1/10/25 Prices

International cash wheat conversions are generally lower compared to yesterdays conversion. The exceptions appear to be some Black Sea ports, mainly Ukraine. US and Canadian values out of the Pacific Northwest were back AUD$5.00 to AUD$8.00 per tonne when compared to yesterdays conversions. Even white wheat out of the PNW was softer, that conversion shedding AUD$5.36/t day to day.

The stronger AUD has something to do with it, but as a rule a stronger AUD equals a weaker USD, a weaker USD should in theory equal better US wheat values. That wasn’t the case last night. The punters at Chicago pushed values there lower, Dec 25 SRWW futures shed 11c/bu, ignoring the fundamentals of the excellent US wheat export pace. US values into the Asian market are also good, not needing to “buy demand” under current values.

Take HRWW for instance, moving out of the PNW into the Asian market it’s worth roughly US$250 C&F Asia today. If we were to compare that to Aussie H2 wheat, similar protein but better milling characteristics, H2 comes in closer to US$265 C&F Asia. This spread has moved wider by roughly US$5.00 over the last week or so.

Asian buyers must be looking at US wheat and thinking how much lower is this going to go. Should we buy now or hold off and see what kind of stimulus Mellie will feed the exporters out of Argentina in a few months. Will the Russian ruble collapse and Russian farmers finally get the domestic price they are hanging out for in rubles per tonne, only to have US/t values out of the Black Sea fall away. Will the Euro move lower against the USD as tension rises between NATO and Russia. There is so much political play at hand at present that the fundamentals almost appear irrelevant.

The worlds major exporters of wheat have stock. The desire of the major importers to change their hand to mouth strategy in purchases is currently under no fundamental pressure. The only foot on the supply brake pedal at present is that of the grower and their lack of incentive to meet this market at current values.

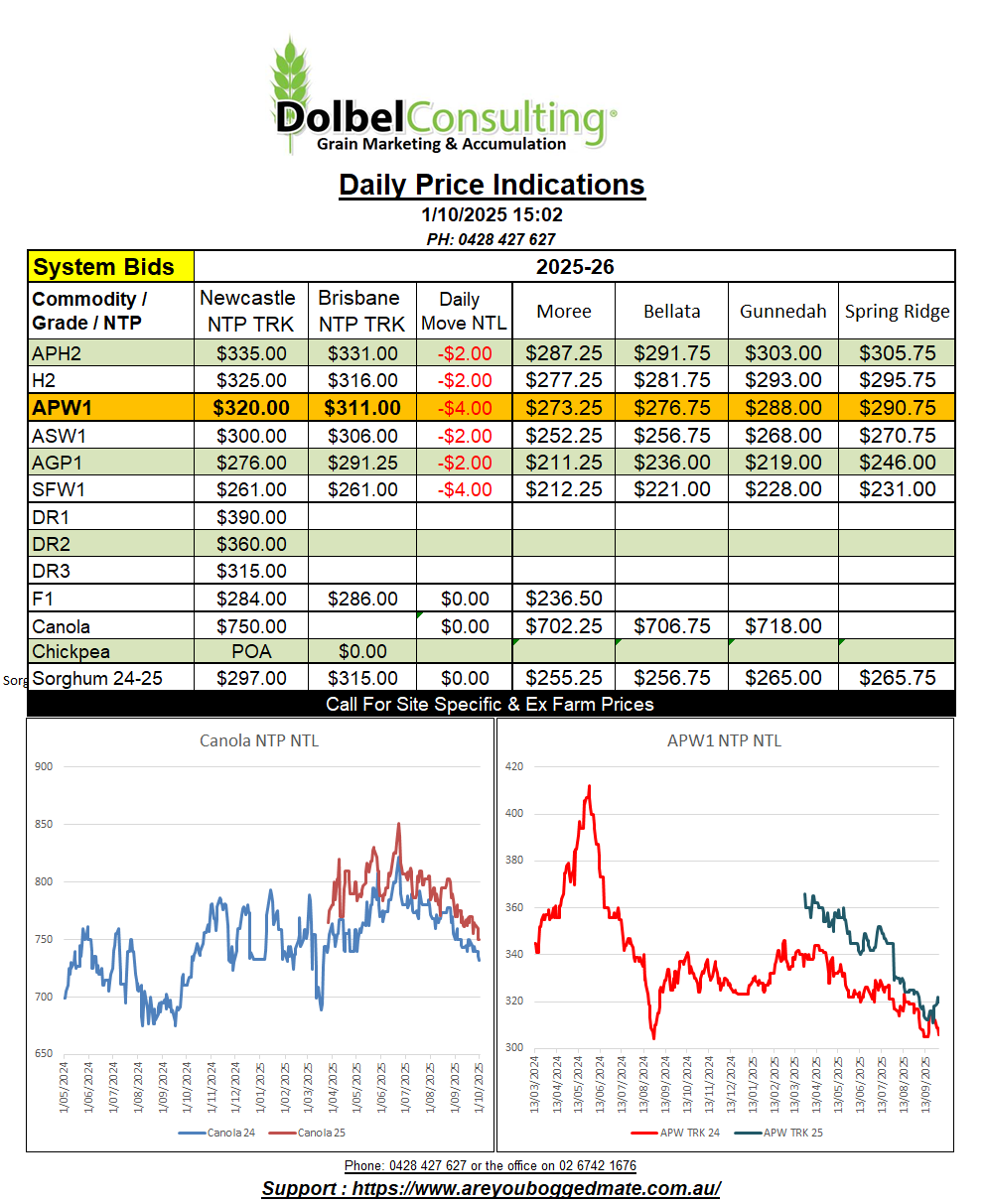

The move higher in the local track wheat market surprised me yesterday. The base grade APW was $3.00 per tone higher. An improvement in basis to Chicago wheat futures from roughly +48c/bu to +54c/bu. Is this a trade opportunity to sell basis.

Don’t go glazing over now I’ve mentioned basis, it’s important we take a look at this and ask why would local values move against the trend in both US futures, US cash and a higher AUD against the USD. Was the move higher pre-empting an increase in domestic values. We also saw ASX wheat futures increase $2.00 / tonne. That contract tends to reflect the Melbourne wheat market. Was it simply a case of the trade “getting it wrong” (hungover).

Overnight US futures, and most of the international cash wheat market, apart from Ukraine, moved lower in value compared yesterdays conversions. If the trade did get it wrong, we may not only see some downside reflecting last nights shift lower in international markets. We may also see the couple of dollars downside that wasn’t reflected in yesterdays session here taken away, plus the $3.00 jump yesterday. Not a nice thought but a realistic one.

The local new crop wheat price is already testing the downside estimates using traditional spreads. This doesn’t mean it can’t go lower, but it does show that grower resistance at these values is very high.

The desire of the trade to buy at this basis level, high basis, may also be very low. Will the trade play the long game, meeting grower offers now, getting some volume on the books, then push basis lower as the bulk of selling picks up? A trade book is a book of averages after all. Or will international values recover from this post harvest lull, local prices stay flat, eroding basis as we move towards harvest, allowing the trade to buy low basis at harvest.