19/5/25 Prices

US wheat futures fell moderately lower overnight. Bearish data from the US hard red winter wheat crop tour was said to be part of the pressure. The 3 day tour wrapped up with an average Kansas wheat yield estimate of 53bu/ac, 3.56t/ha, not huge, but it’s actually a 4 year high for Kansas. Total Kansas wheat production was estimated at 338.5mbu, 9.21mt. Not bad for a state about 9% smaller than Victoria which grows about 3.9mt.

Total year to date export sales for the US wheat crop now stands at 21.689mt. This is roughly 97% of the USDA projected sales for the marketing year which ends in 3 weeks.

France reduced the good to excellent rating for their soft wheat crop to 73% G/E. Although this is back 1pt week on week, many had expected to see a sharper fall. This opens the door for a further decline next week. According to WorldAgWeather.com 14 day totals for northern France are less than 5mm and things are not much better for NW Germany. The 7 days forecast for northern France shows the chance of 5-10mm of rain around the middle of next week. Germany is expected to see some better falls towards the east of the country late next week. All is not rosy for the wheat crop in Europe and a G/E rating of 73% may be over stating the potential quality of the crop for now.

Rainfall is expected across much of the Russian and Ukraine winter wheat regions next week. Showers are also expected to return to the spring wheat regions of both Russia and Kazakhstan. Turkey is expected to remain mostly dry, a condition Turkey has had to deal with most of this season. Irrigated durum in Turkey remains in great shape, but reports of much lower yields than last year for dry land crops have some thinking that the durum aggressive export program that Turkey pursued last year will not be repeated this year. Durum harvest in southern Italy is underway between showers.

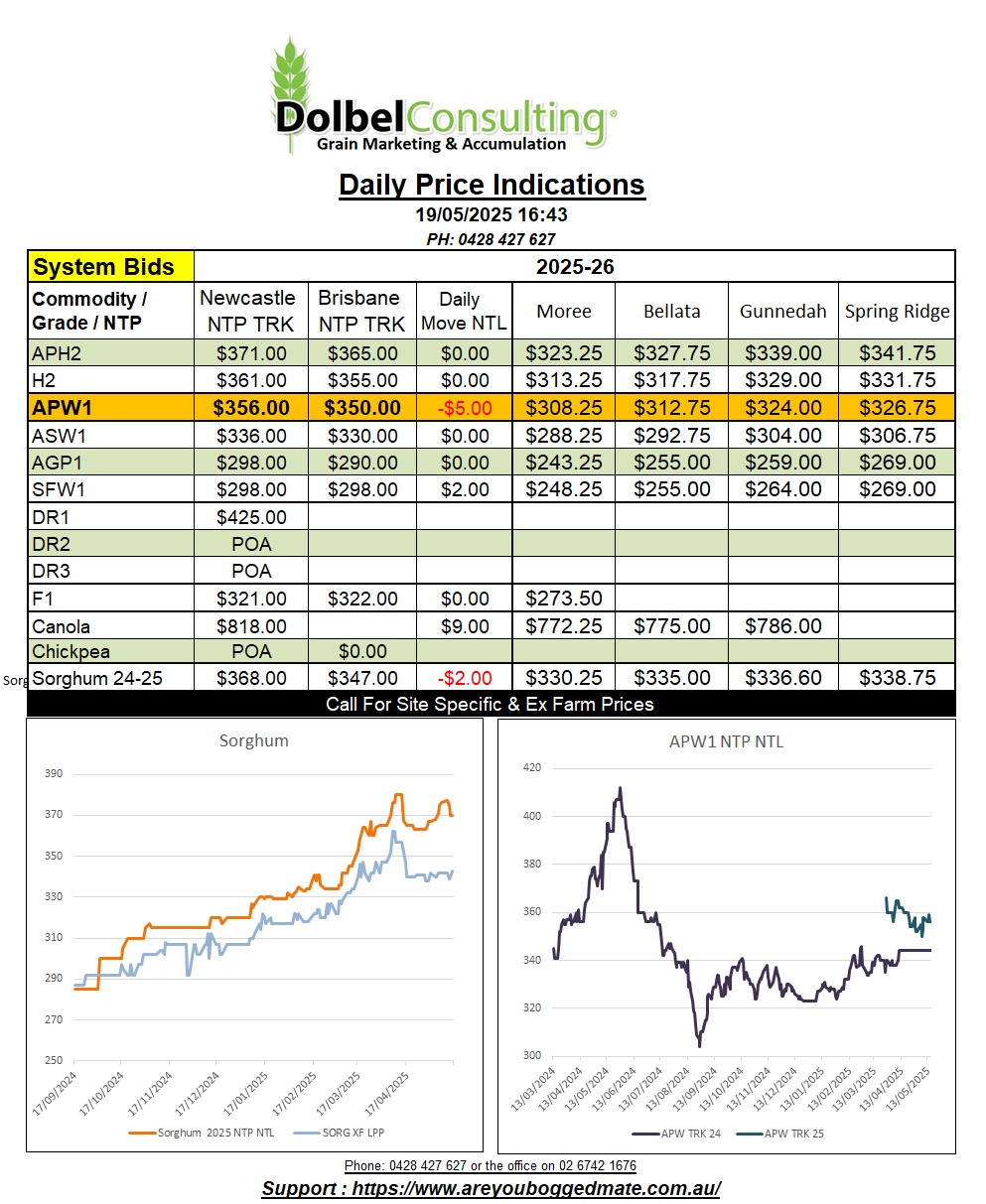

Sorghum values were flat to firmer. Grower selling has eased, producers are busy with the logistics of executing existing sorghum contracts, sowing winter crops and picking cotton. This has seen the bid for Newcastle port by road climb back to $388 delivered June / July. There was interest in buying sorghum on the track, but selling has stalled after values slipped earlier this week. Many traders pulled bids back as the AUD improved, unusual for the middle of the month but this may enable the trade to compete once grower selling picks up again. Keep the offers high but it’s becoming a very fickle market.

Overnight international sorghum values were generally a smidge lower. US FOB offers were flat to AUD$1.50 lower, while CiF China values slipped by less than a dollar.

The AUD closed where it opened after setting a mid session low of 63.89 and bouncing in the afternoon. The AUD continues to be used by the punter as a proxy trade for the Yuan. Not ideal as the recent trade deals done between the US and China will help the AUD in the longer term if the punters back the Yuan / AUD. A move higher in US interest rates now seems less likely as the US GDP contracted 0.3% in Q1.

Locally a weaker currency would help exporters, thus pulling the economy higher “naturally”. If the AUD moves higher as a Yuan proxy this is little counter intuitive for the Aussie economy. A strengthening AUD will thus make Aussie exports less attractive, possibly stifling what may have been a quicker recovery being helped along by the weaker AUD. Will the RBA reduce rates locally to counter this, I doubt it.

With both Winnipeg canola and Paris rapeseed bouncing after yesterdays hard sell, we may see a slight recovery in canola here on Monday.