6/11/25 Prices

International grain markets were relatively quiet overnight leaving the AUD as a major influence this morning. With the dollar improving by 0.34% against the US dollar, and against many of the regions trading partners, we see some losses in the day to day conversion for most grains.

Delhi chickpeas done nothing overnight, thus the AUD move creates a AUD$1.77/t move lower in the day to day conversion. It’s probably not enough to be reflected in the day to day cash prices here, but it doesn’t help our cause when attempting to talk the market higher.

Generally international cash wheat values were flat to less than AUD$2.00 lower when taking the AUD into account. The bigger moves lower were in spring wheat values for US and Canadian product out of the Pacific Northwest, and Argie wheat, which remains very competitive as they look likely to harvest a record crop after a wet winter. Compared to Aussie H2 wheat into the Asian market, Argie wheat is still a little expensive, roughly US$20.00 over the Aussie protein equivalent for a Jan / Feb slot. Time will tell if Milei wants to put on another flash grain sale like he did last month by reducing export tariffs. It served Argentina well and generated much needed US dollars in a hurry.

Russian milling wheat was valued at roughly US$232.75/t FOB. This puts Russian wheat into the market at roughly US$276.75/t C&F east Asia. Not a huge premium to either the US or Aussie product, and comparable to US and Canadian spring wheat values. It’s probably not cheap enough to compete with these grades though, but may still be used as a bargaining chip by the consumer.

US wheat is our major competition at present. The US has used the threat, or implementation of tariffs, to negotiate sales and it’s worked well for the US, for now. Longer term we’ll see, it’s done nothing to influence price, it hasn’t pushed prices higher, but it has seen US wheat exports increase. This isn’t a hugely bad thing as it will result in lower US ending stocks if the pace persists. It also means that the stronger pace in US exports, should be somewhat countering the slower start to the wheat marketing year that Russia had. Global fundamentals are pointing to a longer period of flat prices unless politics intervene.

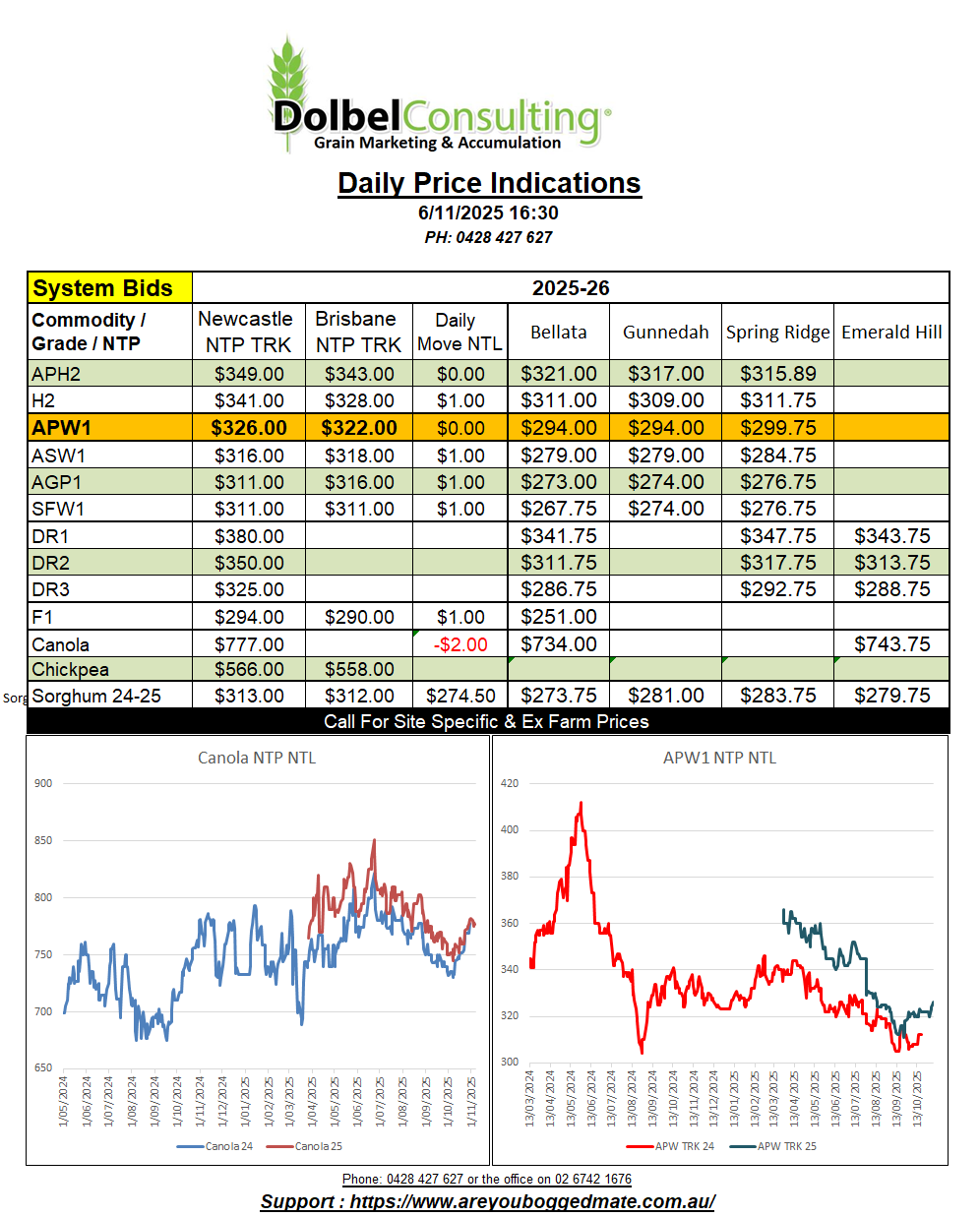

Local basis to Chicago SRWW futures has continued to fall dramatically this week. From a high of +71c/bu back on the 22nd of October to a low of +28c/bu yesterday. It was always on the cards but still disappointing to see. At the spot rate it reflects a basis decline of just over AUD$24.00 / tonne. The local markets were having none of the volatility in US futures, unless they could make basis trading work. During the same window local cash prices on a Newcastle NTP basis have risen AUD$2.00/t, Chicago in AUD/t spot rate are up AUD$28.80/t.

Does this mean much, besides the funds and basis traders making some profit. On a cash grain comparison into the Asian market the current H2 bid here reflects a price of US$270 C&F, the HRWW value out of the US Pacific Northwest reflects a delivered Asian consumer number of US$265. So the answer is yes, yes it does mean something. It means that the US$20+ premium we had over US HRWW is now just +US$5.00.

A more accurate comparison may be white wheat values for US wheat into the Asian market. Today this number is close to US$270, pretty much the same as what Aussie white wheat is valued at. I find this interesting considering that US hard white wheat production has declined 28% in 2025, not much more than 380kt. US soft white wheat production is 6% higher though, at 6.25mt. So it disturbs me that we are seeing values in NNSW more closely reflect the lesser grade of US white wheat.

The next obvious question is will this premium improve. With quality in the north looking pretty good supply isn’t going to be an issue. Port by road values reflect a slightly better ex farm return than the system. H2 into Newcastle port by road was bid at $355 yesterday, $315 XF LPP, Vs $310.75 into Graincorp Spring Ridge. One would hope that the port by road number improves as we get past harvest and the trade see less low hanging fruit. BNE = $360/t.

The WA wheat fields saw a few showers yesterday, Geraldton in the north picked up 7mm, Morawa 12mm, Dalwallinu 0.2mm, Cunderdin 2mm some nearby locations to Cunderdin did see up to 27mm. Newdegate picked up 9mm, Katanning 2.5mm and Salmon Gums 3mm. Not as much as some models had predicted, and only delaying harvest by a day or two.

Cloud associated with the low cell that produced light showers across the WA wheat fields is now pushing across southern South Australia. The heavier falls are closer to the south coast but are by no means heavy, Cummins so far picking up less than a mill.

Rainfall associated with this low should increase across SA and W-VIC tonight and tomorrow. As the low cell passes across Bass Straight on Friday the BOM synoptic analysis predicts a trough line will move across the NSW wheat belt.

The ECMWF models shows storms mainly in the SE of the continent from midday to late afternoon but unsettled weather increasing across both the NWSP and CW of NSW by early evening on Friday. Storms are expected to become more active across the Piliga after sunset Friday and track NE, potentially becoming more severe around Millie or Bellata late Friday night.

Storms may clear to the NE on Saturday morning, but are expected to develop again as Saturday warms up, potentially becoming more widespread across the NWSP on Saturday. The amount of general rain expected remains minimal, probably less than 5mm. Storms clearing to the NE later Saturday arvo.