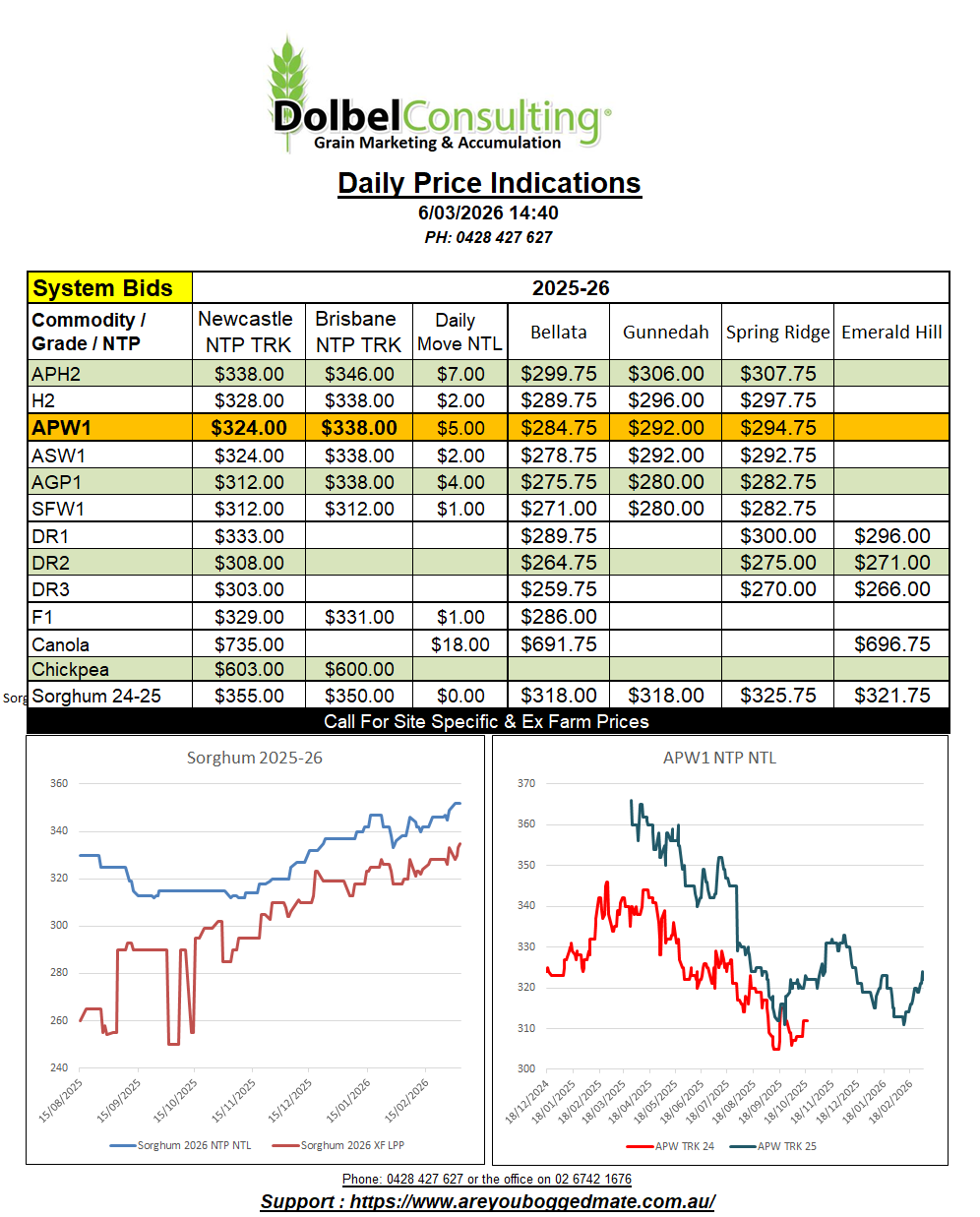

6/3/26 Prices

Both Chicago soft red winter wheat and hard red winter wheat futures saw double digit gains overnight.

There’s no fundamental reasoning for this rally. Weekly US sales were not great, 203.1kt, that’s towards the low end of trade estimates leading up to the report which ranged from 200kt to 500kt.

StatsCan data came out with an all wheat planting intentions number of 26.74 million acres, spring wheat pegged at 18.87 million acres. That was above trade estimates, but also -1% below last years area. The big move is a -7% fall in the winter wheat area. Chickpea area is expected to grow 6% to 575kac, barley is expected to increase 5% to 6.44 million acres. Summer fallow is expected to increase 11% (low prices fix low prices). The big fall in area is dry beans and sunflower, sunflower area is back 13% to just 66kac.

The move in US wheat futures could be a couple of things, neither of which are fundamental in nature. We have the US FED talking possible inflation again. In the past we’ve see the punters jump into grains as an inflation hedge. We also have the last of the speculative shorts trying to exit the market. The last couple of weeks had seen an orderly exit of short hedge positions, considering the volume held. We could possibly be seeing the last of the punters now exiting in a less than orderly fashion.

Cash wheat values out of the US Pacific Northwest were higher. In the case of HRWW even higher than the futures market may have indicated. Compared to yesterdays conversions we have white wheat up just over AUD$5.00/t, HRWW up AUD$14.49/t and spring wheat up AUD$9.48/t. The lower dollar is helping. If we look at C&F Asian values compared to yesterday (but reflecting last weeks ocean freight rates), we see H2 now roughly the same price as US HRWW. This is excellent news, and if sustained should see Asian buyers looking much closer at Aussie offerings.