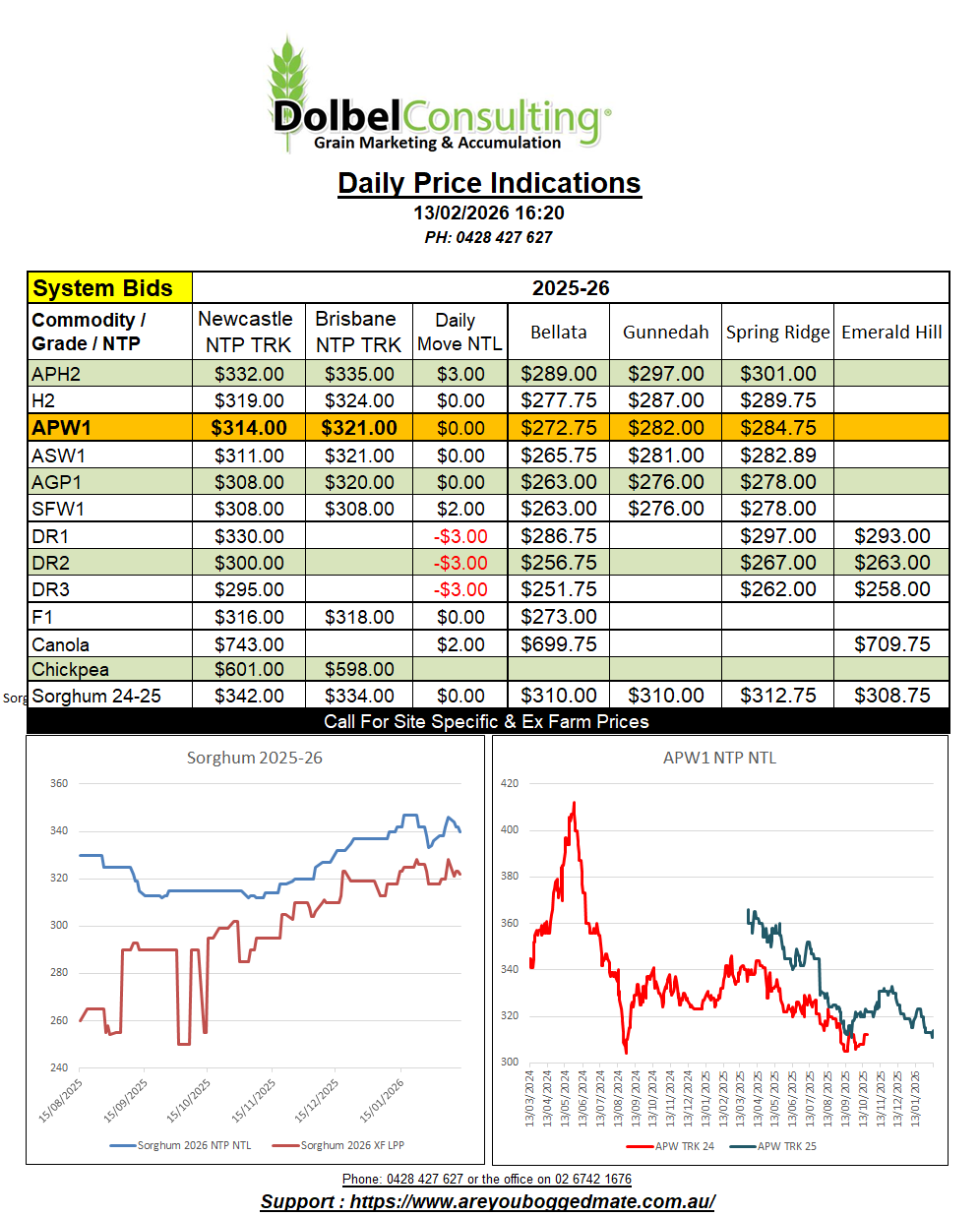

13/2/26 Prices

US wheat futures found some upside last night. The rally in futures spilled over into support for cash values out of the Pacific Northwest.

There’s not a lot of excellent reasoning in market wires to discuss the double digit rally in US wheat last night. US weekly sales for the week ending Feb 6th were OK. They were towards the higher end of trade expectations leading into the release of the report, but at 488kt the volume isn’t huge. It more than meets the weekly volume needed to cover the current USDA seasonal export projection, but it’s not excessive.

Could the punters be piling back into wheat as an inflation hedge, it wouldn’t be the first time commodities get overpriced by the punters when they run out of options to park money, and wheat is cheap.

International cash values certainly do not indicate that the US futures move was justified. The AUD has had more of an impact on the day to day conversion comparison than actual cash wheat values from all of the other major exporters bar the USA. The AUD move is equivalent to roughly +AUD$1.44/t.

Is it time to pull on the tin foil hat, probably not. Are we about to see a commodity rally like we have often seen prior to a general market collapse in the middle of year. I hope not. It’d be nice to think that the rally has some fundamental support, maybe some winter kill, or drought threat, but at this stage, middle of Feb, none of these things make a big difference until we get closer to ANZAC day.

Let’s hope the funds continue to cover their open wheat shorts at Chicago, dragging US wheat values higher, and our local basis is somehow kept at the current lofty values. Can’t see that happening without continued dry weather either.

Rapeseed and canola futures were also higher last night, drawn by a higher close in Chicago soybeans. Combined this with the weaker AUD and we should see some of yesterdays decline in local canola bids handed back today. Why US soybeans continue to rally is a gamble all of its own.