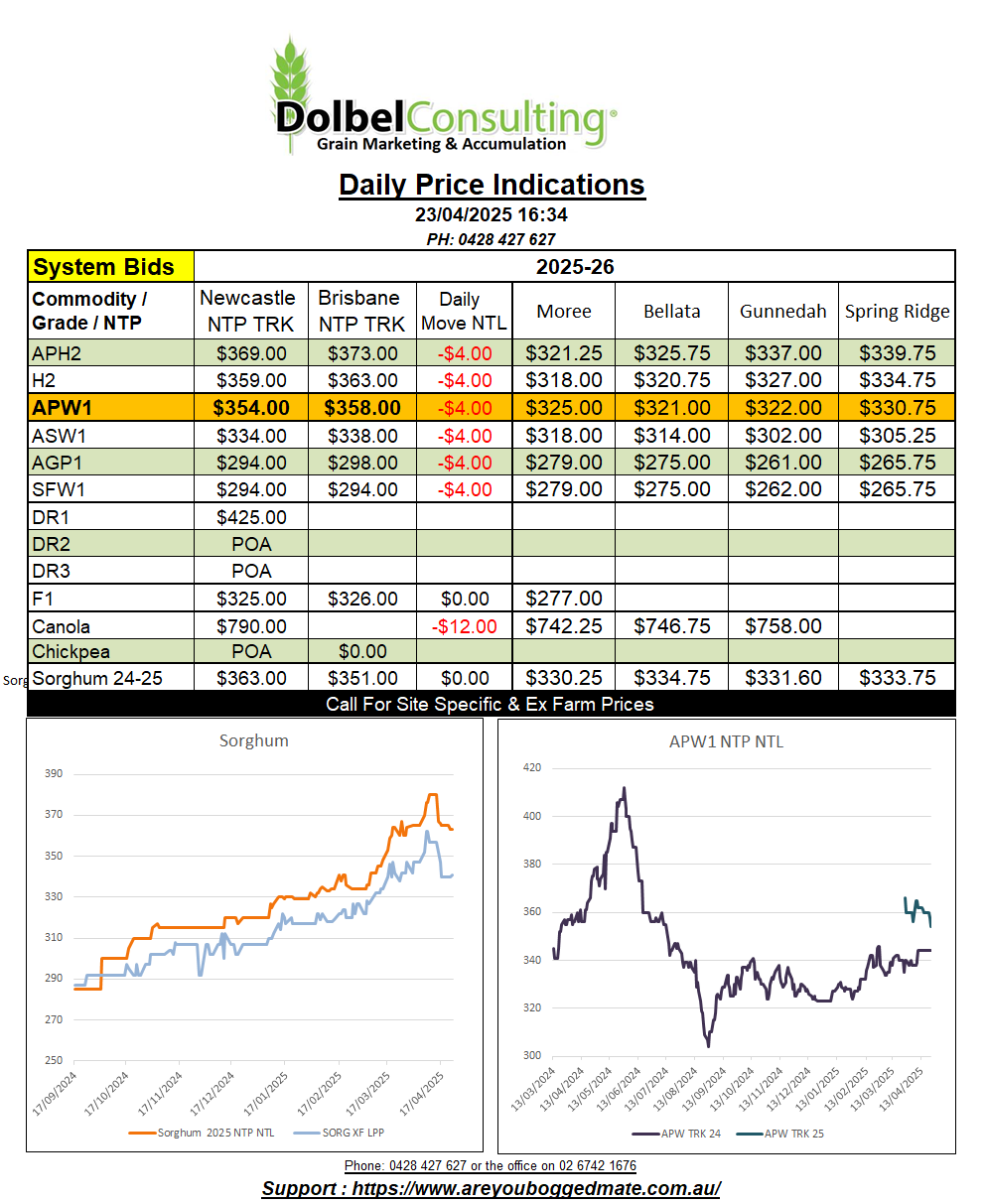

23/4/25 Prices

International wheat futures were sold lower overnight. US and EU futures markets shed value, the EU markets were sharply lower. Paris milling wheat shed €2.75 / t nearby and €4.00 / t in the December slot. One of the harder hit contracts was London feed wheat, back £5.40 / tonne nearby and £3.35 in the January 26 slot. The trend in futures spilled into the cash markets, Black Sea values were lower, FOB France, and US values were also lower in native currency.

Looking at cash wheat out of the US Pacific Northwest we see HRWW, once converted to a delivered Asian buyer value and then converting that value back to an equivalent value here, using spot currency, it is roughly flat. The only grade of wheat out of the PNW using the above day to day comparison that was lower by more than a dollar was club white wheat, back -AUD$1.31 / tonne. Canadian spring wheat, using the above comparison is actually higher by roughly AUD$2.65 / tonne, even though the CAD price is on average lower by C$1.12 / tonne ex farm SE Saskatchewan.

The AUD found weakness as trade tension between the USA and China appears to be…… less tense. The improvement in the USD and the prospect of inflation in the USA, versus deflation here in Australia, has the two currencies in a mid to longer term opposing trends. The US FED continue to suggest that any inflation created by tariffs is likely to be contained using higher interest rates. Here in Australia the RBA may have little choice but to continue to lower interest rates in a half baked attempt to stop the economy slipping into a full blown melt down. I’m not convinced either the blue tie man or the red tie man have the capability or the desire to fix the local dogs breakfast left by the covid debacle, etc etc. Thus there’s probably a good chance that local interest rates will stay lower or be lowered for some time. I’m no currency trader but I’m not about to back interest rate increases here either.

Back in the grain world we see domestic wheat values in Russia slipping lower, stimulating exports. Improvements in the outlook for both the Ukraine and Russian wheat crops, plus additional Russian wheat coming back into the market will continue to weigh on international values mid to longer term.

Local markets were dead. Sorghum found seller resistance at current bids and old crop wheat was held close by the seller.

Locally old crop unsold wheat stocks on farm are very low. I have buying interest for both ASW and SFW1 above the public bids but continue to struggle to fill local slots with local grain.

The falling track value is helping the trade to execute system stocks. There is also the thought that stocks being held through to the new financial year will soon make their way onto the market. For the sake of the exercise ASW at Gcorp Walgett was bid at $285 delivered site yesterday. To execute this by road and move it into the Liverpool Plains consumer market would cost the buyer roughly $352 delivered, plus trade margin if applicable. Yesterday we saw local ASW end user bids closer to $340. So still some plausible upside in the wheat bid yet.

Sorghum was bid at $360 NTP NTL on the track and $385 delivered Newcastle port by road. Both these markets have fallen away from the recent highs as the AUD improved. The weaker AUD today should counter further declines in the international sorghum market on average, but even with the weaker AUD, USD prices are still back by just less than a dollar out of the Gulf. The trade were happy to look at offers yesterday but were not willing to bid the market higher in a generic manner. This may lead one to think that the seller resistance is working, and grower volume has slowed enough to try and put a floor in the price.

The weaker AUD appears to be solely related to the de-escalation of trade issues between the US and………well…. everyone. Is the red man back in his box.