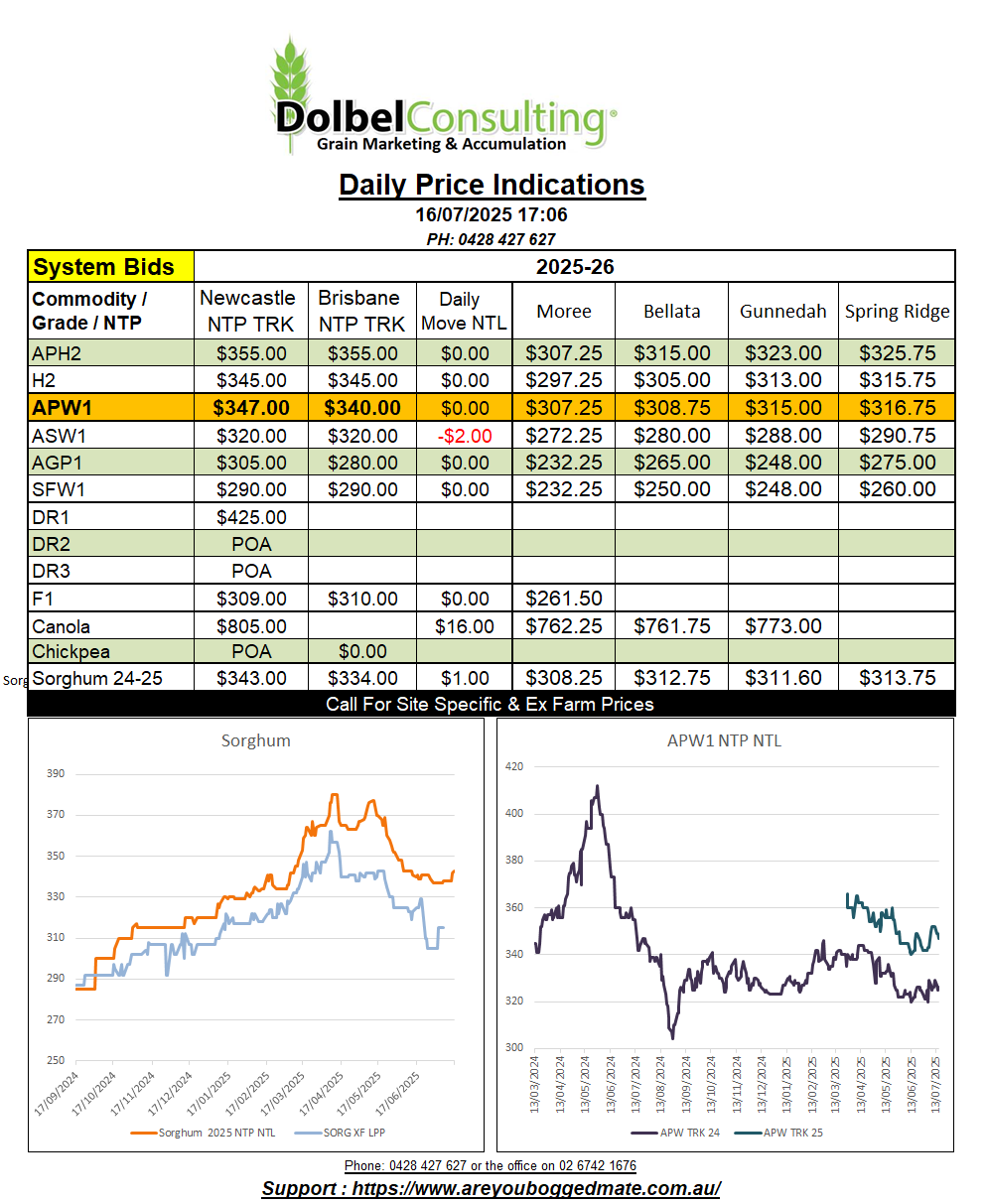

16/7/25 Prices

Bangladesh saw offers ranging between US$268.90 and US$288 CiF for the supply of 50kt of 12.5% milling wheat. On the back of an envelope this is roughly equivalent to about AUD$308 to AUD$338 ex farm LPP. Currently we see this grade of milling wheat bid at AUD$315 to AUD$320 XF LPP.

This could be indicating that the grade supplied may be the correct protein, but may well have a few other issues that have allowed the purchase price to be a little lower than current levels.

Looking at FOB values, say for Russian wheat of a similar quality. It also indicates that Russia would need to see values closer to US$288 to complete the sale. US HRWW out of the PNW would come in somewhere around US$228 FOB to compare to the sale price of US$268.90 CiF Bangladesh. Today we see US HRWW out of the PNW prices closer to US$224 FOB.

Algeria was said to have picked up just over 1mt of wheat in their latest tender for 50kt. This isn’t unusual for Algeria to do but 1mt in one hit is a big buy. Algeria do not make their purchase details public. Both price and quantity is speculative and is generally determined by the trade and made public through unofficial reports. Reports on price are harder to find but should come to light in the short term.

Paris milling wheat futures rallied on the news, up €3.00 in the September slot and +€1.50 in the Dec slot. US futures and cash markets were not so influenced. The flow of fund money and harvest pressure still the major hurdle to ag prices there.

Canola and chickpea values are the two big movers overnight. So far this week Delhi chickpeas have put on roughly AUD$37.60 / tonne. There are a lot of different reports coming out of India regarding 2024-25 chickpea production. Some suggesting a supply deficit of as much as 2.5mt, good news for Australia.