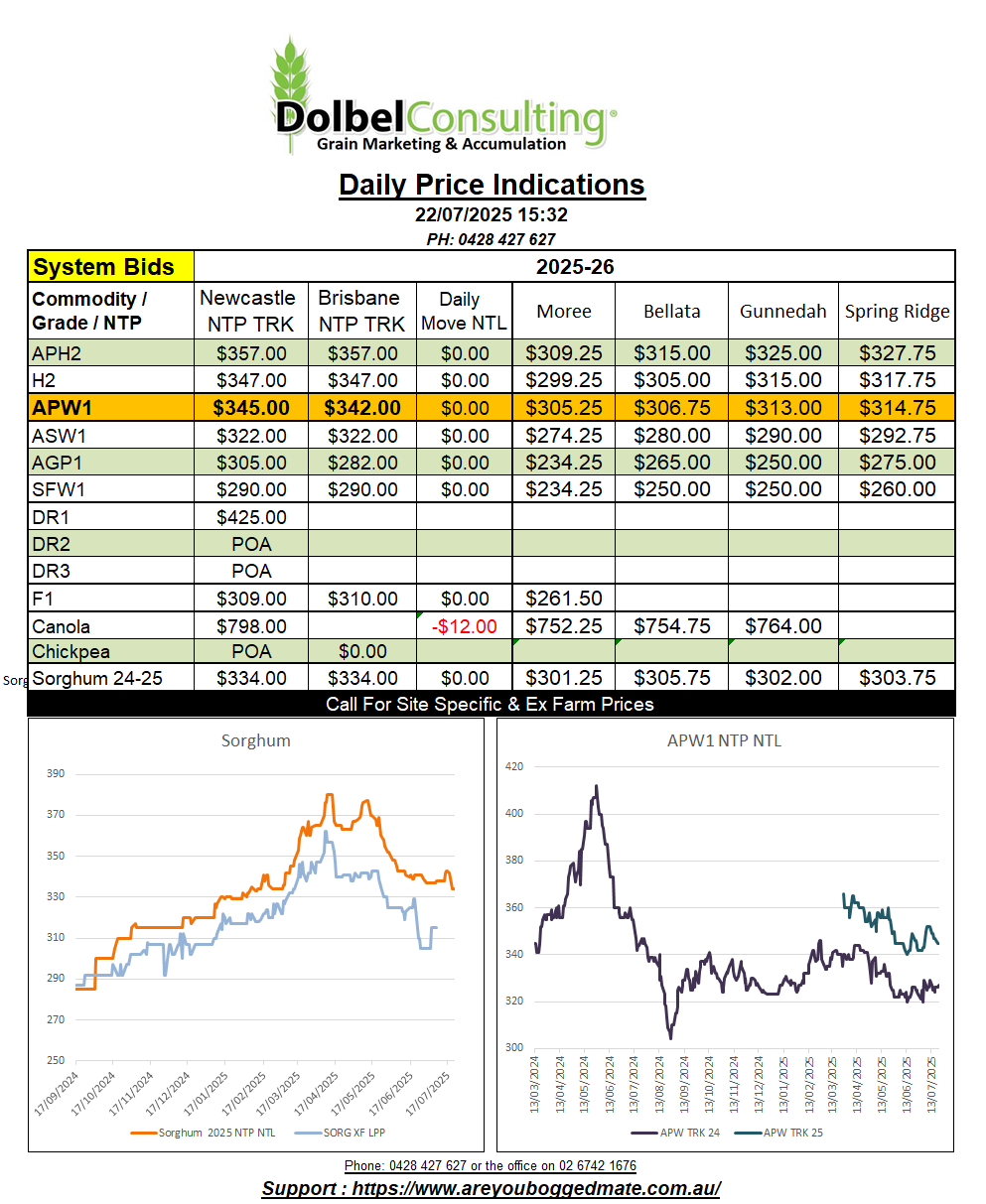

Local markets were dead. Sorghum took a nose dive on the track, falling from $315 DEL Werris Creek silo on Friday to just $307, down $8.00. Offers above the bid were rejected by the trade, of which there was only one trader left showing any interest in ownership of track sorghum.

The road market was bid into the Bathurst packer at $363 delivered. Roughly $320 ex farm LPP equivalent. Carrington by road found buying interest at $365 delivered August, $325 ex farm LPP equivalent.

There were no bids into the NAT port. Both CHS and Qube claiming to have completed their sorghum program for 2025, joining the likes of Bunge and a few of the smaller guys in closing their 2025 sorghum book.

New crop wheat basis was hit hard, down from +62c/bu on Friday to +42c/bu yesterday. The local market showed little interest in tracking the volatility in US wheat futures, as per the last 7 months.

New crop SFW1 values on the Downs was bid at $342 delivered, versus old crop at $339. The delivered market is not showing the spread the track is showing between old and new crop ($19.00). I guess this is because the grower is wearing the cost of carry in this instance, not getting charged by Graincorp. New crop bids for SFW1 on the LPP are harder to find as a generic bid, but work on a similar number to the Downs market for budgeting purposes.

The trade are actively seeking new crop chickpeas. Any wonder after Delhi values jumped $60.00 last week while local price moved just $35 higher. Overnight the Delhi market pushed higher by roughly AUD$10.00 per tonne. Taking the 10 days move to over AUD$70.00 / tonne.