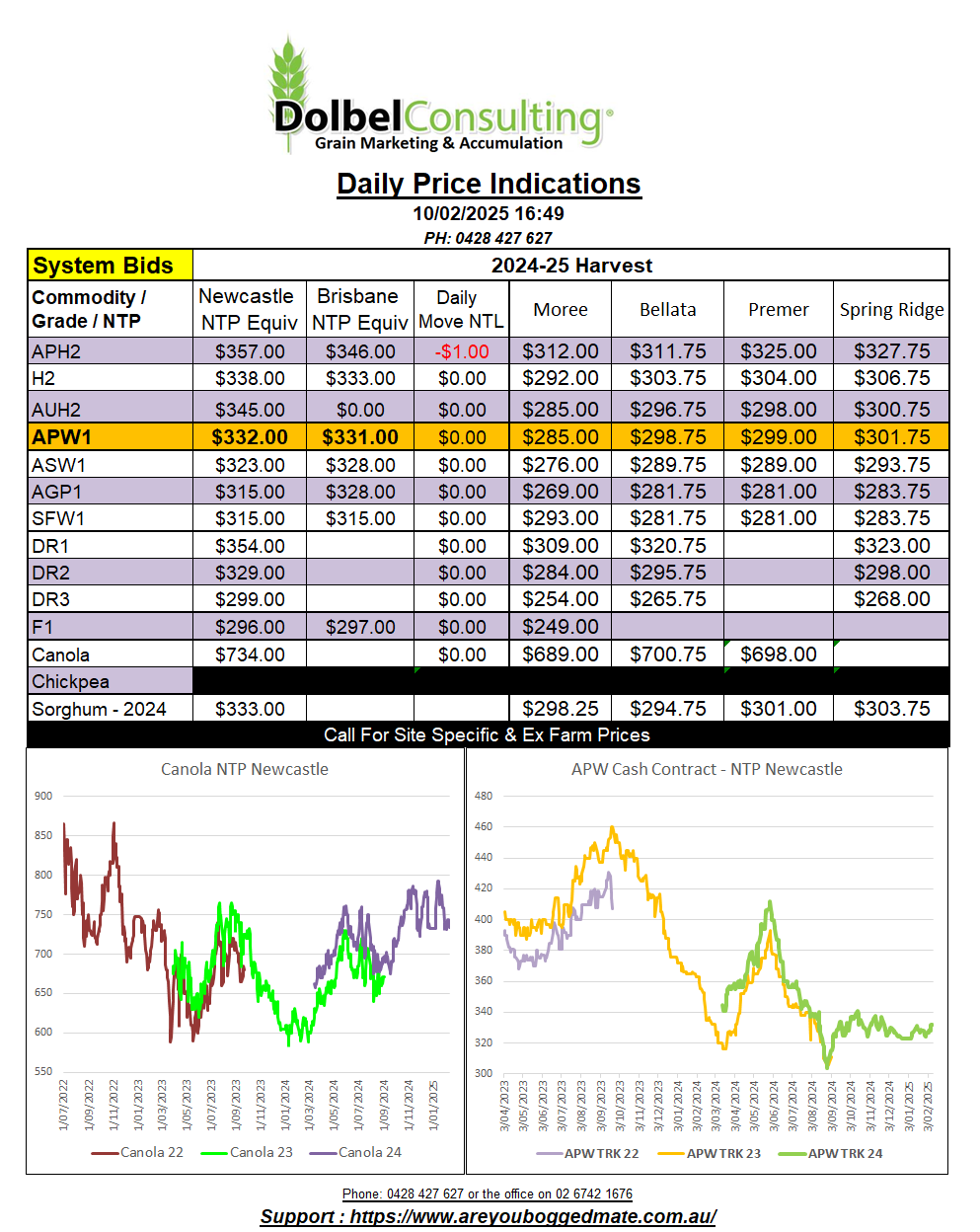

10/2/25 Prices

All major world grain futures markets were softer overnight, bar Winnipeg canola. Not sure what that’s about, maybe they are just happy they are still not part of America. Chicago wheat, corn and soybeans all closed in the red. Wheat handed back a slice of yesterdays sharply higher close but has still managed a week on week gain of roughly AUD$13.62 / tonne for nearby Chicago SRWW, while local prices here moved high by AUD$5.00.

Paris rapeseed followed Chicago soybeans lower, shedding €6.25 per tonne in the May 25 slot, and €2.25 per tonne in the Feb26 slot. Maybe Winnipeg was more interested in what was going on in palm oil futures than in EU rapeseed or Chicago soybeans. The March 25 palm oil contract closed 93 MYR/tonne higher and the April slot was up 101 MYR / tonne (AUD$36.29). WTI crude was also a little higher gaining 41c/b to close at US$71.02/b nearby.

Cash markets were flat to softer. Canadian values for milling wheat out of the Pacific Northwest were flat. US wheat out of the PNW followed futures lower shedding a couple of AUD/t compared to yesterdays conversion. Black Sea values were mixed, Russian prices were flat when converted and Ukraine values were actually a few dollars higher. French milling wheat followed the lead from the US and pushed lower, shedding about AUD$5.75 from yesterdays conversion.

Grain market commentary runs the risk of becoming stagnate or uninteresting during this time of year. With northern hemisphere crops in dormancy or spring wheat yet to be sown and the southern hemisphere harvested or yet to be sown. The main drivers are trade shorts or unexpected consumer interest. Neither offering any long term support or guidance to the market. The next USDA World Ag Supply and Demand report is out on Feb 11th, next Wednesday our time. We may see a little speculation on Russian stocks and Chinese imports in this report but seriously no one is expecting to see a market mover.