29/10/25 Prices

Reuters reports that late monsoon rain has damaged summer crops in India. Western Maharashtra has seen fields of rice, soybeans and cotton written off by the late season deluge and associated flooding. Some yields are being slashed by as much as 80% in some locations, and then there is the quality problems. The rain has primed winter crop fields for wheat, canola and chickpeas. Producers will struggle to make repayments using the income generated by the failed summer crops in some areas, possibly reducing sowing inputs.

It appears that every time India states they can help out they get pushed back down. When the Russia / Ukraine war broke out India was there to state they could fill the void left by shrinking Black Sea wheat exports only to see their own wheat crop shrink. This time around we recently heard that India was going to help supply oilseeds to China, canola meal and oil, due China’s Canadian ban. Only to see Indian import requirements likely to increase by 1.5mt.

One crop to keep an eye on is mung beans. There are reports of large areas on mung beans being damaged, firstly from the August rains and now the late season rains. Officially the Indian government is reporting a surprisingly low level of damage to summer crops. Market value for the quality of mung bean being produced in India may be giving away what the quality is really like though. With a government minimum support price of 8768Rs/Q versus a market price of 6500Rs/Q it tends to indicate that something isn’t right with the crop quality. Time will tell.

Chicago soybean futures continued to push higher, dragging corn and wheat along for the ride. The lack of US Gov data and little fundamental change to the global outlook for wheat has resulted in the deterioration of basis against US futures for many non US markets. The stronger AUD is also an issue, hurting the conversion again this morning. Higher grade US red wheat out of the PNW is +/- AUD$1.50/t this morning while US white wheat out of the PNW was higher. The AUD didn’t help but the net change is roughly +AUD$3.20/t compared to yesterday for white wheat. Making Aussie wheat more competitive.

Local merchants are not actively engaging this market at present. They have bids on CropConnect they are happy to book grain at, but this early in the harvest they are showing little interest in following offers to sell above the bid higher. This isn’t always the case but it is becoming apparent that the softest seller may well set this market in the short term, which is usually the case in good volume years.

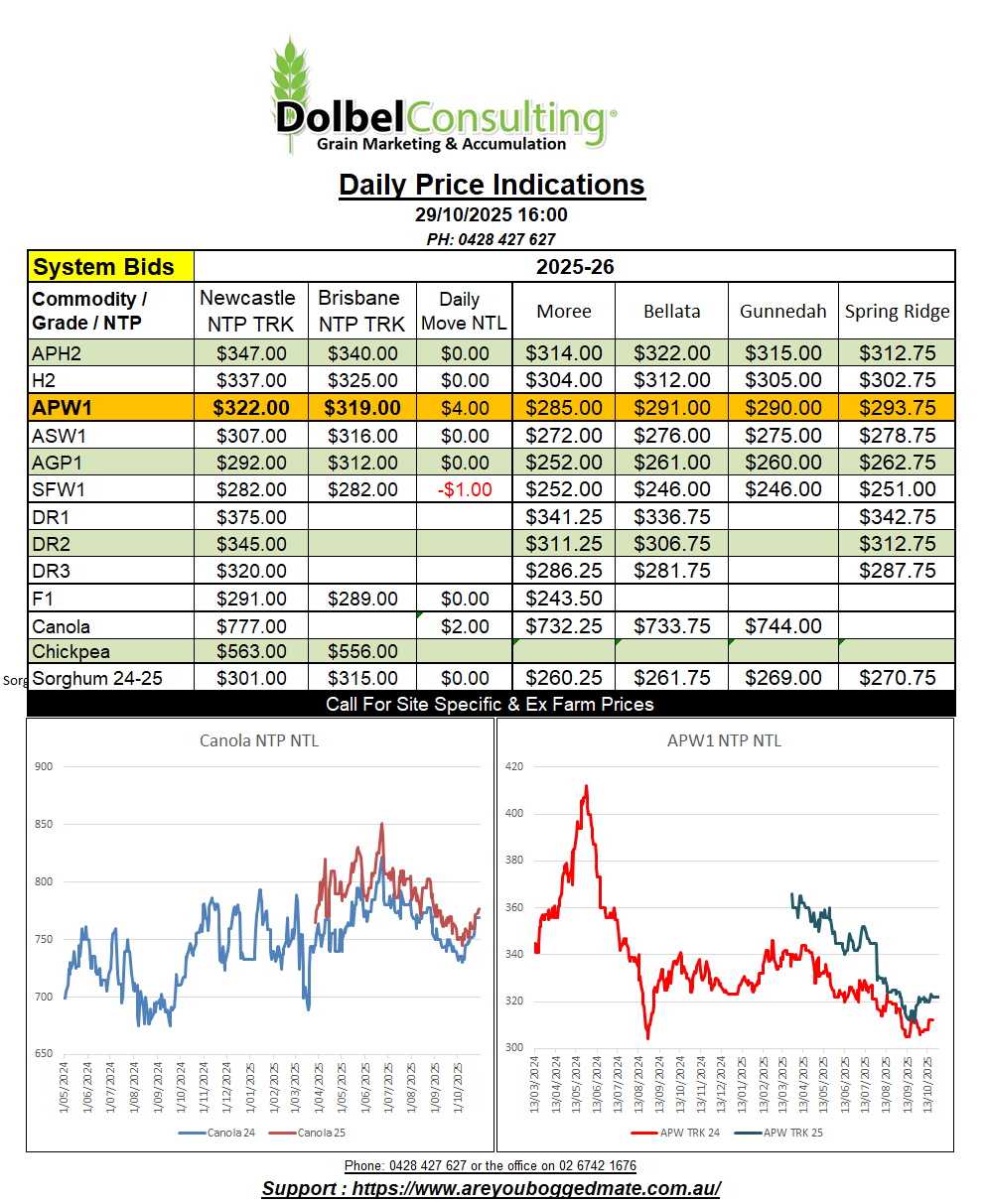

Yesterday we saw basis for APW wheat versus Chicago futures slip substantially, falling from +58c/bu on Monday to +45c/bu yesterday. A result of a rally in US futures and a flat market here. Granted the rally in US wheat futures had no fundamental strength and was potentially just a rally on the back of potential US / China trade deals with soybeans, but at the end of the day it was a sharply lower basis.

The trade have struggled to make back to back profit for a while now, this year is shaping up to be no different. Basis trading could be a tool being used to enhance the small level of profit being used in flat price trades. If for instance if a trader sold basis last week at +70c/bu and is looking to buy this week at +45c/bu this gives them a basis profit of almost AUD$14.00/t, less hedging costs, already. The flat price for APW during the same time has done nothing.

The failure to engage with growers in the canola market is also a little frustrating. It’s the 29th of the month today, the worst time of the month to try and sell track grain. This year Graincorp continue to offer 6 months free storage to the producer. This doesn’t apply to the trade though, if they buy today, they pay warehouse fees from Saturday. This may explain the lack of engagement for those producers looking to sell and transfer in October.

With both the Paris and Winnipeg canola conversions improving overnight, even when considering the stronger AUD, we should see better canola $$ today.

7 Day Rainfall: Dalby 13mm, Miles 16mm, Roma 6mm, Wallumbilla 21mm, St George 13mm, Moonie 13mm, Goondiwindi 19mm, Millmerran 23mm, Warwick 34mm, Toowoomba 58mm, Garah 9mm, Moree 23mm, Bellata 10-45mm, Rowena 24mm, Walgett 14mm, Coonamble 17mm, Gunnedah 25mm, Premer 15mm, Mullaley 21mm, Blackville 19mm, Spring Ridge 18mm, Gilgandra 4mm, Trangie 4mm, Forbes 7mm, Condo 3mm, West Wyalong 7mm, Wagga 9mm, Deni 6mm.

The low cell that created the showers last night is now off the east coast of Brisbane / Byron Bay. With a high cell off the SE coast of NSW and another high west of Tasmania we should continue to see easterly airflow being created by both the location of the highs and the low off the coast. This should keep storms and showers active along the ranges from the far south of NSW to the Gulf today.

As the low cell pushes further east the high in the south will combine over the Tasman on Thursday / Friday keeping air flow from the E-NE through to the weekend.

The BOM expect to see the development of another area of low pressure over NW South Australia drift SE across SA and W-NSW and W-Vic on Friday potentially producing storms across the southern half of the state before clearing on Saturday.

With airflow generally from the SE here but turning more SW-W later in the day we may see storms remain active along the western edge of the ranges before clearing to the east this evening. Saturday’s storms are not expected to push north of the Hunter west of the ranges. Storms again Mon / Tue.