11/9/25 Prices

There’s a USDA World Ag Supply and Demand Estimates report due out tomorrow night. The punters have been active squaring up this week, some of this action had been supportive but the steam appears to have ran out. US futures were a sea of red last night apart from soyoil. Wheat, corn and soybean futures at Chicago were all lower. Across the Atlantic the European exchanges were generally flat to lower, Paris rapeseed did buck that trend though, closing a little higher, up €2.00 in the Feb slot.

The stronger AUD made short work of the move in rapeseed, turning a positive into a negative. The AUD also exacerbated flat to softer market moves, turning conversions here in AUD terms lower across the board, bar Winnipeg canola, this morning. Even Delhi chickpeas were lower last night after trending higher this week. Back roughly 66Rs/Q, or to you and me once the AUD move is considered, -AUD$13.84/t. Delhi chickpeas are still showing a week on week gain of AUD$4.60/t, but the consensus in the trade now appears to be more along the lines of “when, not if” India introduces an import tariff on chickpeas.

The AUD is testing upper level resistance again, this time busting through 66c to set an overnight high of 66.34USc before drifting lower for the later half of the session, but still closing above 66c. Softer than expected US inflation data (PPI) overnight have the punters back on the US rate cut trail. Punters are tipping a 25pt cut to official US rates next week, a small minority expect to see as much as 50pts.

The day to day conversion comparison for US and Canadian wheat out of the Pacific Northwest was lower by AUD$3.00 to AUD$4.50 / tonne. White wheat out of the PNW slipped AUD$3.86/t. almost all of that due to the AUD. International feed barley values were mixed, the average generally helped by increases in Russian FOB values, but the greater picture couldn’t beat the pressure from the AUD and the average slipped by less than an aussie peso..

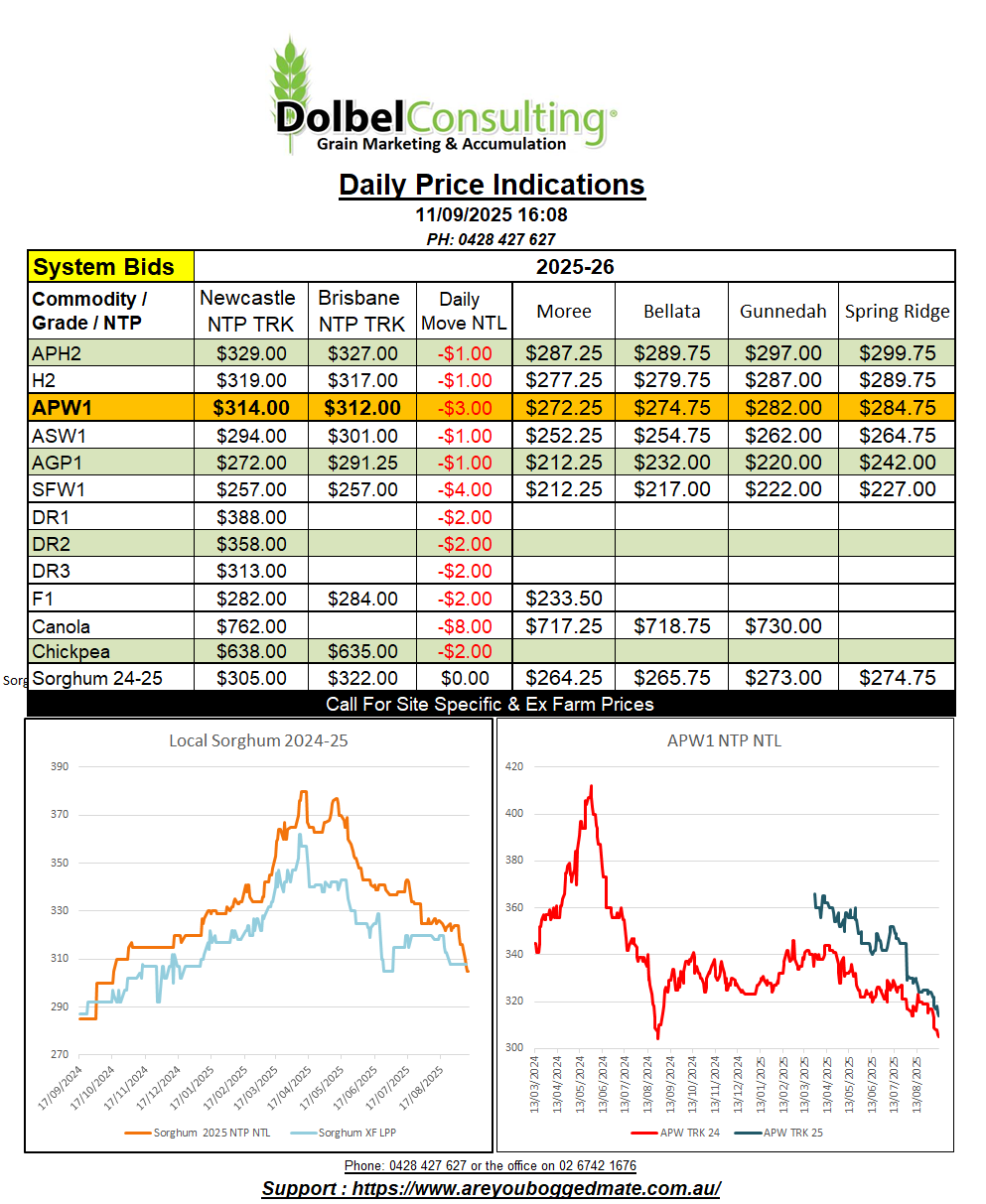

The local market is dead, most sellers have sold and most buyers have bought, leaving little liquidity in the old crop markets for white grain and sorghum. New crop grain prices continue to fall giving growers little incentive to contract at what could be a bottom in the market. Looking at season charts tends to back this plausibility up as well.

Chickpeas remain mixed, overnight weakness in the Delhi market may impact on new crop bids here today but the trade currently appear to have a significant buffer factored into new crop bids. The may have more to do with the speculation that India could at any moment introduce an import tariff.

Forward contracting pulse crops, unless utilising a full multi grade, acre based contract with 0 yield, is sometimes a little dangerous. Even a washout on a minimum production contract can be costly. The problem lies with the trade / trade side not the grower / consumer side. A washout value is determined by replacement grain value. If the only place the trade can find replacement grain is from the trade, then you can bet London to a brick that the trade will not go easy on the trader looking to buy when it comes to determining that replacement price.

The only other alternative is for the grower to find grain from another grower to fill the contract. Easy if the value of the contract is higher than current market values, but not so easy if everyone has shot and sprung grain and those that don’t get a sniff of a market short.

Over the last 3 months the Delhi chickpea price, converted to AUD per tonne, versus local price has seen a significant increase in the spread. From -AUD$130+/- when new crop contracts first came out, to roughly -AUD$400 +/- over the last week or two. Mind you a 60% tariff applied would still see reductions in local bids.