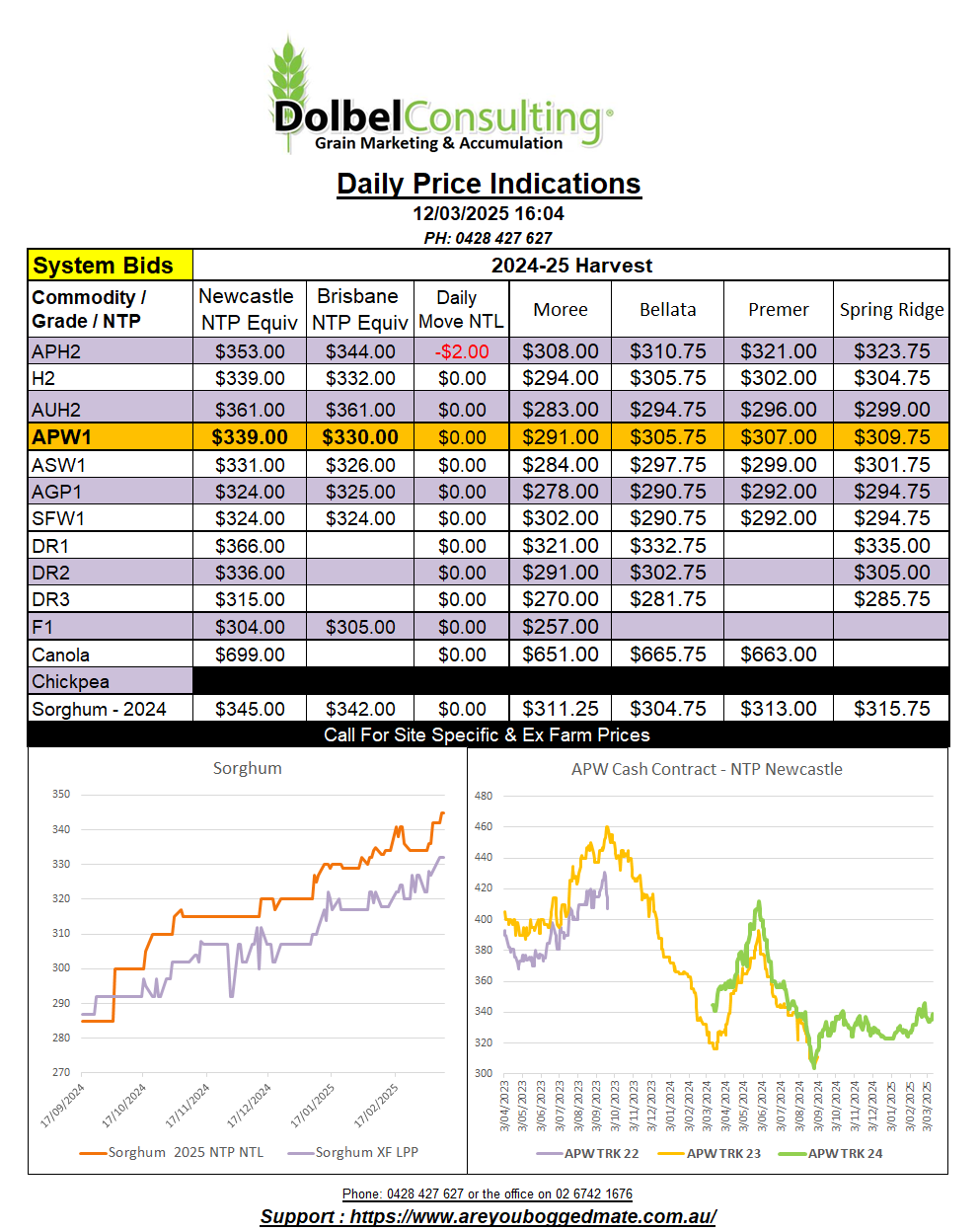

12/3/25 Prices

The USDA World Ag Supply and Demand Estimates report (WASDE) was out last night, hanging a wet blanket over the wheat market. Looking at the data the thing that sticks out the most is the increase in both opening stocks and closing stocks. The net result a month of month increase in the carry over stocks of 2.52mt to 260.08mt. A stocks to use ratio of 32.24%, still way to high to see a significant rally in wheat. To get the S:U ratio under 30% we’d need to see carry out reduced to something close to 241mt. A 20mt reduction is significant and we’d need to see some big adjustments to supply for a fall of this magnitude. Not impossible. Looking at carry out from 2022-23 at 276.14mt compared to carry out in this report at 260.08mt, that’s down 16.06mt in two years, without any huge issues around the world (the EU may argue that point).

Drilling down into the wheat table we see adjustments to Aussie production, up from 32mt to 34.11mt. Aussie exports and domestic consumption were increased a little to counter the production increase but carry out was increased 610kt to 3.22mt, still pretty low.

The bulk of the increase in world ending stocks was in the major exporters, Black Sea (Russia / Ukraine) ending stocks increased by 1mt. Russian production was increased 100kt and exports reduced 500kt. Ukraine production was increased 500kt, increases in Ukraine domestic usage helped counter that a little.

Argentine production was increased 800kt to 18.5mt, that rolled straight across to their ending stocks. This increase could be questionable given their season.

Brazilian imports were increased 100kt to 6.5mt. Chinese imports were reduced from 8mt to 6.5mt, with Chinese consumption unchanged this resulted in a 1.5mt draw down on ending stocks for China. Now estimated at 129.1mt, representing just 49.63% of world ending stocks……

Indian production was left at 113.29mt, Indian consumption 112.24mt and ending stocks of just 8.5mt.

In summary the report is not bullish wheat and may cap old crop values in the short to mid term. The volatility in wheat for 2025 will come from production issues in the northern hemisphere over the next couple of months. With dry weather in both Russia and parts of America there’s sure to be some volatility.