23/7/25 Prices

Delhi chickpeas were firmer again, up 8Rs/Q, but the stronger AUD made short work of such a small move. Compared to yesterdays conversion to AUD / t, Delhi chickpeas are roughly AUD$5.28 / tonne lower this morning. There’s still a large degree of speculation over both Indian chickpea production and the total volume India is likely to need to import to meet any domestic short fall. This is putting pressure on neighboring countries like Pakistan and Bangladesh who will over top up supply from India or Australia.

Delhi mandi chickpeas have moved from a harvest low of 5450Rs/Q back in March to a high of 6340Rs/Q last night, a 16.3% move higher. Local bids for new crop chickpeas here in NNSW have moved from roughly AUD$730 per tonne XF LPP back in March to AUD$685 per tonne yesterday. Conversions of the Indian value to an XF LPP equivalent price tends to indicate a value of AUD$740 XF LPP is probably closer to the mark given the current Delhi price.

US wheat exports continue to beat trade estimates on a weekly basis. Although not long into the new marketing year, US export sales are setting a good pace. With the recent trade deals being announced for the Asian markets by the Trump administration, one can only assume that US demand will continue on at a brisk pace creating significant competition for Australian and Argentine wheat late in the year and throughout 2026. If deals are honored.

US sorghum into China is valued at something close to US$233 CiF, plus import duty of 10%, US$256 CiF. On the back of an envelope this will come back to an XF LPP price (not including trade margin) of something close to AUD$280 – $290 / tonne at the current AUD/USD exchange rate.

Cash values for wheat around the world last night were relatively flat to firmer. The stronger AUD took away a little of the upside potential leaving many conversions into the Asian consumer market unchanged in AUD terms XF LPP equivalent.

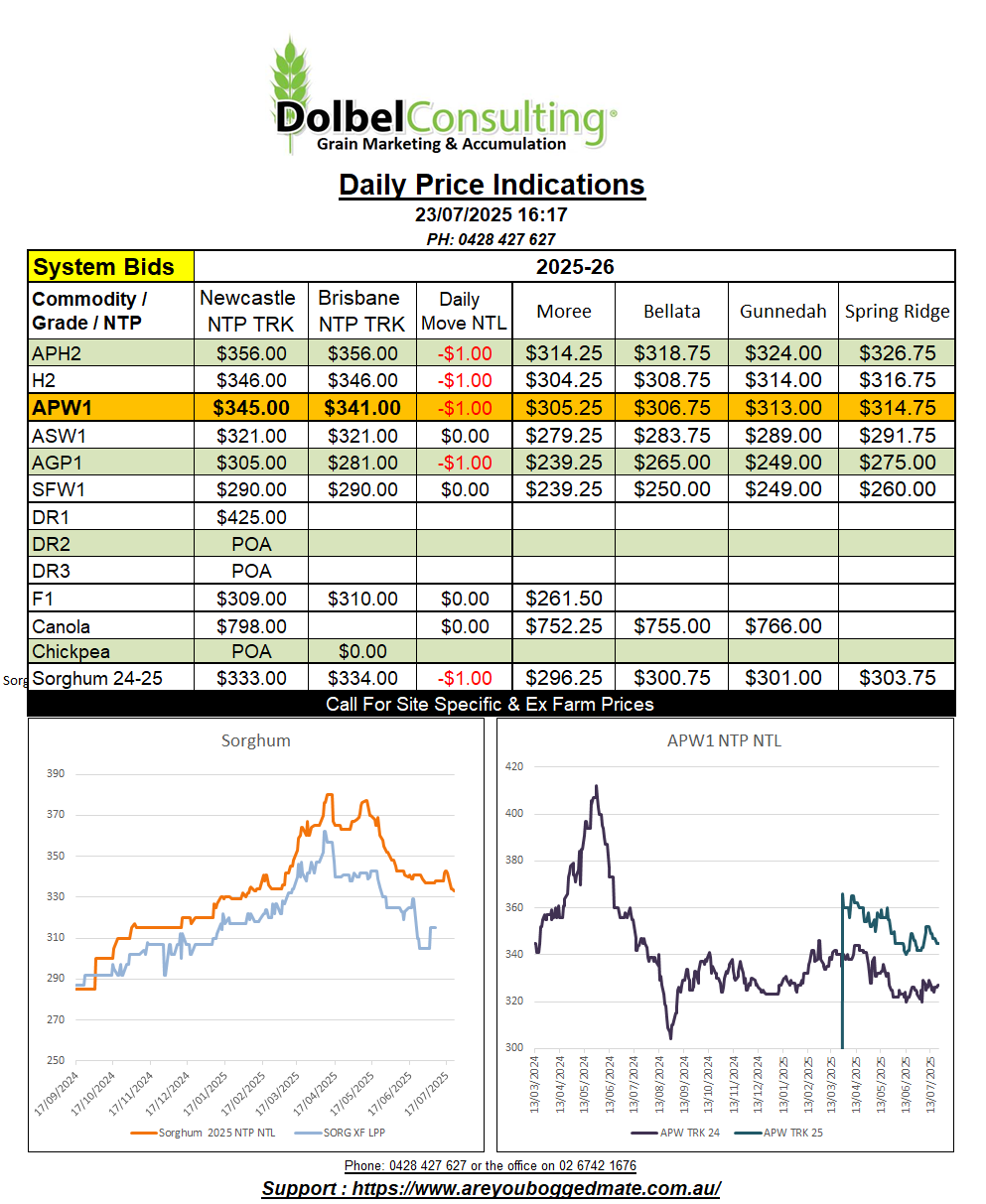

The sorghum market was sideways yesterday. There’s not much driving the sorghum price now. Box demand is about it, and it is only competing with the delivered port market because it has to. Carrington by road last traded at $365, the box market at $320 XF LPP, roughly $5.00 lower than the Carrington market. According to current box traders $320 is towards the high side, and unlikely to persist if the bulk port market was to fill or fail to bid moving forward. The current DCT market indicates sorghum values XF LPP may fall by $10 – $15 with little resistance, if the box market become the only option. A fall of this amount still fails to make sorghum look attractive to the local consumer market. This lack of attraction locally is two fold though, both price and sustainable availability making it unlikely. Once current demand is met sorghum, in any significant volume, will become hard to move, as it usually is in August.

New crop wheat basis to Chicago wheat futures improved, jumping from +42c/bu to +48c/bu, nothing to write home about but signalling a flat market locally. New crop H2 wheat will move into the Asian market for something close to US$275 CiF. HRWW out of the US PNW would land in the same market for something close to US$263. A spread of US$12 isn’t a major hurdle when considering the characteristics of the two types of wheat. What is a concern are the trade deals the US is currently negotiating with the Asian markets. The thing to watch over the next couple of years is if these trade deals are honored or if they need to be subsidised by the US to make them honored. In the meantime with have Russian wheat potentially priced US$10.00 to US$15.00 lower that US wheat into the Asian market to compete with. The international market has a “race to the bottom” (if not there now) feel about it in the short to mid term. A put option ???