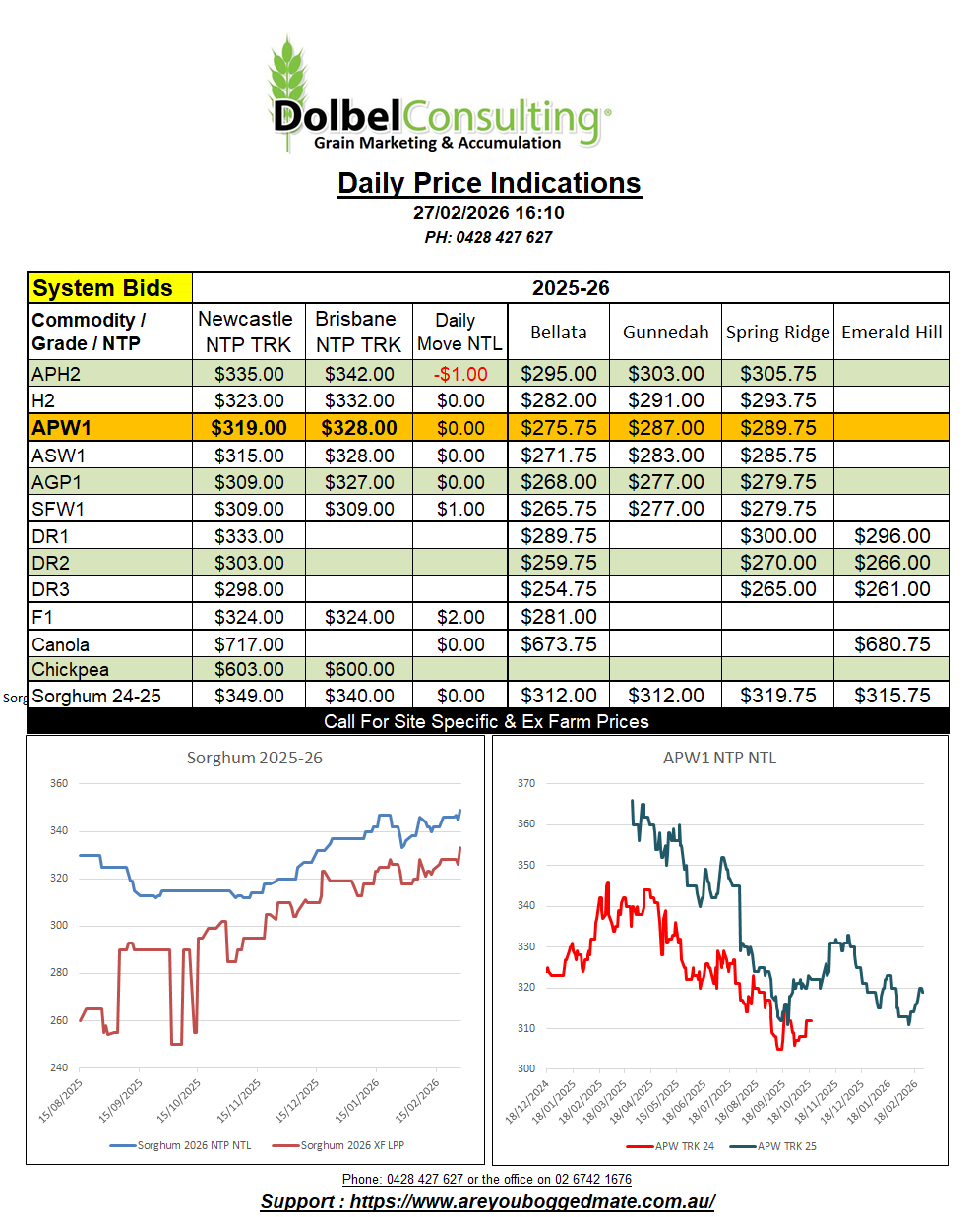

27/2/26 Prices

US weekly wheat export sales for the week ending Feb 19th were terrible, just 243kt, well below the average and highest trade estimates prior to the reports release. Obviously this data had little relevance to the futures market and nearby SRWW futures at Chicago rallied 6c/bu. Funds continue to reduce their net short in wheat. What the analyst call “uneven technical maneuvering”.

EU rapeseed production is set to increase as policy changes the dynamics of bio fuel there. The products that may suffer as canola or rapeseed benefit, include palm oil, soy oil to a lesser degree, and Chinese biodiesel due to EU import duties.

The EU is expected to increase rapeseed production to counter the reduced import volume of these alternatives. Increased production will need to see increased crush capacity. This is happening in Ukraine, but also needs to happen in more secure EU countries like Romania, where production is expected to spike. If the EU is to avoid a short term increase in stocks due to a lack of crush capacity, they need to look closely at either policy or crush capacity. Currently we see Paris rapeseed futures paying a premium for the nearby slot, May 26 €484.25/t versus, Feb 2027 @ €473.75/t and Feb 2028 @ €466.75/t.

Saudi Arabia are tendering for 655kt of 12.5% hard milling wheat for delivery May / July. We should see the results over the weekend, the tender closes 27th Feb, SA time.

Algeria picked up an estimated 600kt of milling wheat on Wednesday for delivery in April / May. The price was said to be around US$259 – US$260 C&F. This would place Black Sea exporters as the most likely point of origin. Argentina was not expected to participate due to shrinking availability, hard to imagine after their recent record harvest in December. At current values Argie wheat would have been +US$14.50 compared to Black Sea values C&F Algeria.