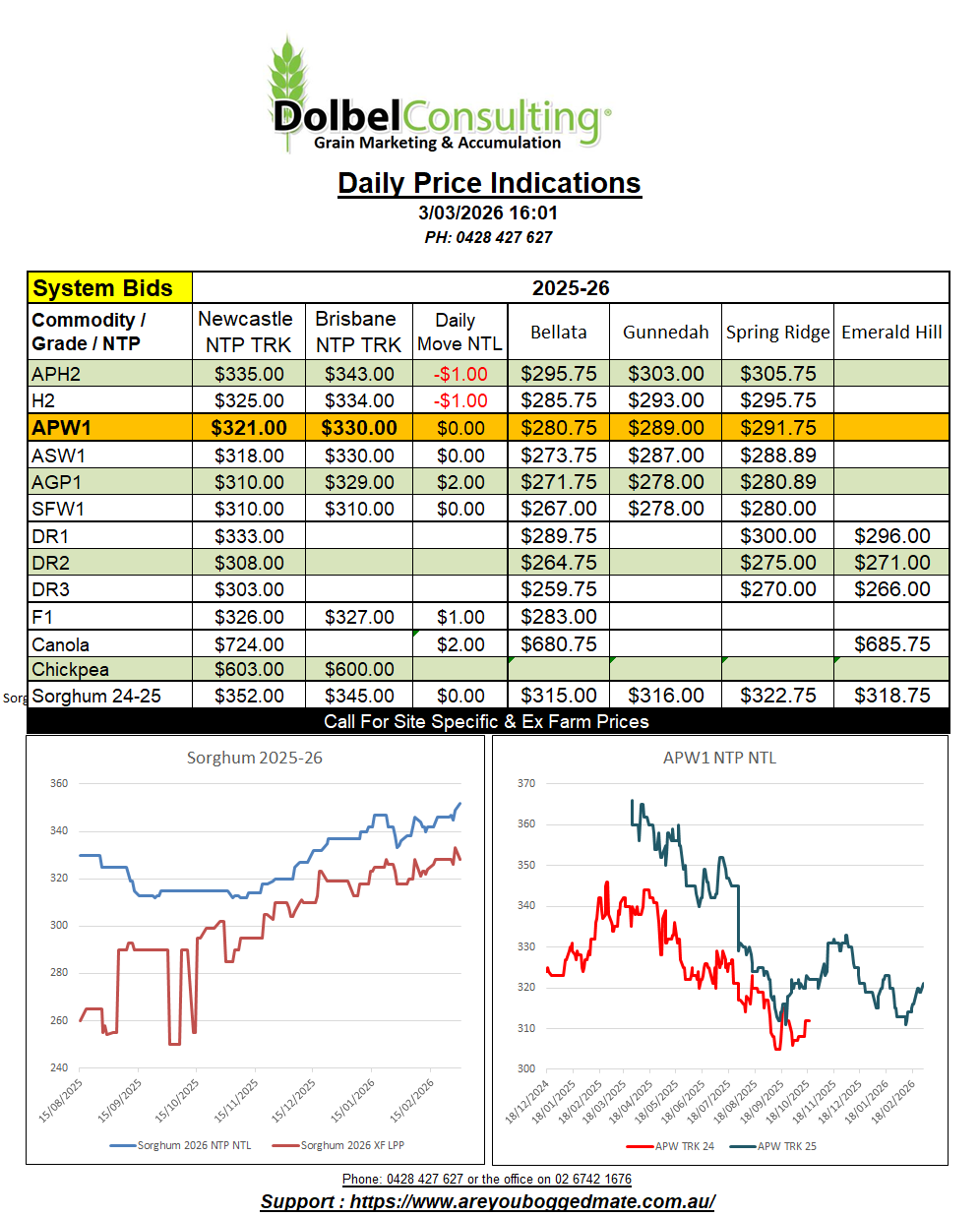

3/3/26 Prices

One week you have to be an expert on Venezuela, next week China, then global tariffs, then freezing rain in Russia, then blizzards in the US, then crude oil shipments from the Middle East, no wonder I have no hair. From a fundamental perspective the actions between Israel, it’s proxy, and Iran will have little impact on wheat. There’s a good chance that wheat will come in across their northern borders when required.

The payment of Iranian imports will be the issue, and this may take a while to play out. I’m sure they will work out an exchange rate at some point but with the Iranian wheat harvest about to start there will be speculation if current stocks can carry them through to when harvest begins in earnest in April / May / June.

The winner on the war at the moment, apart from the likes of Rathion and Boeing, is the oil futures punters and the insurance companies. Spillover buying from crude oil into oilseeds is happening, prompting good rallies in Winnipeg canola, Paris rapeseed and Chicago soybean oil.

For the farmer, the longer there are delays in passage of the Straight of Hormuz, the higher the chance you will see fertilizer prices increase. Not ideal for any part of the world at present, the southern hemisphere leading into winter crop sowing, and the northern hemisphere about to start spring sowing of summer crops. The issue appears to be the insurance side of the trip, once you get over the GPS interference. A lot of boats appear to be stationary as the owners negotiate the cost of insurance, and attempt to pass this onto the shipment owner. All in all, and at the risk of sounding like I’m glossing over the human cost of this war, the impact on ag markets is excitedly boring.

The Aussie dollar has done little against the USD, but has strengthened against most other currencies overnight. One can’t help but think that the war will increase local fuel prices, feeding inflation, thus encouraging higher interest rates from the RBA. It’s a cruel world. If the war goes longer than the 4 weeks Trump is suggesting, which in reality it is probably more than likely to. Then we’ll probably see the US printing presses start up again, feeding longer term inflation in the US as they work on debasing the USD yet again.