28/10/25 Prices

The AUD is often viewed in the currency trading world as a liquid proxy for the Chinese Yuan. Hence when the press tell the world that the talks between the US and Chinese preventatives over the weekend went well, then that must be good the Yuan, bam, they buy Aussie dollars. Australia benefits greatly from an improved Chinese outlook, hence the connection. As long as Chinese demand for raw material is supplied in volume from Australia there is no reason this connection should break. A few punters are also of the opinion we may not see the pre-Christmas rate drop from the RBA in a couple of weeks.

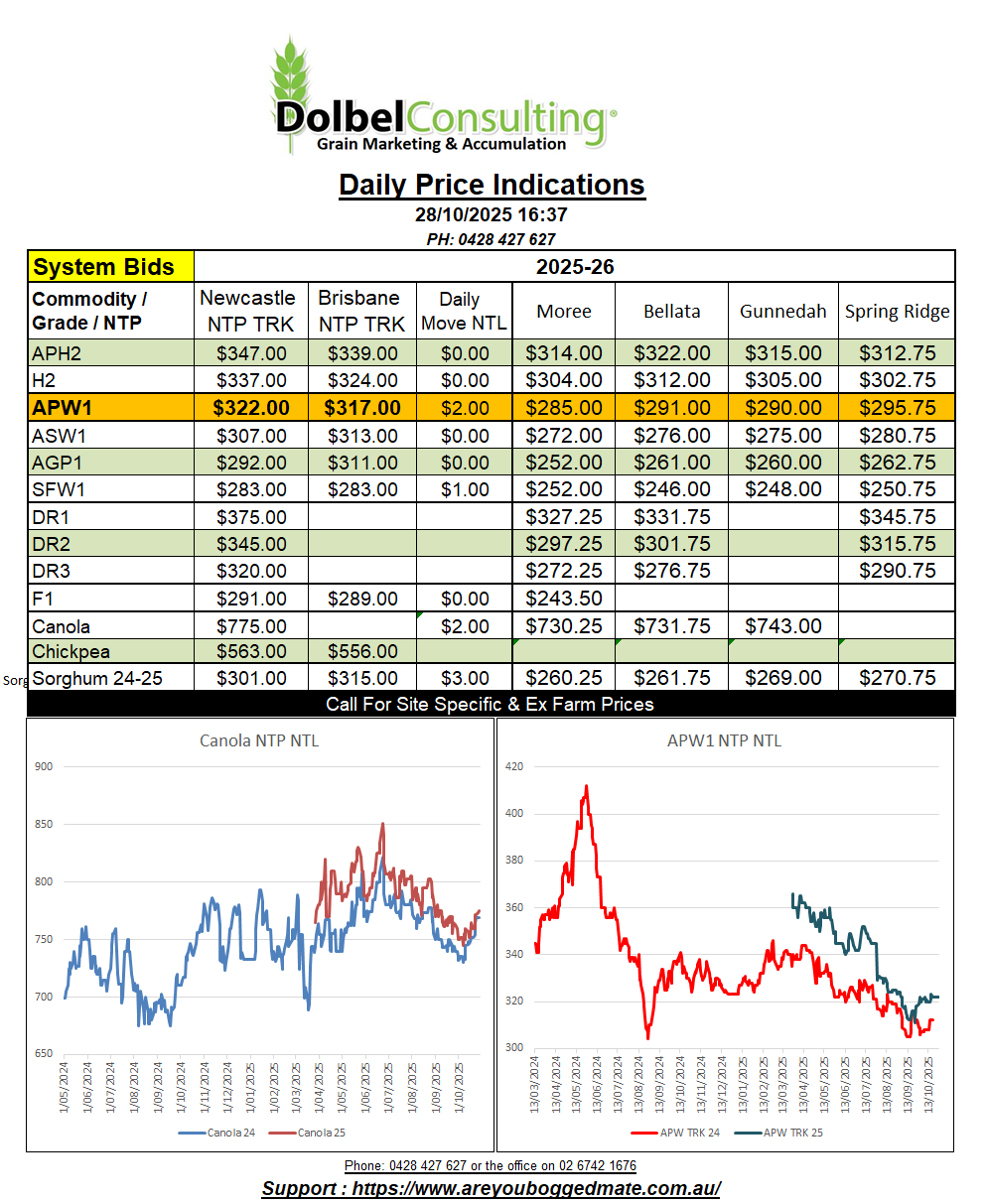

International grain markets were generally stronger, FOB values for US, Black Sea and EU wheat all improving. The thorn in our side when converting these changes and comparing today’s values to yesterdays values in AUD/t is of course the stronger dollar.

US Pacific Northwest wheat was firmer, but compared to Fridays conversion value, spring wheat out of the PNW is back AUD$0.79/t and white wheat is back AUD$2.27. It’s not all doom and gloom though, US HRWW did see more upside than some of the other grades, and even with the higher AUD being considered we still have upside in the day to day conversion comparison of AUD$4.47/t. French wheat was another good one. The AUD moving less against the Euro than some of the other currencies. French 12% milling wheat day to day comparison improved by over AUD$6.00/t. Ukraine values were also sharply higher.

FOB values for wheat were said to be higher on increased tension between Russia and …. well the rest of the world..

Chinese rapeseed imports were sharply lower in September as the Chinese consumer / importer got used to the huge import taxes on Canadian canola. September volume was back 86% versus last year and 53% lower than August. For the calendar year Chinese imports stand at just under 2.5mt, this time last year volume was over 4mt. Not sure what the “talked about” US / China soybean deal will do for canola, probably not bearish though.

New crop sorghum saw a public bid of $307 ex farm SE LPP yesterday for the March / April slot. On the surface this doesn’t look like a bad number, anything starting with a three is generally acceptable at the farm gate, probably more so this year. The question is does the bid reflect international values and is the risk worth the reward. The later the main question when forward contracting.

US continues to have trade negotiations with China. Currently China have a 10% import tariff on US sorghum. US sorghum for May next year is roughly valued at US$258 C&F China. Plus the 10% import tariff gives us a delivered China bid for US sorghum of just under US$284 C&F. This would roughly work back to a FOB Australia number of something close to AUD$392, cost vary to calculate this back to an ex farm LPP number, but let’s work on -AUD$65, so call it $327 ex farm LPP equivalent.

The other origin we need to consider is Argentina. Currently their sorghum is valued at roughly US$211 FOB Argentina river port for November. This works back to roughly US$264 C&F China. For our sorghum to sell at a similar C&F China value it would need to be valued something close to AUD$297 ex farm.

These numbers tell us an upside to $327 XF and a downside of $297 +/-. So the $307 XF SE LPP number is probably a fair bid, but not a great bid. It’d be nice to see some volume on the offer side to see if we could get the bid closer to the $327 XF mark.

The biggest issue today will be the AUD. It’s up against all the majors, buying more than 100 yen for the first time in ages. The AUD was strongest against the Indian Rs. This may see some of the recent gains in chickpea values handed back today.

We’ll find out if this change is another fizzer over the next 12 hours. The satellite map shows the development of the area of low pressure around Cobar and active storms across much of Queensland. The BOM don’t expect the area of low pressure to develop into a cut off low and reek havoc across the area, so we better be ready for anything. The low is only rated at 1010hPa so they might be right. Cobar is currently 1011.7hPa.

Airflow here is expected to turn from the SE to the east and potentially the NE as we move through the day. Easterly airflow would feed moisture inland, possibly triggering a few more storms across the NWSP.

The ECMWF model looks better than the BOM forecast if you want some rain. Always a questionable topic late Oct / November. By this afternoon the model predicts the low to be between Cobar and Nyngan. The more severe storms will develop to the NE and SE edge of the area of low pressure. That includes the northern LPP, Narrabri and Moree to Mungindi and SE of Nygan towards Dubbo. By 4pm storms are expected to have produced 10-15mm around Boggabri, north to Narrabri and Moree, Falls across the LPP south of Gunnedah may be a little lighter….. initially.

A second band of storms are likely to develop early in the evening, heavier west of the Newell around Baradine and Piliga, these storms will track slowly east as they break down towards midnight. It’s this second band of storms that may or may not push totals on the LPP above the 10-20mm mark.

Conditions should clear across the plains by mid to late morning Wednesday, but there is a slight chance of a clearing storm tomorrow afternoon or evening, more so to the east across the New England, but potentially across the LPP too.