6/8/25 Prices

US wheat futures were hammered again on Tuesday. Technical sellers gained traction and the slippery slope got wetter. HRWW futures were the hardest hit, shedding 12.25c/bu (AUD$6.95/t). The fall in futures was reflected at the port. Values out of the Pacific Northwest for HRWW were also lower, shedding AUD$7.20 / tonne compared to yesterday’s conversion. The higher grade spring wheat from both the US and Canada fared a little better than the 11.5% protein wheat. Canadian 1CWRS13.5 wheat fell by CAD$1.48/t XF SE Saskatchewan on average, now valued at roughly CAD$247.26/t XF. At the port Canadian spring wheat slipped AUD$1.98/t compared to yesterdays conversion.

The fall in US HRWW values narrowed the gap between US and Russian wheat into the Asian market. In order for Trump to say his trade negotiations were a success US wheat will still need to be competitive into these markets. Russian wheat will simply compete on price, it’s that simple. I can only see one loser in all of this trade / tariffs debacle, the American farmer, and to a lesser extent the Australian farmer, the traditional supplier of this market in the northern hemisphere off season.

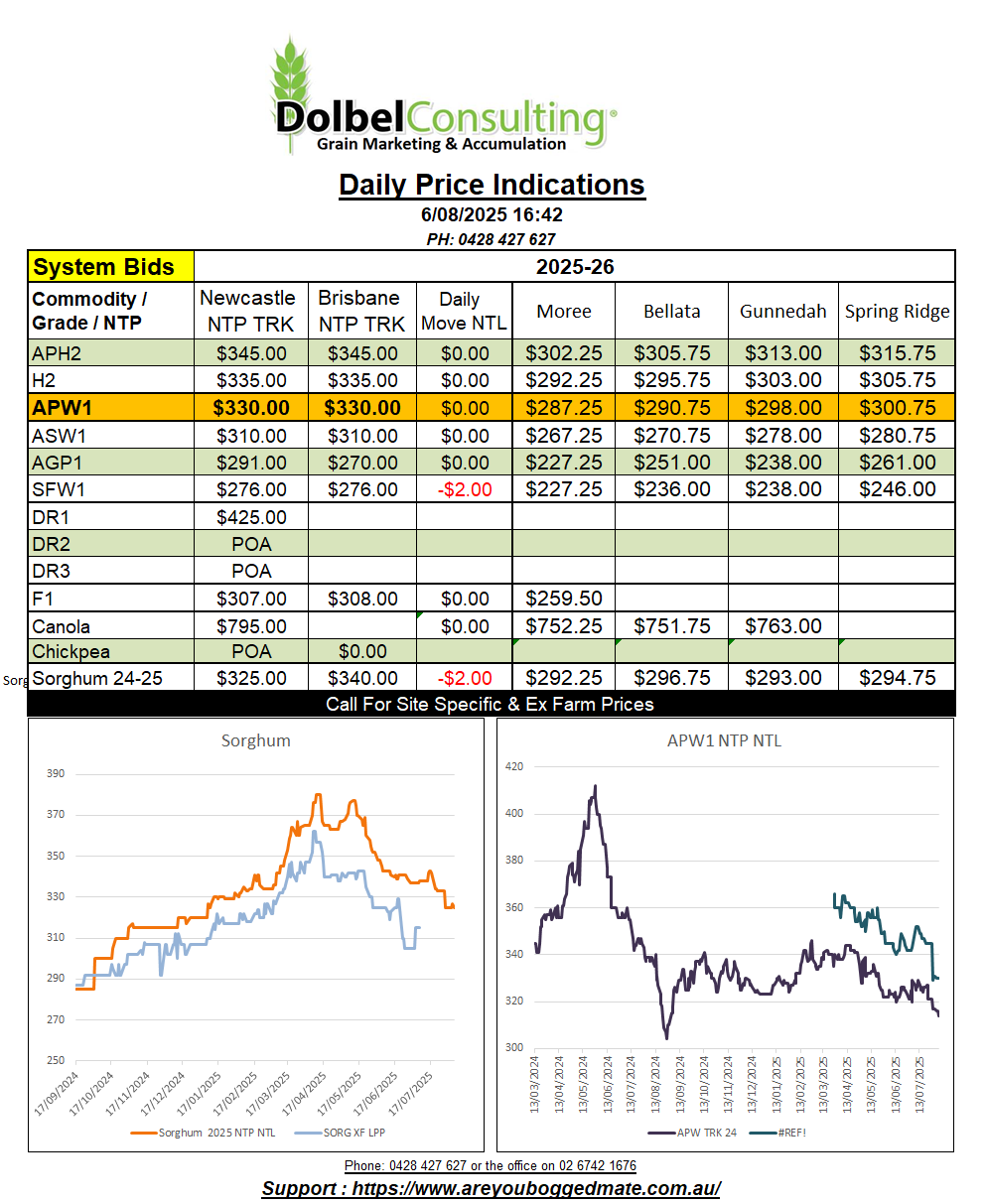

It is interesting to compare prime hard wheat to US / Canadian spring wheat into the Japanese market. New crop APH is bid at roughly AUD$345 NTP NTL. US and Canadian values convert back to an equivalent Newcastle port comparison of something closer to AUD$350 to AUD$360 NTP NTL. During the dry spell in Canada and the wet spell in the US spring wheat region, Australian prime hard spreads never increased, thus multi grade values here are still very competitive internationally. We’ll see how long that lasts once the Russian spring wheat harvest gets under way.

Russian milling wheat values have increased a little at the local level. Poor prices were met with significant grower resistance over the last month. Another signal that the bottom may be in. The strong export pace out of the US is another good sign, but the punters seem hell bent on going lower in futures.

Local markets remain very quiet. The trade continue to look for old crop milling wheat, which is in turn then bid poorly ?. Yesterday saw AUH2 offered at $315 XF Narrabri area against a trade bid at $299. AUH2 topped out in February at roughly $315 XF Narrabri area. Since February track APW has fallen $30.00 / tonne. To see a difference of $16 between Feb and yesterday for AUH2 wasn’t a bad result, but from a carry perspective it’s still a bitter pill to swallow.

The trade have suffered through this scenario all season as much as the farmer this year. Smaller traders generally buy at a harvest low and cover the cost of carry and make a margin as prices improve as stocks shrink and the consumer pays a little more later in the year. This is not the case this year, a combination of good local production and falling international values created the perfect storm for lower local wheat prices. The consumer continued to see offers from the larger traders and producers throughout the season.

Old crop sorghum has buying interest for the Sept / Oct / Nov slot into the box market at $320 – $325 ex farm LPP, depending on time slot and location. Up on the Downs the box market is bid $357. Freight from the plains to the Downs is about $60, this doesn’t compete with the XF packer market here. Bids in the system at Werris Creek were closer to $300 site, or FOT $325, about the same as what the box market is bidding on an ex farm basis. This doesn’t really help the track seller, as both bids are equivalent. I may have a little room for some higher moisture sorghum in October, but not a huge quantity. If you have sorghum ex farm or in the system please bring the offer to me and we’ll see if we can get the price above the current track bid at least.