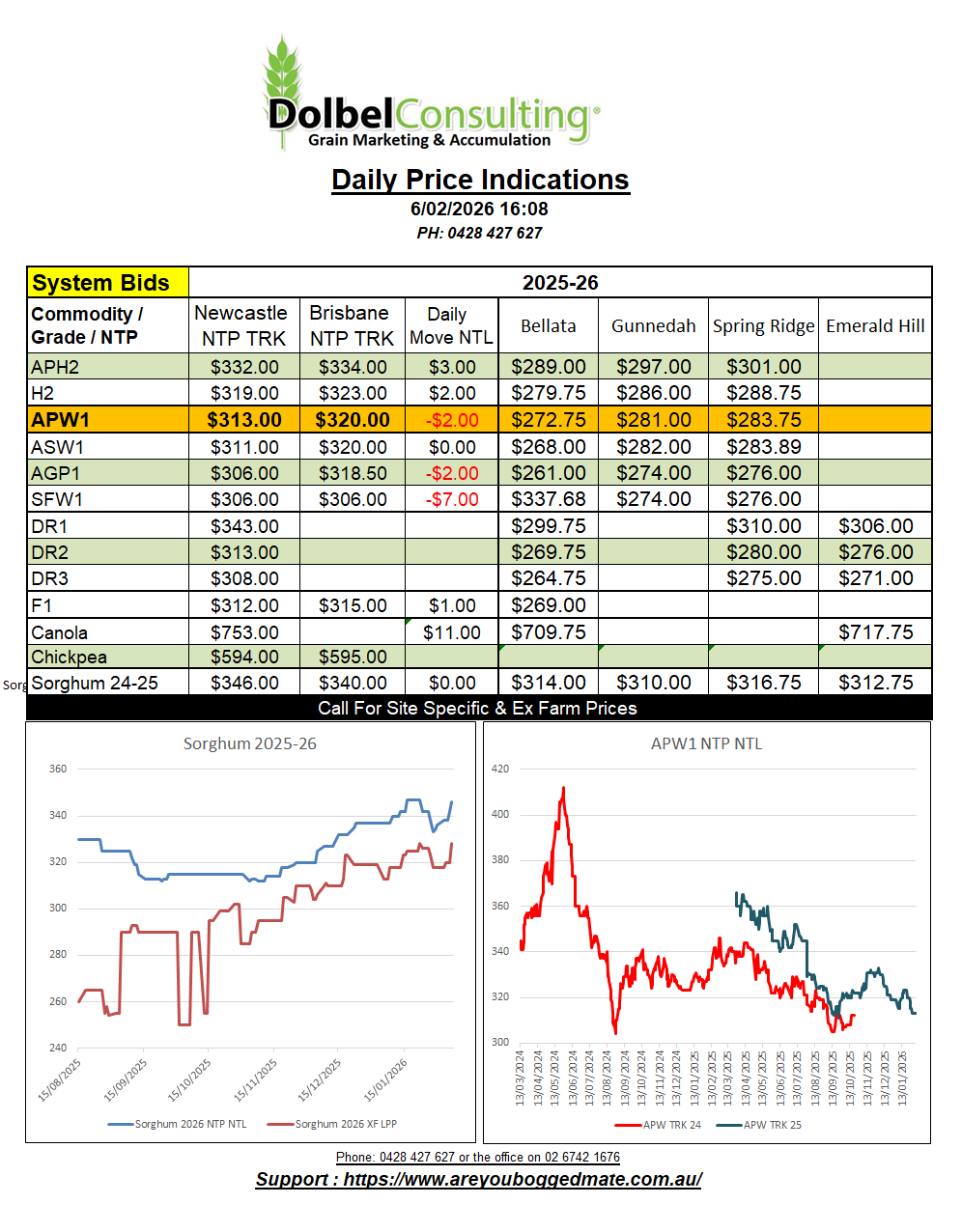

6/2/26 Prices

The strength is in the US soybean futures contracts at Chicago. The “Trump Bump” is the term now. This is adding some support to both grains and oilseeds. Both Paris rapeseed futures and Winnipeg canola saw half decent gains on the back of soybeans last night. Canadian canola is still surfing the wave of returning Chinese business, along with additional domestic crush demand. With the AUD off 0.53% against the USD this morning the moves in global oilseed markets should be reflected in local bids for both old and new crop today.

HRWW out of the US Pacific Northwest was higher day to day, the conversion comparison is up almost AUD$6.00 / tonne. Cash values out of the PNW for spring wheat and white wheat were also higher, their conversion comparison is up roughly AUD$5.06/t and AUD$4.46/t respectfully. This helps Aussie milling wheat be more competitive into the Asian market. HRWW now priced roughly US$8.00 under Aussie wheat. US white wheat into the Asian market is roughly within US$1.00/t of the Aussie equivalent.

There’s been some rain in Argentina. Conditions had become dry in parts of their sorghum belt. Roughly 60% of the Argie crop is grown across Southern Cordoba and Santa Fe and east into Entre Rios. Santa Fe and Entre Rios, where conditions have been very dry, is responsible for roughly 35% (1MT) of production. Rainfall over the last 30 days had only reached around 40% to 60% of the average for January in these two provinces. Temperatures have been 1C to 2C above normal prior to the last few days. Nothing like the heat being experienced across the NSW sorghum belt over the last 3 weeks, but yesterday many locations saw the mercury push above 38C in Santa Fe and Entre Rios. The forecast is for the high temperatures to reduce a little over the next 7 days. There’s a good chance storms will become active across the driest region early next week, producing falls of 25-50mm across the Argie sorghum belt. Sorghum values in Argentina have been stable this week at US$220 FOB river.