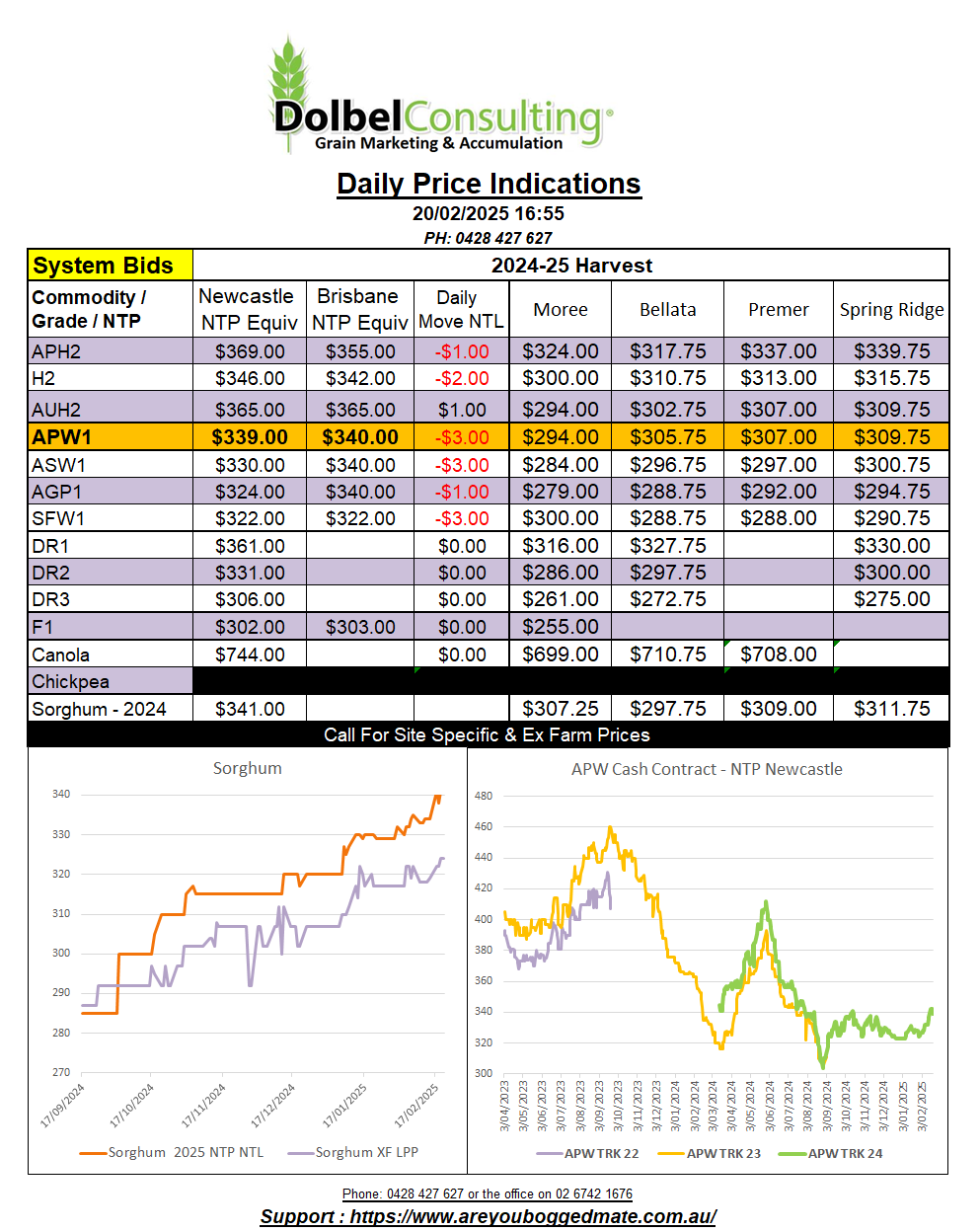

20/2/25 Prices

US wheat futures gave back a slice of the recent rally overnight.

Nothing has changed a great deal from a fundamental perspective. NW Kansas is seeing temperatures down around -20C. Further south towards the Oklahoma border overnight minimums were around -15C +/-, which is very cold. The snow cover map now shows most of Kansas has 2″ to 4″ of snow cover, as does NE Oklahoma. This may limit the chance of winter kill but we’ll need to wait this one out to see. One might expect to see some damage around the panhandle come spring.

The US futures session was seen by many as some short term profit taking. Many punters continue to talk US wheat futures higher on the back of two hard freezes in the US this winter, and the cold, dry weather in Russia.

The fact that Russian wheat exports are actually increasing again is not exactly backing the theory that the Russian winter wheat has been as hard hit as some are suggesting, but I guess we all need cash. Old crop Russian wheat exports may decline in coming months as we lead into their new crop and the export quota system limits exports to 10.6mt, or according to Rusagrotrans potentially no more than 8.1mt from this week.

The quota portion of this years marketing season commenced as of the 15th of Feb and runs through to the 30th of June, roughly 19 weeks, or 549kt/wk on average, not exactly poor weekly export capacity either. If Rusagrotrans is correct this could be on average closer to 420kt/w.

Paris milling wheat took the lead from US markets and also slipped away, shedding €1.50 / tonne nearby and €1.00 / tonne in the Dec slot. Generally most grains were lower. US corn and soybeans also shed value while Winnipeg canola was slightly higher, Paris rapeseed was mixed, nearby lower but outer months were a smidge firmer. Palm oil futures lost value, shedding much of the previous sessions gains.

International sorghum values were flat while international feed barley values were roughly AUD$1.00 lower from the major exporters.