24/7/25 Prices

The headlines get a little over the top these days. The first one I read this morning was “scorching weather fails to heat up grain prices”. US centric obviously. I remember in the past hot weather wasn’t even rated unless it sat in the low 40c for a week or more. The US hard red wheat belt, not the central corn belt, has seen a couple of hot days this week, actually this summer. Temperatures across Kansas climbed into the low 40s for a day of two this week. The punters got a little pumped up, thinking maybe the heat will damage this corn crop that’s been sitting in mud for a few weeks.

But here we are, the scorching weather failed to kill a corn crop that’s been rated 72% G/E…… 72% Good / Excellent, that’s a bloody good corn crop. So forgive my cynicism somewhat for not getting on board the climate induced doomsday wagon this time around. If you are currently long US corn, you may need a little more than a couple of hot days south of the corn belt to square your book up.

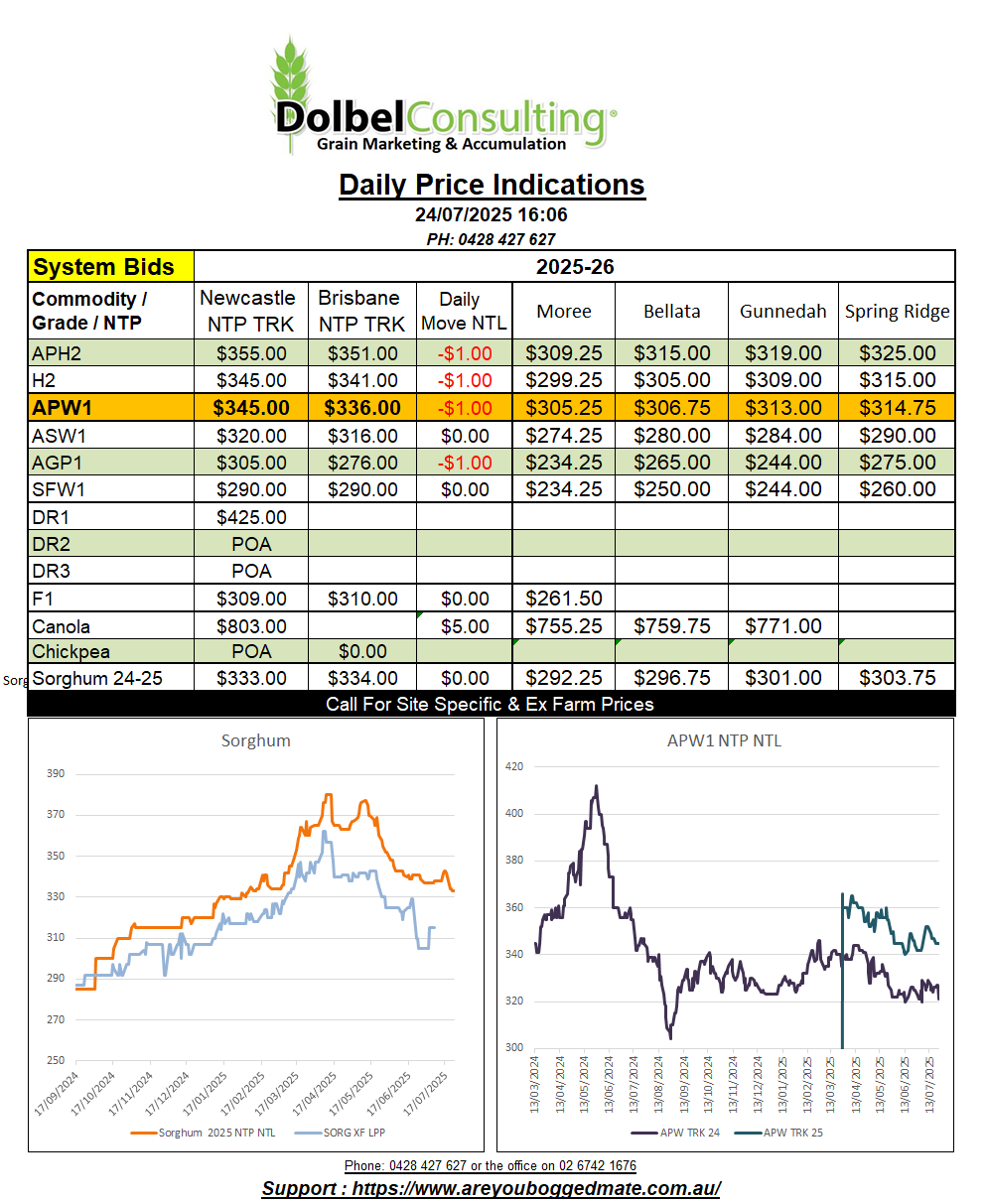

International futures markets are a sea of red this morning (bar canola / rapeseed). Combine this with an Aussie dollar above 66 for the first time in 9 months and we have the potential to become a little softer here today. Global cash wheat conversion values were lower day to day. New crop out of Russia into the Asian markets saw a conversion comparison reduction of roughly AUD$1.03/tonne. US HRWW out of the Pacific Northwest was back AUD$7.69/t compared to yesterdays conversion. This fall makes US wheat roughly US$9.00 above a comparable Russian wheat into the Asian market. Good luck with those trade deals Donald. With talk of a cease fire between Ukraine and Russia I can only see that part of the world becoming more competitive in the mid to long term, if the cease fire occurs / persists.

France and Germany have both raised their wheat production estimates, not by much, and French production still remains below the 6 year average, but at 21.6mt for Germany and 33.4mt for France, production is much better than last year. France seems to have pulled off a good crop in a dry year ??

Currency might be a bit of an issue today. It’s the first time the AUD has nudged above 66 US cents since November last year. The move in the AUD is equivalent to a US cents per bushel move of -4c. Add that negativity to the decline in Chicago Dec futures of -8.25c/bu and the net loss is about AUD$7.34 / tonne. There’s a good chance that we’ll see basis improve and absorb a slice of the potential downside in wheat, but the international trend is lower at present. A combination of harvest pressure and improving weather conditions for some of the major spring wheat producers. Locally we are also looking down the barrel of another good year in NNSW / SQLD. This will continue to keep a lid on both prices and consumer demand.

This raises the forward contract question now that production here is looking a little more secure. The local merchants have not reflected the volatility in futures, thus we’ve seen very little incentive to lock in forward contracts this year and, if they continue down this path, we probably won’t see a lot of opportunity going forward. This leaves the producer as a price taker come harvest. We saw how that panned out in 2024, first in best dressed. I’m not predicting a date to date repeat of 2024, but the chance of a significant rally on the back of something happening in the northern hemisphere, other than war or sanctions, is a rapidly decreasing possibility. We also have a long way to go here. The chance of a localised issue, flood, frost, heat, can present regional opportunities. We may need to take a short term cash, long term store and sell strategy for the coming crop.

This may just be one year where we really miss the old pooling system. Not that we can’t duplicate that system to some extent using OTC hedge products and scaling cash sales, but the ease of access will be missed.

The WA wheat fields are seeing a few showers today, Narrogin has picked up 13mm since 9am yesterday, taking the 7 days total there to 31mm. Katanning 7mm (22mm), Cunderdin 3mm (10mm), Merredin 4mm (12mm), Dalwallinu 13mm (17mm), Morowa 11mm (16mm).

A low cell (999hPa) off the coast of Albany WA is producing a front that stretches as far north as Exmouth. The low cell will move across the Bight quickly, reaching the SA croplands around Friday morning. The front will by then extend as far north as Katherine in the Northern Territory. By Friday evening the front will be located along the NSW / SA border and the low cell roughly over Adelaide and still decreasing in pressure. By the time the low cell hits Bass Straight on Saturday evening it will be as low as 995hPa and tracking basically due south from there.

The front will bring very strong winds to much of Victoria and the Riverina on Friday night and Saturday. Winds on Sunday will still be strong but should start to die down across the inland by the afternoon.

Rainfall will accompany the front, moving across the NWSP early Saturday morning and producing falls for much of the day and into Sunday morning. Here on the LPP we should see the arrival of the front around 2am-4am on Saturday morning, in the form of a thunder storm further north. There’s a good chance we’ll see 10mm before sunrise, rain potentially becoming heavier before 9am. Showers are expected to ease and contract east Saturday afternoon.