16/12/25 Prices

US weekly export inspections for the week ending Dec 11th were good for wheat and corn, coming in towards the higher end of pre report trade estimates. US soybeans export inspections were not so good, coming in well below the lowest trade estimate.

Let’s focus on the positives, corn was estimated between 1mt and 1.6mt prior, and came in at 1.583mt. A little lower than the 1.741mt from last week but keeping a very strong pace up, and taking US year to date corn inspections to 22.501mt, up 69% year on year. Obviously corn futures fell 1c/bu. ???

US wheat export inspections were estimated to be between 250kt and 500kt and came in at 488kt. An increase on last weeks 396kt. This takes year to date US wheat export inspections to 14.125mt, up 22% year on year. Obviously US wheat futures fell 6 to 8c/bu.???

The weakness in US soybean export sales rolled across to softer US soybean futures, which in turn softened Winnipeg canola futures, producing lower cash prices for canola across SE Saskatchewan and capping the upside potential across the greater oilseed complex. Paris rapeseed fared well in the Feb slot, just €0.25/t lower, a number the weaker AUD/Euro managed to counter. Palm oil was also caught up in the weaker oilseed market, shedding roughly AUD$4.78/t in the Feb slot.

Canadian canola is valued at roughly US$530/t C&F EU port. This represents a much better buy for the EU compared to current Aussie C&F values using local bids as a guide, cheaper by something close to US$80.00. This spread above Canadian canola into the EU isn’t that unusual though. Australian product has managed to pull a significant premium to Canadian product for some time now. Into China we see Aussie product roughly US$100 more than the Canadian equivalent, but Aussie still cheaper than Ukraine canola into China.

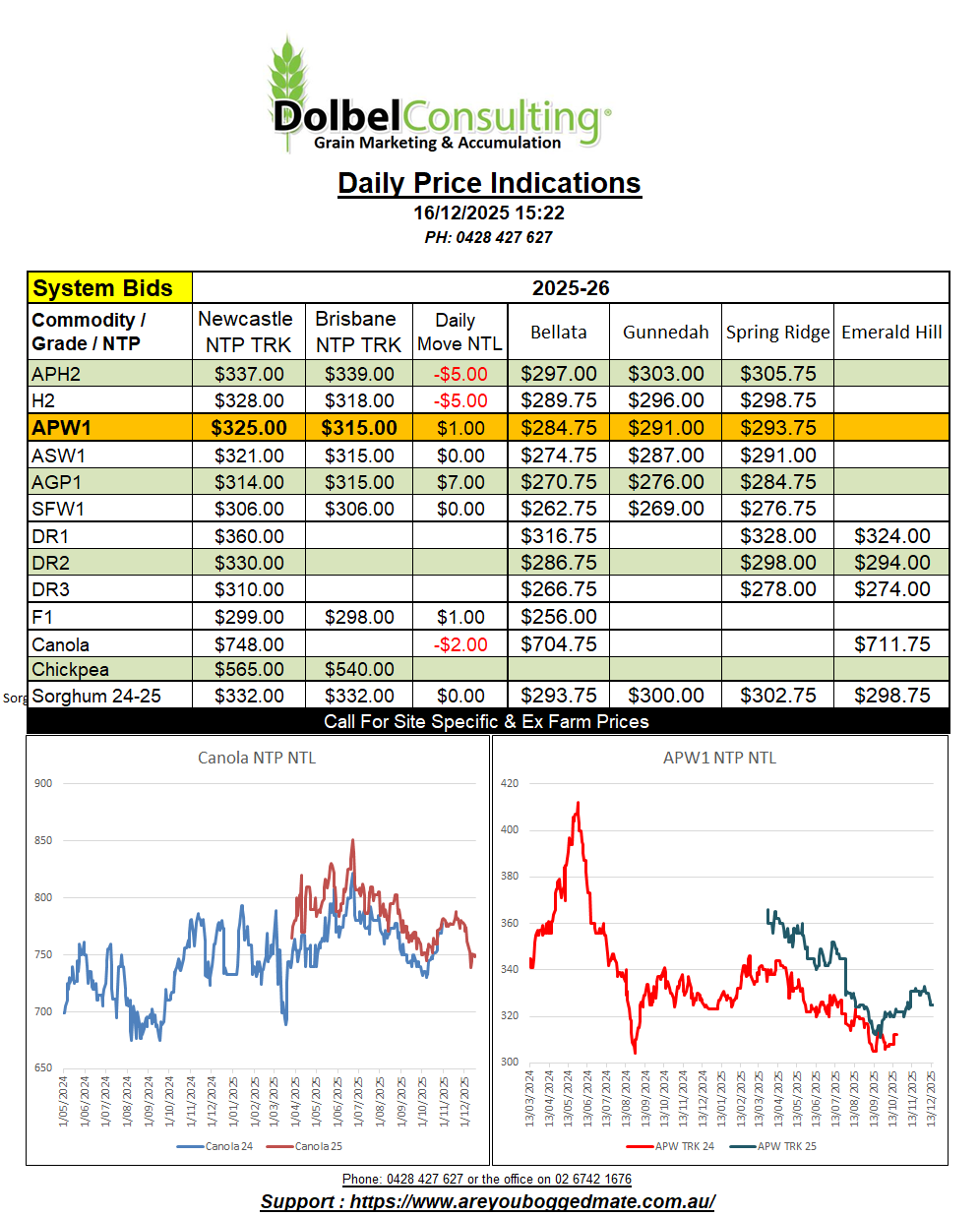

Aussie basis to US wheat futures remains very high for this time of year. Australian producers remain reluctant sellers of wheat at current values.