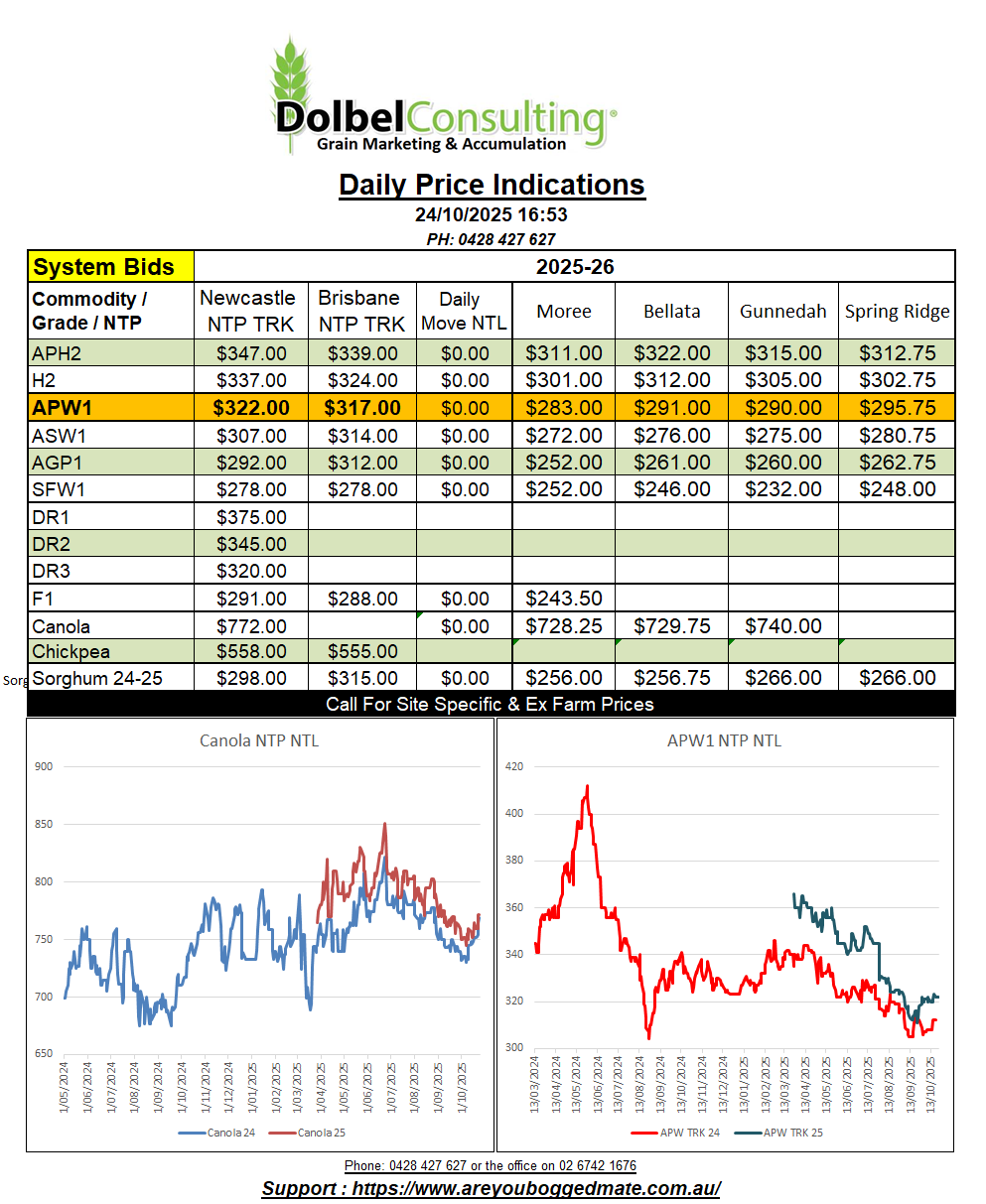

24/10/25 Prices

There’s a bit of push and pull in the international durum market at present. Drought continues in Turkey, creating sowing problems for dry land producers and potentially reducing supply into the Turkish pasta processing industry for 2026-27. Turkey is also expected to limit 2025-26 exports.

The current situation is basically good international production. The IGC say as much as 36.5mt of durum will be produced this year, increasing carry over stocks while world trade decreases due to better domestic production from some N.African importers. But is this the signal for lower prices, potentially no. There’s still a dark cloud hanging over the grade splits for the Canadian crop. Rainfall has potentially severely downgraded 30% of the Saskatchewan crop, meaning we could see a significant reduction is the supply of top grade durum from Canada.

On the flip side we have France producing one of the better quality durum crops they have grown in a few year. Even with France producing 1.26mt of top quality durum and Italy producing 4mt of excellent durum, taking EU production to 8.3mt. There will be continued demand for good quality durum into 2026, as less than 30% of the Saskatchewan crop made the top grade. We should still see good export demand for a premium product. The biggest threat to values is probably in the lower grades, but the recent Algerian tender indicates downside potential there is probably limited.

US wheat futures pushed a little higher overnight as funds liquidate shorts. The stronger AUD is hurting both CBOT conversions and cash price conversions for milling wheat out of the US Pacific Northwest. Compared to yesterdays conversions we see PNW HRWW cash values +AUD$5.47 / tonne, spring wheat up AUD$4.77 for US wheat and AUD$3.51 higher for Canadian spring wheat. The net move in futures is about AUD$4.10/t, the AUD taking back about AUD$1.11/t of a AUD$5.22 move higher. French milling wheat was only up €0.25/t in the March slot and unchanged in the December slot. Cash values out of the Black Sea were lower compared to yesterdays conversion, Ukraine wheat sharply so.

With canola and wheat harvest about 10-14 days away in the Forbes / Condo area we are starting to see agronomists produce some yield estimates, and they are not great. Yield expectations for canola are coming in around 1.4t/ha, and wheat at 3.5t/ha. The season here on the plains has been much better with local yields potentially doubling these estimates for some fields. The dry finish across NW Victoria is also seeing some canola used for silage, walking the canola off the farm this year.

Local canola values were the big mover yesterday, following the move in the EU market. If we track Paris futures again today we should see further upside. The day to day conversion comparison has been impacted a little by the firmer AUD, but there’s still potential for +AUD$2.49/t if we track the Paris rapeseed futures as we have been. The question now is, is this a selling opportunity. With the risk of sounding like a cop out, every day is a selling opportunity. Do I think this market is going higher. Well as I’ve said before a lot depends on the demand side from China for Aussie product, and how much the Canadian domestic crush can increase. Looking at crush margins tells me that there is plenty of fat in the oil / meal side of the equation at current numbers. So there’s theoretical upside in canola seed values. The other way to look at it is cash flow. One would hope that wheat has more potential upside from here versus the upside potential in canola. This may push a few growers towards cashing canola on a rally to create cash flow versus early harvested wheat. Wheat basis may be telling you there’s more potential downside than upside, but even with the high local basis vs Chicago that we are seeing in wheat, from a cash price comparison into the Asian market Aussie wheat is still good value. For example HRWW out of the PNW will land into the Asian market for something close to US$252 C&F, while Aussie H2 wheat at current values is closer to US$268, that’s only a USD premium of US$16.00 for top quality white wheat. That’d appear cheap.

The cloud mass associated with the area of low pressure across the SW on the continent is pushing east towards the WA / SA border this morning. By this evening SA should start to see a few showers associated with this system. Some the forecast models are predicting falls of up to 36mm for Kadina in S.Aust from this change on Saturday. Too little too late for some but it could stop the decline in later sown crops, which there are plenty.

The synoptic chart predicts the complex area of low pressure to consolidate into a single low cell a little further south than initially expected, but still far enough north to have an impact on Victoria and possibly the Riverina on Sunday. A front extending NW away from the low will move across the NSW wheat belt on Sunday, as the low moves through Bass Straight and into the Tasman late on Sunday evening.

Showers are expected to start across the far SW of NSW early Sunday morning, reaching the central west wheat belt around sunrise. Falls will be much heavier south of the NSW / VIC border, but even the heavier falls may only amount to 5-15mm around Shepparton. The south coast and Melbourne may see more than 30mm.

Here on the plains showers may spill over the Liverpool Range from the SW mid to late morning Sunday. This change is starting to look like a bit of a fizzer on most models for anyone north of Dubbo. With airflow turning from the SW on Monday conditions will be cooler, 26C. As airflow turns to be more SE-E on Tuesday we should see moisture pushed west of the ranges feeding into an area of low pressure over NW NSW. Storms will develop around Bourke at sunrise, becoming more active to the SE of Cobar in the afternoon. Midday storms will push NE from Nyngan towards the LPP by arriving around sunset, LPP 5-30mm.