11/8/25 Prices

Mostly technical trade in US futures as the punters position themselves ahead of next weeks USDA report. Chicago wheat futures followed both corn and soybean futures lower while Minneapolis spring wheat futures defied the Chicago market, closing a couple of cent a bushel in the green. Paris milling wheat futures gave back most of yesterdays gains. Shedding €2.00/t in the December slot. Looking at both US and global futures markets it is hard to see any green at all. London feed wheat was lower, Paris corn lower, Paris rapeseed lower, ICE canola lower. MGEX spring wheat and Malaysian palm oil were two of the few softs closing in the green.

International cash markets generally followed the lead from the futures markets. HRWW values out of the US Pacific Northwest slipped the most shedding almost AUD$3.00/t compared to yesterdays conversion. White wheat values there held on OK, down just a few cents per tonne on average. Canadian spring wheat was firmer at the port, up less than AUD$1.00 compared to yesterday, as was US spring wheat. Cash bids for canola out of SE Saskatchewan were back, on average CAD-$8.08/t ex farm, pretty much reflecting the weaker Winnipeg market.

Durum out of SE Saskatchewan was flat for a Dec lift. The Dec window there has done nothing for a while now, nearby durum values there have slipped a little as harvest approaches but outer months are flat. There’s not much difference in price between prompt SE Sask durum and Dec durum now, prices have converged. Durum out of France seems to be finding it’s feet at current values, chart attached. When converting French values to a N.African or Italian consumer and then converting that CiF value back to an equivalent price here, we tend to see current values for new crop are about right.

Canadian feed barley values continue to slip away domestically. International feed barley values were mixed last night, the average coming out flat.

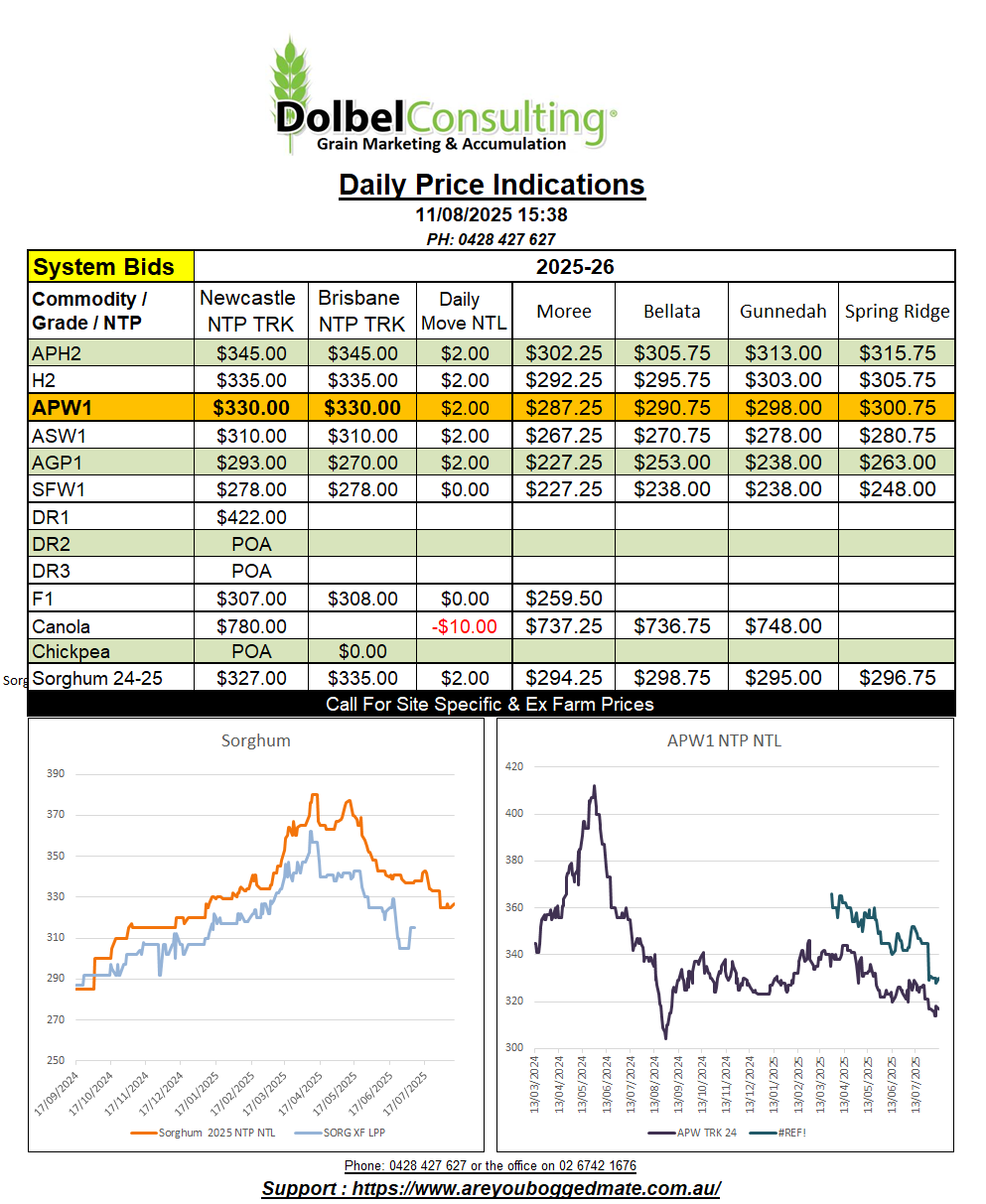

Cargill had 1kt of prompt sorghum to Carrington to buy at $358 delivered yesterday. This was going to compete with the Werris Creek packer market at $340 but was probably not that attractive given the port requirements versus the ease of execution locally. The ex farm market into the southern packer wasn’t lower though, bid at $320 ex farm for a Sept / October slot, the delivery window the biggest obstacle for most given the approaching winter crop harvest. The track market saw sorghum change hands at $300 delivered LPP site (all locations). This could be executed onto a truck for roughly $324.55 and road freighted to port or packer. Graincorp were considering execution of LPP sorghum out of the Willow Tree depot. If that was the case road freight to Newcastle would have been roughly $38.00, so landed Carrington at $362.55 offer, against a $358 bid, doesn’t work. The other logical choice would have been Werris Creek packer, although execution spread may have been an issue in that direction. Local freight would have come in around $22.00, so FIS Werris Creek at something close to $346.55, against a $340 bid, again doesn’t work. The system buyer was a packer, with freight costs of roughly $45 if executed from Willow Tree, so $369.55 delivered packer, last bid $365. Using all the options for arbitrage to compare the $300 site price, tells us the $300 site price was a good sell.

New crop wheat was mixed, flat to lower on the track and generally unchanged on a delivered consumer / packer basis. Opportunities to book new crop wheat at what could be a considered a “good” price remain few. International values continue to grind flat to lower. US exports continue to be strong while Black Sea exports are a little slower than usual due to some up country delays. Current new crop values here do reflect the soft international market closely.