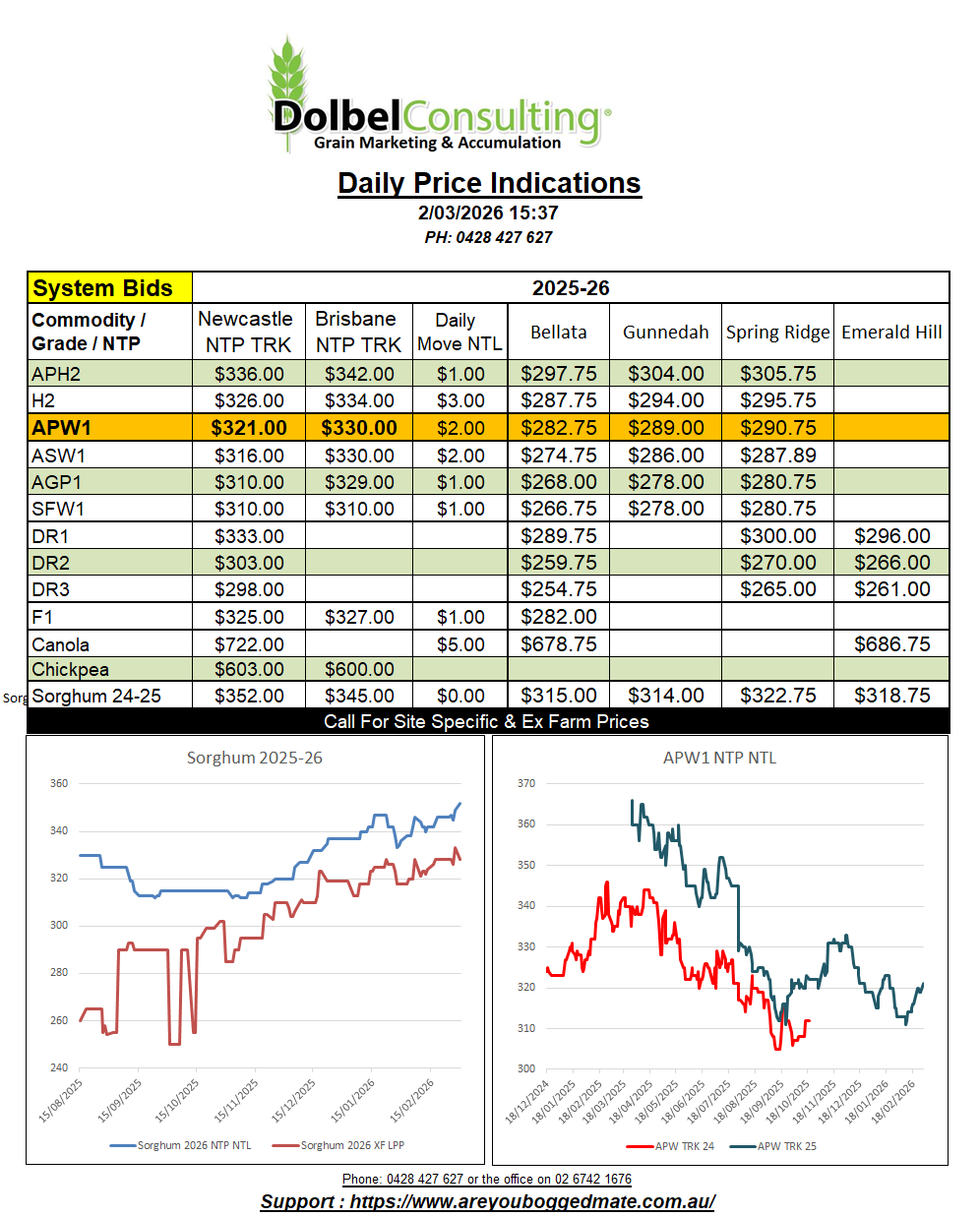

2/3/26 Prices

International wheat futures were firmer, Chicago, Minneapolis and Paris milling wheat contracts all finding good gains by the close. Is it sustainable, if you can show me a fundamental reason why this is happening, than yeah, we can call it fundamental, but otherwise it still appears to be technical in nature. Funds have been short for weeks, probably not the best position to carry into the winter thaw period in the northern hemisphere. Working out it’s very dry across eastern Australia isn’t rocket science at the moment either.

Paris milling wheat closed +€3.75/t to €201.50 / tonne in the May slot, March is irrelevant and about to roll off the board. Volume for the March slot is just 881 contracts at Chicago, May volume was 104,732 contracts, that’s 14.24mt. The rally in Chicago SRWW didn’t leave a gap in the charts either, starting from below yesterdays close.

The rally is equal to roughly AUD$10.00 per tonne. The question is how much of this rally is the local trade willing to reflect in old crop wheat prices here in Australia. Recently we’ve seen the trade more likely to reduce basis than track Chicago higher dollar for dollar. Fair enough too given the price difference between local and export values at the moment. The rally in US HRWW was reflected in cash values out of the Pacific Northwest. The change in the day to day conversion from PNW to Asian buyer and back to an Aussie farm equivalent price is roughly +AUD$8.54/t. This takes US HRWW on a C&F Asian consumer basis to about US$274, compared to H2 into the same Asian consumer at roughly US$280 (no tariffs, or margin over grower bids). The US product still has a slight price advantage, but it’s not huge. Any move higher in H2 here on Monday will simply increase that US price advantage. To be fair that price premium to Aussie wheat has been constantly above US$15 to US$20 for most of the marketing year now. Yes Aussie exports are slower than needed to meet annual export projections, but not by a huge amount. Sales are being made, but it’s hard going for the Aussie exporter.

International sorghum values were generally a flat to a smidge lower in origin currency but not enough to influence local prices, corn values were higher.