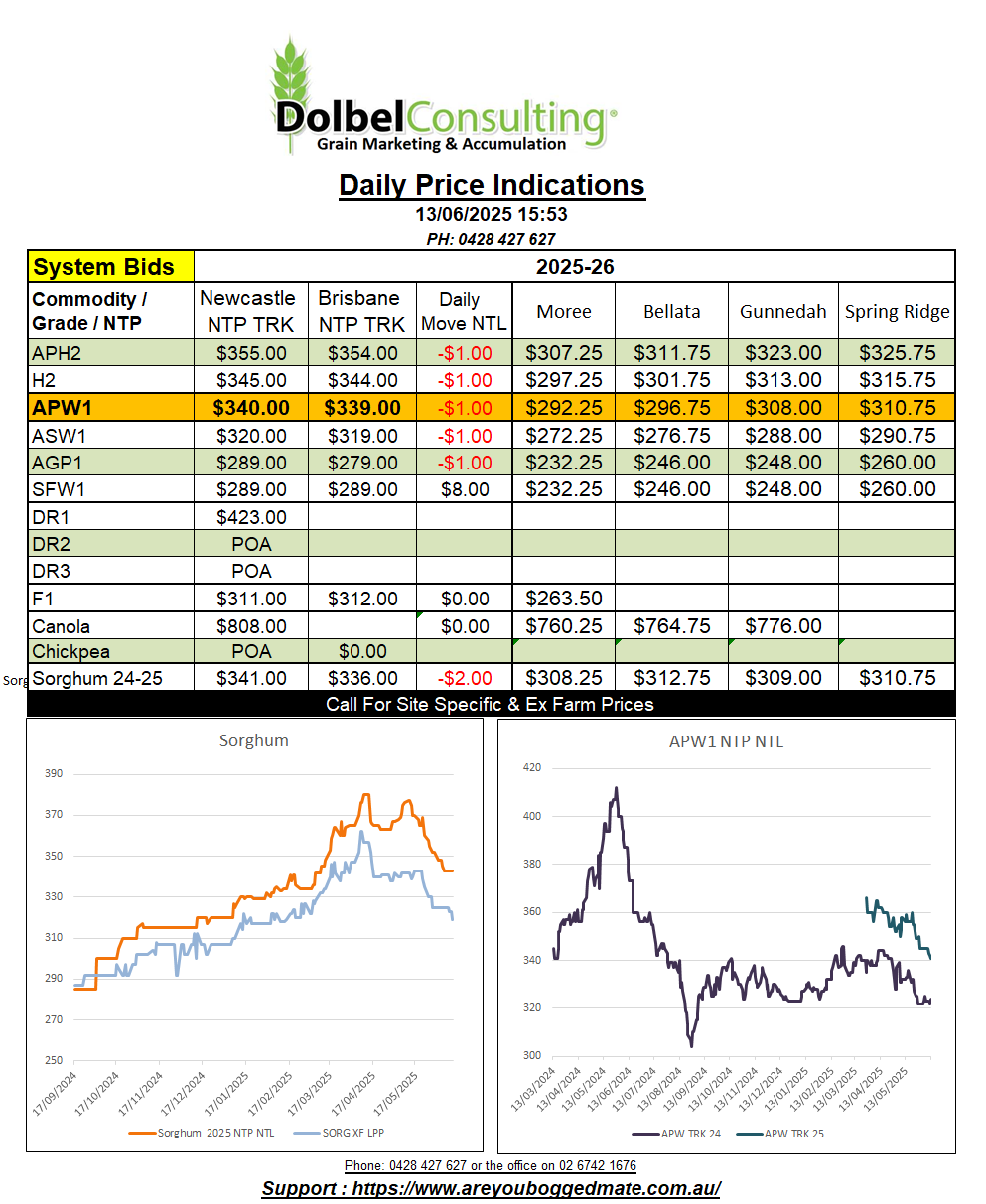

13/6/25 Prices

The June WASDE was out last night, something for the market to ignore when it comes to wheat. The data is more bullish wheat than bearish. Opening stocks are lower by 1.23mt, global production was increased a smidge, a few tweaks to demand, a 1.34mt increase in world exports, and we come up with a net result of 2.97mt lower ending stocks. Still a stocks to use ratio over 32% is going to weigh on the market going forward. Data attached.

Looking down into the data we see a 680kt increase in projected US exports, this comes straight off their projected ending stocks, reducing that number to 24.45mt. This number is the real problem with the market at present, we need a production problem in the US or increased demand. All the other major exporters, Argentina, Australia, Canada, the EU, Russia and Ukraine combined ending stocks total 37.14mt.

How the USDA managed to find an increase in EU wheat production from the May estimate is beyond me, but find an additional 550kt they did. They reduced Russian carry in by 1.5mt and increased Russian domestic use by 500kt, net result a 2mt reduction in carry out. Ukraine data was left unchanged, most of the trade now expect to see much than the 23mt of wheat this WASDE predicts Ukraine. Canadian data unchanged, Aussie data unchanged.

The one that makes me want to throw the report in the bin is Chinese data. Chinese opening stocks were increased 700kt, production is left unchanged at 142mt, probably 10 – 15mt more than a lot of the trade think likely. Chinese imports were left unchanged at 6mt and domestic use was left unchanged at 150mt, thus we have a month on month increase in carry out of 700kt to 124.6mt. China hold over 47% of world wheat ending stocks. Remember the great wheat steal Russia pulled off in the 70’s, maybe the Chinese have read the play book and have modified the names for 2025. Maybe I’ve got it all wrong, but at this stage I’m believing weather maps over and above this report for the time being. Yeah, yeah, the markets never wrong….. -_-

Indian production was increased 500kt, as was their consumption, net change to ending stocks was just 10kt. Most importers saw slight increases to imports and reductions to ending stocks. Nigerian imports were increased 700kt to 6.2mt, I think I have a rich uncle there that may help me move grain.