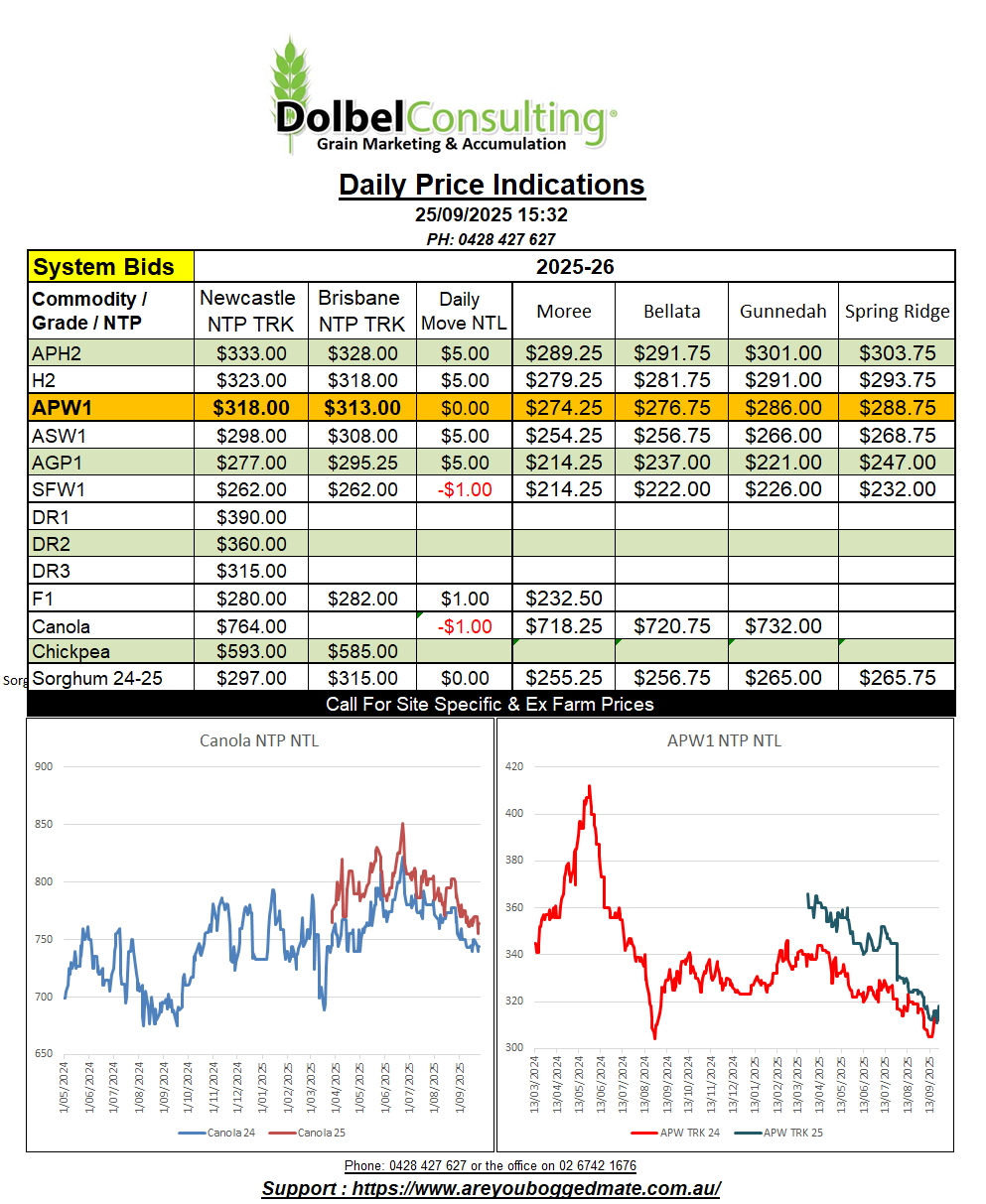

25/9/25 Prices

The Argentine government removed export taxes on all grains 3 days ago. The ruling will stay in force until October 31st, or until sales reach a value of 7 billion. That sounds like a lot doesn’t it. Over the last 3 days sales have totaled 4.2 billion. The move was an attempted to draw more dollars into the Argentine economy, looks like it’s working just fine. Grains like corn, wheat, soybeans and soybean products, barley, sorghum, etc account for roughly 39% of Argentina’s export revenue. Argentina also removed export taxes on beef and poultry.

It will be interesting to see what impact this has on the October WASDE, will it simply bring sales that were expected to be spread out over the year forward, will it mean more sales, if so who are these sales displacing. Is the US set to loose even more market share to S.America.

Currently I’ll call it a good thing for wheat and sorghum, here at least. Australia only needs to export an average volume of wheat over the last couple of months of the old crop marketing window to meet wheat export projections. One would assume that those sales are made and shipping is in place. So it should have little impact on old crop Aussie wheat, and given the window should have little impact on new crop as well unless it displaces Nov / Dec demand. I find this unlikely as the value of Argentine wheat over the last three days has moved roughly AUD$15.00 higher. Keeping it significantly more expensive than both US and Aussie milling wheat into the Asian market. So you can see where the money is going.

Paris milling wheat futures bounced of the mid term support number, and moved a little higher. Technical support combined with news of an up coming Algerian tender kept the market there in the green.

Cash values out of the US Pacific Northwest were mixed, HRWW falling roughly AUD$2.00 compared to yesterdays conversion, while spring wheat and SRWW were both a smidge firmer. The bigger moving was white wheat, up AUD$3.05/t compared to yesterdays conversion. Dry weather in the PNW a driver.

I spent a good portion of the day on new crop canola yesterday. Updating world supply and demand and having a closer look at some of the major consumers and crush demand. One thing that is hard to account for is oil type swapping, say from palm to canola to soybean. The interchangeability is limited in some uses but not others and that interchangeability can vary to some degree as well.

Just looking at canola / rapeseed we see that world production in 2023-24 89.99mt. There is basically 10 players in the world canola market that make up about 96% of the volume on the production side and 90% of consumption on the demand side. To concentrate on those players isn’t remiss. In 2023-24 the top 10 stocks to use ratio was 14.4%. In 2024-25 the stocks to use ratio was 12.44%, and this year, given current demand estimates, we could end up with a top ten stocks to use ratio of 13.43%, somewhere between 2023-24 and last year.

We all know about the Canadian / China problem, a 78.5% tariff is a big hurdle to jump, and will keep the Canadian market sharply priced. There is a number in the Canadian S&D table that may get tweaked in coming months though, that is domestic crush. Most S&D tables have domestic use for Canadian canola at 11.6mt in 23/24, 11.76mt last year and a projected 12mt this year. I have read reports suggesting that this domestic consumption number could be underestimated by as much as 2mt. If this is the case, and only time will tell, then top 10 S:U comes in at roughly 10.69%, that paints a different picture. With Canada blocked out of the Chinese market, increased domestic crush is very much feasible. The tables also show reduced Chinese import demand, probably due to substitution with S.American soybeans. It also shows a significant reduction in Canadian exports year on year, from 9.335mt to 6.7mt. If Canada can sustain exports closer to last year and increase domestic crush, two big ifs, then we may see prices pull back out of the current slump longer term.