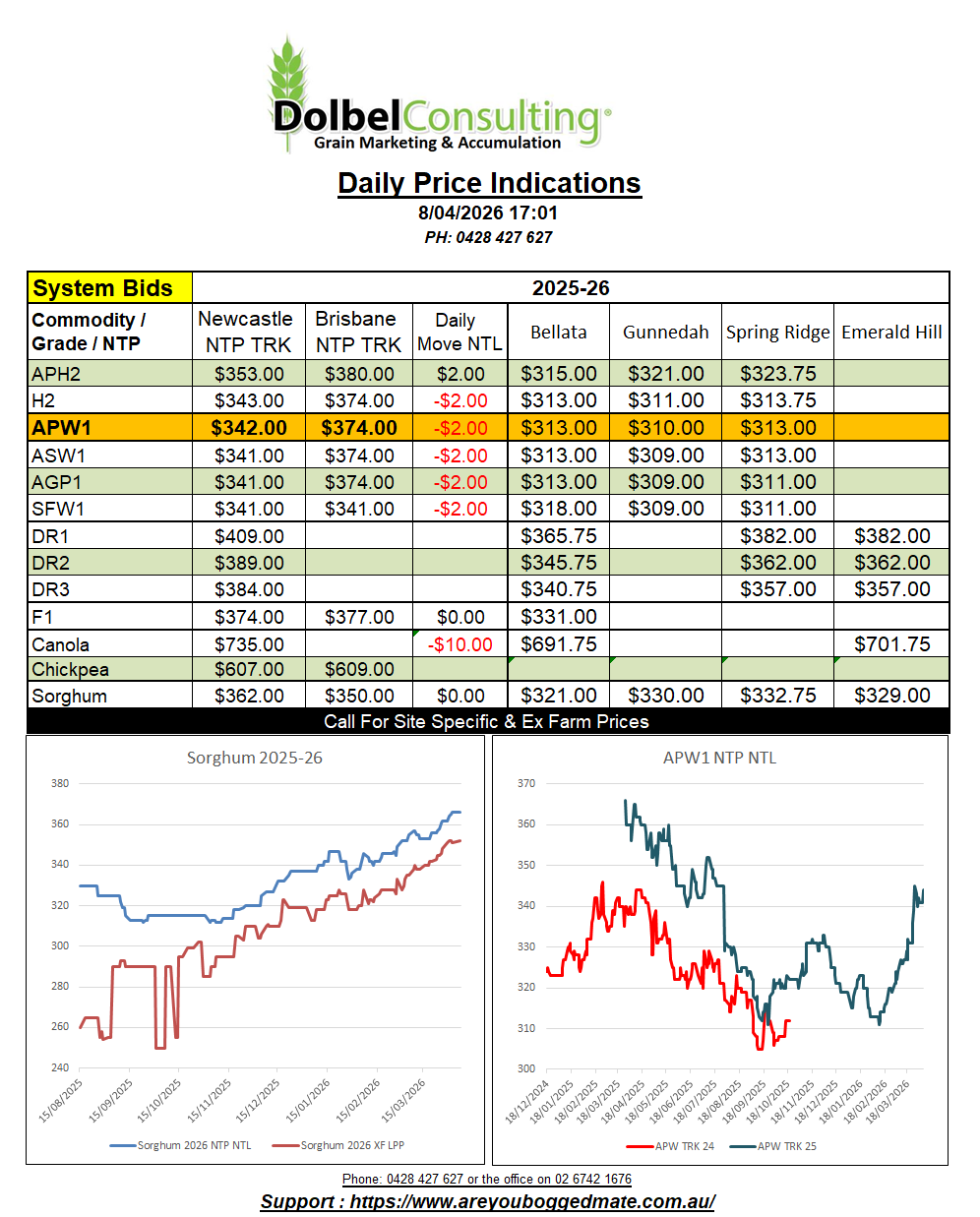

8/4/26 Prices

We have a USDA World Ag Supply and Demand Estimates report due out on Thursday, US time. We should have some data to look at on Friday morning. The punters are not expecting to see huge changes. Much of the data is collated up to 30 days prior to the release of the report, and a hell of a lot has happened over the last 30 days.

Cash wheat values out of the US Pacific Northwest were lower in USD FOB terms. The day to day conversion comparison is also lower. Assisted somewhat by the stronger AUD. The drop is roughly AUD$3.00 to AUD$5.00 per tonne. Comparing H2 and HRWW into the Asian market we see that HRWW is roughly US$11.00 cheaper than H2 now, a big turnaround from early last week. This may weigh on Aussie export opportunities.

Local Aussie basis, east coast, remains strong. Local producers holding tight to old crop stock as weather conditions continue to deteriorate. NNSW is drier than the lead up to the last record breaking drought. Many locations across the LPP seeing less than 30mm of rain since mid January. Add to that persistent hot weather and we see subsoil across much or NNSW and SQLD is now depleted.

During a call yesterday it was stated that if there was ever a good time to have a drought it may as well be now while everything is too expensive or hard to get. Personally I tend to think that there is no good time to have a drought, but you can see the logic in the statement.

Argentine milling wheat values are higher week on week. The move putting Argie wheat well above both Aussie and US milling wheat into the Asian market. This should assist US sales that had been falling behind the stronger average pace a little over the last few weeks.

SovEcon reduced the projected wheat production number for Ukraine by 1mt. High input costs the key to the decline. We need to see global wheat production fall by 30mt to 40mt to have any fundamental impact on prices longer term. That’s a global production estimate under 800mt, realistic?, probably not.