28/8/25 Prices

Canadian durum values were sharply lower overnight. PDQ reports the average farm gate price out of SE Saskatchewan fell by CAD$21.55 / tonne yesterday, closing the day bid at CAD$283.79 / tonne for a December lift. It’s hard to be accurate when converting the SE Sask durum number to a relevant number here as different buyers have different freight, insurance and operating costs. Roughly on the back of an envelope, using Italy as an export partner, the latest Canadian number would convert to something close to AUD$410 delivered Newcastle port. The current numbers out of the SE of France would support a slightly higher number Newcastle port equivalent, but both locations did see overnight losses.

Durum wasn’t the only Canadian grain hit hard, spring wheat, canola and yellow peas were all lower by the close of business. The sharp move lower in harvest values is yet another kick in the guts to the Canadian producer. The season has been tough, going from very dry to too wet for many. Later sown crops are yielding a little better than expected but the quality has been affected by the late rain. Now the market decides to discount the freshly harvested durum anyway.

The move lower in Canadian durum values comes at a time when we are seeing EU durum imports at roughly 8% above the 3 year average for this period in time of their marketing year. Although early in the marketing year reporting period, demand from Europe has been robust. Grain trading 101, buy low, sell high.

PDQ also report a sharp decline in spring wheat values across SE Saskatchewan, 1CWRS13.5 spring wheat shed CAD$6.25/t to close the day bid at CAD$242.13 / tonne ex farm. Canola from the same area was back CAD$5.33/tonne. Even with these overnight reductions being taken into account, Canadian spring wheat is still more expensive than Australian APH2 wheat CiF Japan. USA and Canadian spring wheat values are very similar FOB PNW.

You need to look pretty hard to find some grain numbers in international grain futures from last night, Paris rapeseed is one of the few, up €5.25/t for Feb slot.

There’s not a lot of joy in this mornings markets. The AUD is slightly higher and the majority of both international cash and futures markets for most grains are lower. Paris rapeseed has a day to day change in the converted price of roughly +AUD$7.71 / tonne, pleasant to see some upside somewhere, but the rest are generally lower.

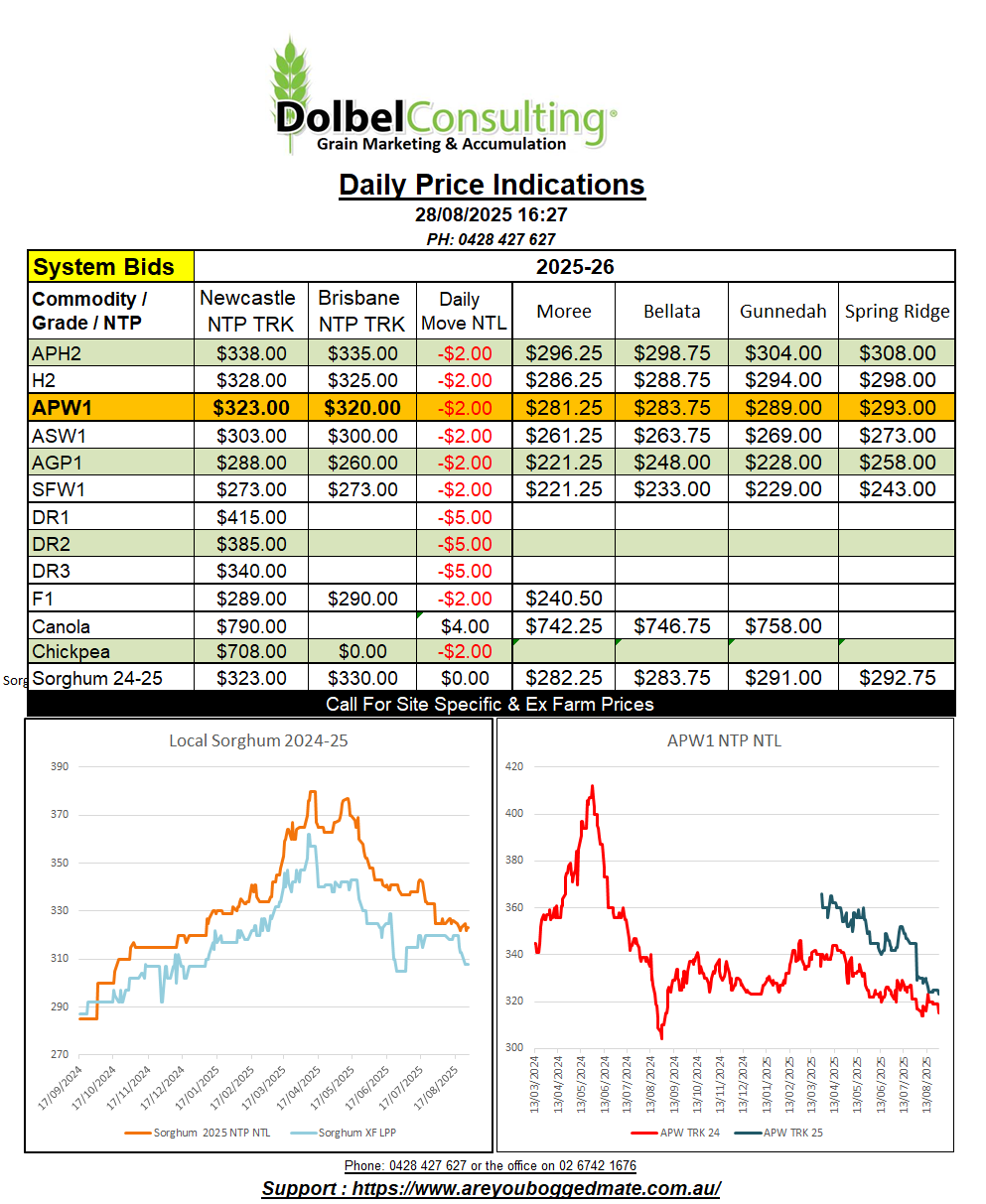

As mentioned above, Canadian durum values were smashed. Local new crop durum bids were back $10.00 here yesterday, DR1 bid at $420 NTP Newcastle. Perhaps the same buyer as the one who ran the market lower in Canada, perhaps not, but there are not 100’s to choose from these days.

With both wheat futures and cash markets lower it will be hard to talk local values higher today. There was also some basis erosion to Chicago SRWW futures yesterday. I can imagine that with this kind of negativity permeating from the international markets today, that regardless of the direction of the AUD, we are probably more likely to see further wheat basis erosion today than any firming in basis. This may exacerbate moves lower. The average world cash price did not slip as much day to day as the Chicago market though, this may offer some assistance.

On the back of an envelope we can compare local new crop H2 values to US HRWW values out of the Pacific Northwest into the Asian market. US HRWW is currently roughly US$10.00 / tonne below Aussie H2 values. This isn’t a hurdle to great to jump considering the milling characteristics of both wheat’s and may be what helps our basis in the longer term. Aussie prime hard wheat versus US and Canadian premium wheat into the Asian market, is also competing very well considering the poor new crop spreads to APH here. Local APH wheat is pretty much on par with N.American values into Asia.