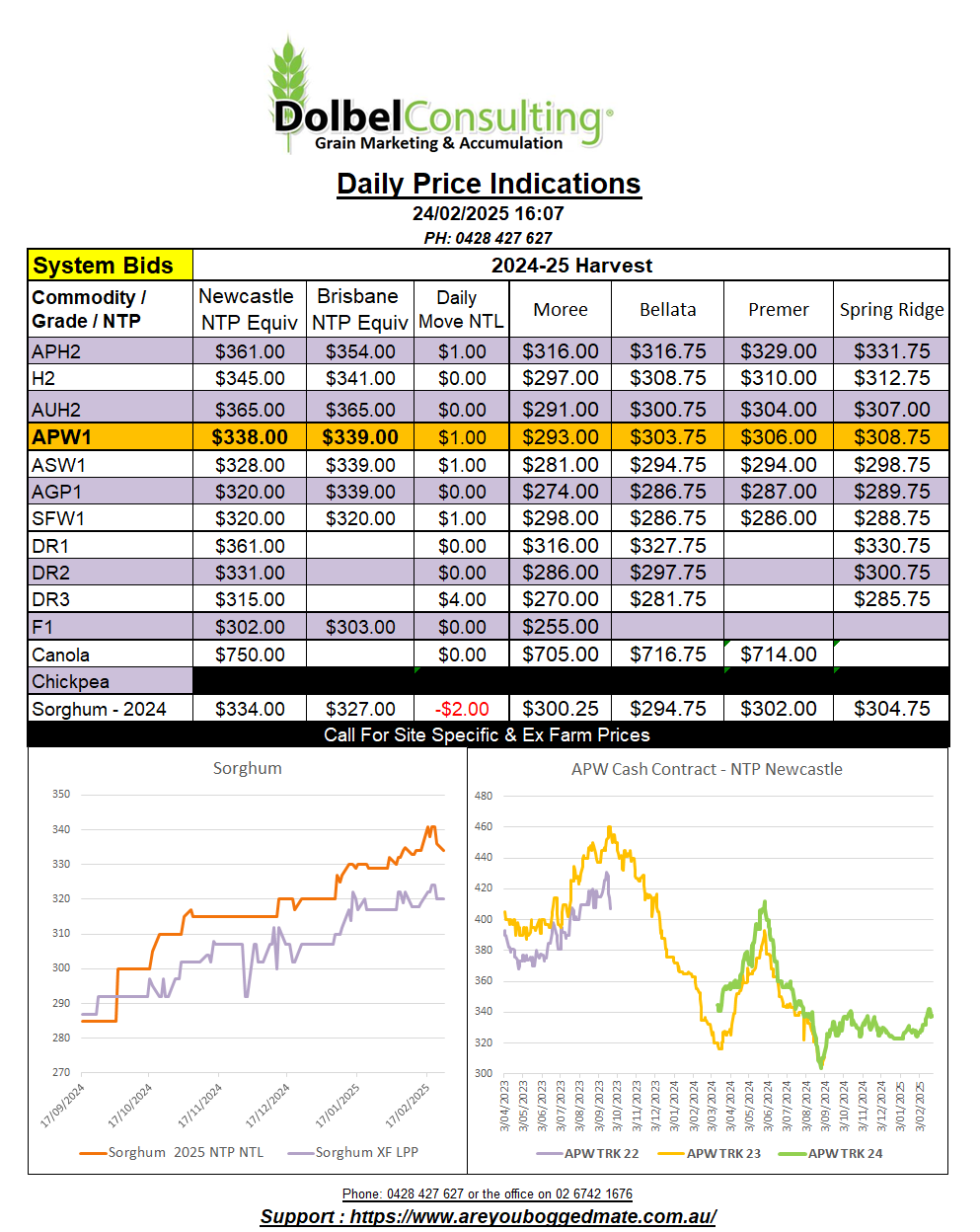

24/2/25 Prices

US futures were mixed, wheat tried to take back some value, succeeding in soft and hard red winter wheat futures but failing in nearby spring wheat futures. Either way the move in wheat was against the flow in corn and soybean futures, both shedding value and weighing on the Paris rapeseed and Winnipeg canola markets. Paris milling wheat also shed value, down €0.75/t nearby and €0.25/tonne in the Dec 2025 slot. The weaker AUD is taking care of these minimal losses.

The international cash markets for wheat were generally firmer. In the case of France values moved in the opposite direction of the futures market and made some significant gains in comparison to yesterdays conversions. US (not Canadian) wheat out of the Pacific Northwest more closely reflected the Chicago and Minneapolis futures markets. White wheat was unchanged in USD, the weaker AUD resulting in a net change of +AUD$3.02 / tonne for WW compared to yesterdays conversion. Hard red wheat was AUD$4.26 / tonne higher and spring wheat was also higher than yesterdays conversion, adding roughly AUD$2.72 / tonne. Canadian upcountry wheat was higher but once converted to USD Asian buyer > AUD NTL equiv, is actually a couple of bucks lower.

There is now little difference in price between US HRWW and Australian H2 wheat to the Asian consumer. With white wheat the better milling wheat one would think that Aussie wheat should continue to have the advantage, even if it is a few dollars more expensive.

US net grain export sales for the week ending Feb 13th were again very good. Wheat came in at 533kt, corn 1.454mt and soybeans 480kt, all higher than this time last year and all towards the higher end of the trade estimates leading up to the report. Net sorghum sales improved over the 4 week average but were down 59% from last week, at 21.7kt. Mexico took the lions share of sorghum, helping to negate cancellations from China. FOB sorghum values out of the Gulf of “Mexico” were slightly lower, as were C&F China values.