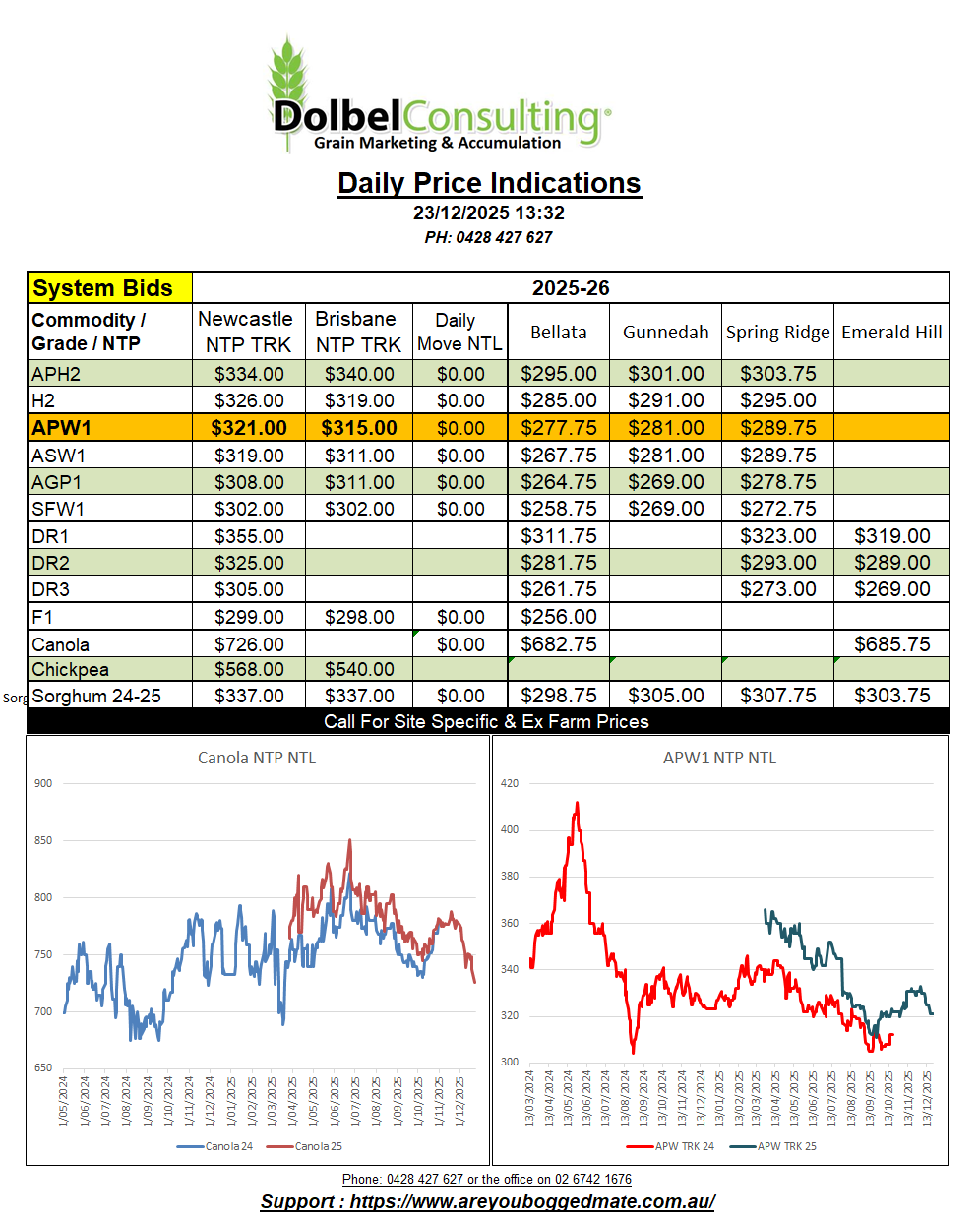

23/12/25 Prices

US wheat, corn and soybean futures found some upside over night. Can’t say it wasn’t needed. The sentiment rolled across to EU grain futures, Paris milling wheat, London feed wheat, Paris corn and rapeseed futures all closed in the green. I haven’t seen this much green on the board for a while.

The big mover was Winnipeg canola, up CAD$20.00/t (AUD$21.86/t) nearby, but also showing healthy gain across the outer months. Paris rapeseed moved higher, not the equivalent of the CAD$20.00 at Winnipeg, but did manage to put on E2.00 /t (AUD$3.53/t) in the May slot. Palm oil closed higher after the sharply lower close on Friday, up roughly AUD$11.05/t in the Feb slot.

Bargain buying, positioning prior to the break, parking money out of the stock market. Time will tell if this is a dead cat bounce or we have actually seen the bottom. The grain market is often used as a hedge against inflation, and the chatter is the US FED is going to start the printing press up again in Q1 2026.

International cash wheat markets were mixed, either side of unchanged by a dollar or two. US HRWW out of the PNW was up AUD$1.57/t on Fridays conversion. DNS and White Wheat out of the PNW pushed a little lower, -AUD$0.85/t and -AUD$1.83/t respectfully. The Black Sea milling wheat conversion was down a couple of dollars in AUD terms but flat in native currency. The 0.51% rally in the AUD is not helping.

Sorghum was a bit of a dark horse. It’s been running it’s own race pretty much lately, yes it is still influenced by corn but not as much as it used to be. US FOB values were up enough to counter the move in the AUD. The real mover was the Argentine value, that conversion improved by AUD$6.00 on last week. C&F China indicators were a little softer, but the process appears to be for Chinese numbers to catch up with western numbers on the following day, ie, today. It will be interesting to see if local values here improve, given the stronger Argie number. The Argie offer now US$8.00 over Aussie, and then + an 8.5% tariff.