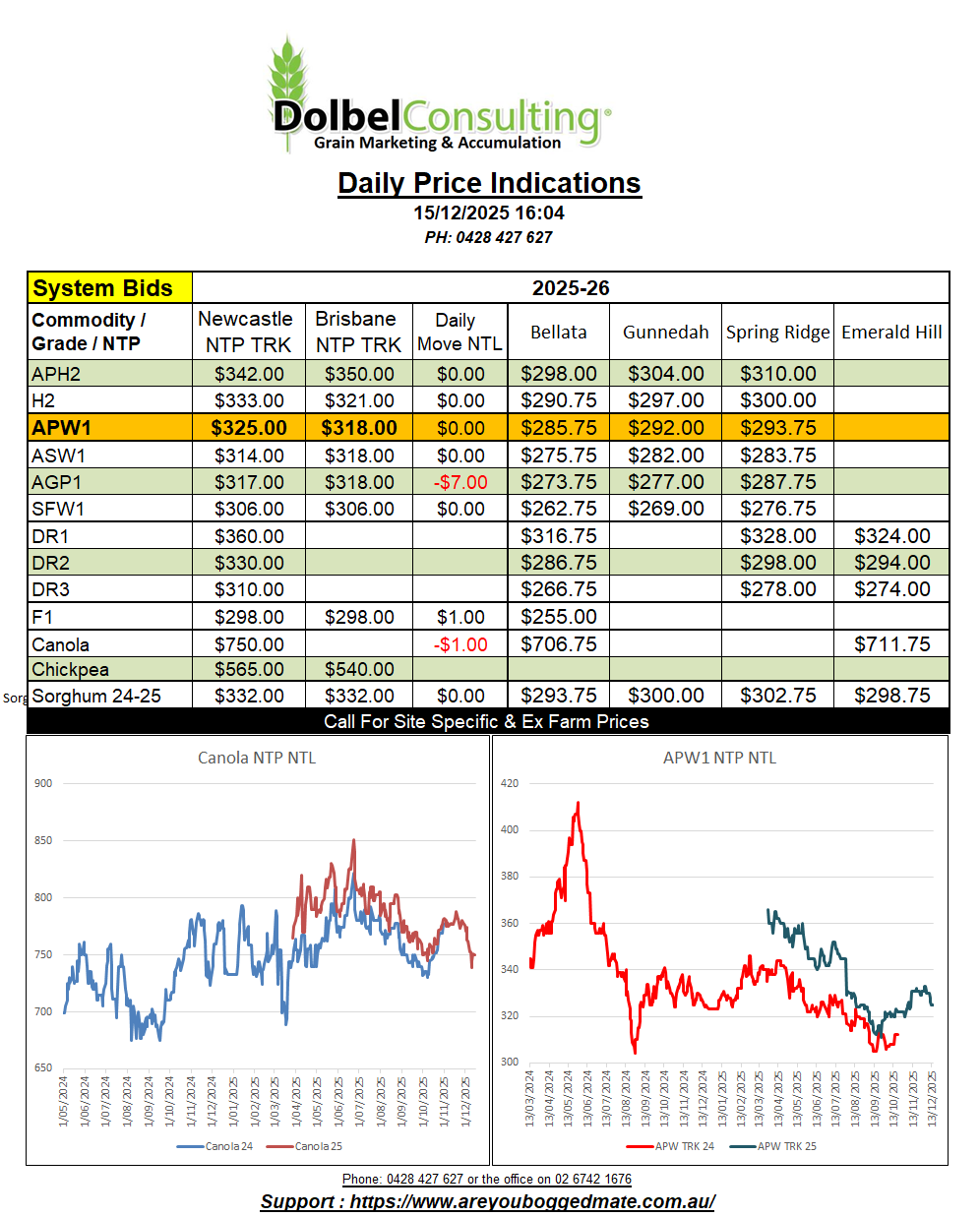

15/12/25 Prices

US wheat futures continue to fumble around in the dark as the December contract rolls off the board. Dec HRWW futures at Chicago saw a decline of 16.75c/bu last night on a volume of 40 contract, talk about caught, someone fell asleep at wheel.

The March contract for HRWW wasn’t pushed as low thankfully, slipping just 4.25c/bu, with a more fluid volume of 22,065 contracts changing hands. The funds are still short wheat, and appear happy to keep it that way. Sometimes we see fund positions adjust in Jan / Feb. Seriously though with the global wheat S&D shaping up the way it is, I can’t see why the funds would jump into wheat and go long. Unless it’s political.

The Rosario Grain Exchange in Argentina increased it’s projected wheat production estimate for Argentina from 24.5mt to a record 27.7mt, up 3.2mt. This estimate is well above the number the USDA pulled out in the Dec WASDE, 24mt, and it was an increase of 2mt from the last USDA estimate.

Argie milling wheat values, FOB river, remain volatile. Talks of reduced export taxes, and now larger production, has seen closing values for cash river wheat move by as much as US$10.00/t on a daily basis, but remaining range bound.

Last night the cash river market appears to have closed a little higher, around US$242/t FOB for a Feb slot. If we use this estimate and determine a C&F Asian buyer value we come up with something close to US$285. US$15.00 higher than what the grower bid here would represent to the same market. Taking white wheat into consideration, and a trade margin, it would indicate that the international milling wheat market remains very, very competitive.

Weekly US export sales for wheat and corn were very good, both coming in larger than the average trade guess prior. US corn sales to week ending Nov 13th were 2.38mt, taking MY sales to 40.721mt, up 30% Y/Y. Wheat came in at 850kt, taking sales to 18.117mt, up 24% Y/Y. US soybeans continue to lag.