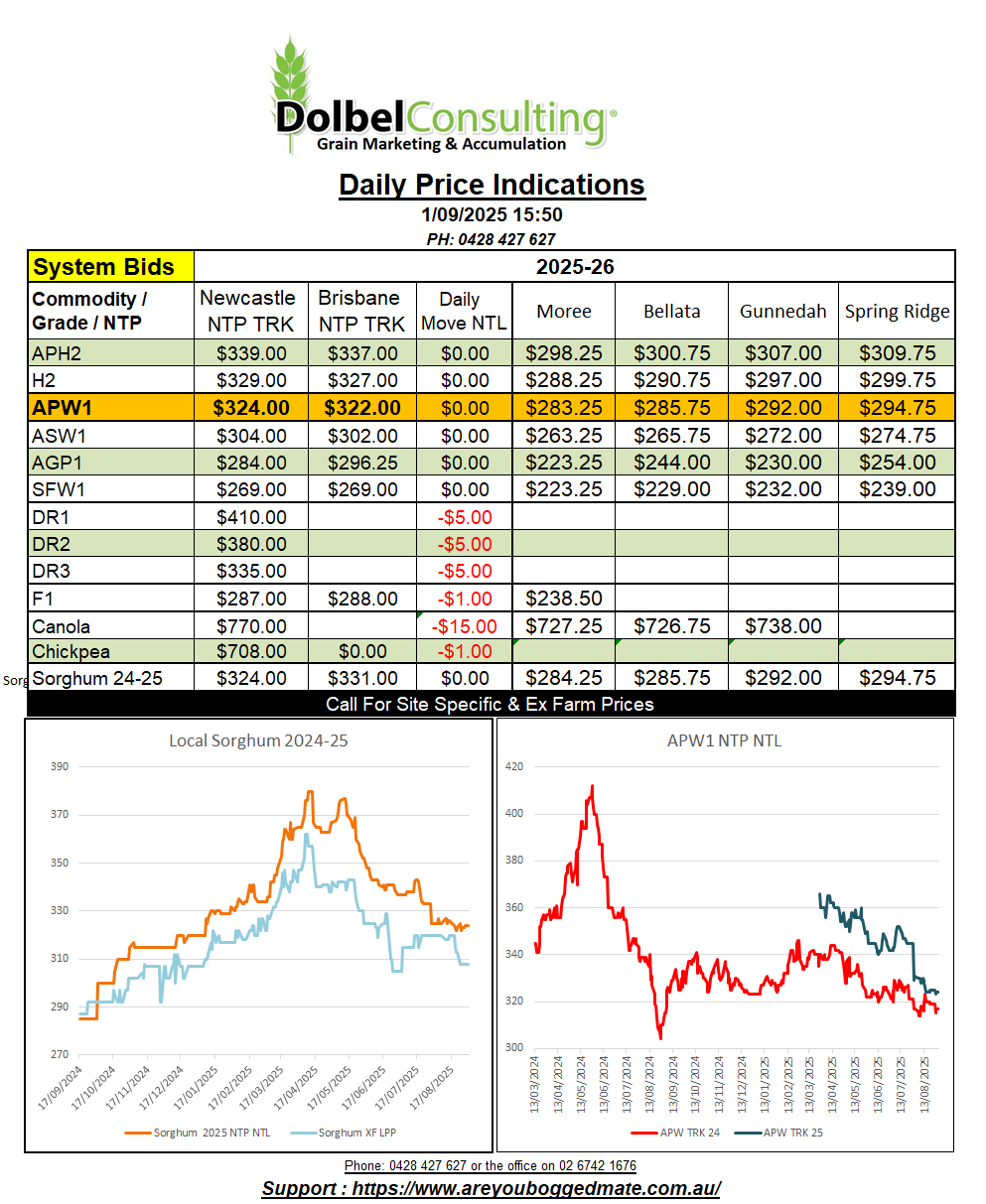

1/9/25 Prices

International cash values for canola were hit again last night. The canola market continues to be very volatile, the introduction of heavy tariffs on Canadian canola into China continues to change international dynamics. Canadian canola is already cheap, cheaper than either Ukraine or Australian canola into Europe. Australian canola is the cheapest option for the Chinese if they are going to tax Canadian product out of contention.

In 2024 China imported 5.9mt of Canadian canola. In 2023-24 Australia exported 4.4mt, and is expected to export 5.1mt in 2024-25. With Aussie production falling slightly year on year, from 6.24mt to 5.97mt, Aussie exports are expected to be very similar year on year.

This does emphasis the Aussie demand capability of China. If China was to replace all of their last seasons demand for Canadian canola than it would absorb most of Australia’s export capability. Potentially swapping our exports to Europe with Canada and their exports to China with us. From a global S&D perspective it may net little as a fundamental driver. BUT if Australia continues to service their European customers, who appear happy to pay a premium for the Australian product over the Canadian product, it may mean than China needs to increase bids to acquire the volume of canola they need to replace from Canada. Australian “traders” really are in the box seat here, and if they do the right thing by Australian producers canola may well stay in favour over the longer term.

Overnight international canola and rapeseed values moved lower. Northern hemisphere harvest pressuring cash and futures. Paris rapeseed futures closed €3.25/tonne lower in the Feb slot and Winnipeg canola futures closed CAD$9.90/tonne lower in the January slot. Cash bids across SE Saskatchewan were also lower, back CAD$10.35/tonne for a December lift. Outside markets may have weighed on the oilseed complex, Malaysian palm oil futures -1.55%, falling roughly AUD$23.16/tonne. All these markets moved against the flow in Chicago soybean futures which closed 5.75c/bu (AUD$3.22/t) higher in the Jan slot.

International cash wheat values were generally higher in native currency but on average the stronger AUD is likely to counter any upside.

Local new crop wheat markets were mixed, higher grades on the track generally tending a dollar or two higher while lower grades on the track and delivered trended a dollar or four lower.

The lack of demand from the consumer is a key feature to the local market at present. With another good season around the corner, the consumer sees little need to rush to the market as long as prices are low and showing little resilience. The combination of low world wheat prices and talk of US interest rates moving lower, also add a feeling to the market that these values may be here for a while.

If the RBA do not move in step with the US FED, the AUD has a real chance of improving against the USD. The only thing that may hold it back is the punters desire to use the AUD as a Yuan proxy. Continued trade disputes with the US and the linking of the Yuan to the USD may counter this desire though.

Canola remains volatile, Canadian values especially. Canadian canola lands CnF Europe at something close to US$542. At current new crop values NTP Newcastle track canola would land in Europe at something close to US$586. Last year Australian canola pulled a premium to Canadian canola of roughly the same gap we are seeing between the above values, US$40 +/-. Currently we see FOB values for French canola at roughly US$559 Rouen. Ukraine canola is currently more expensive into Europe than Australia canola, roughly US$604 CnF French port. By road Ukraine canola may be a different yarn, not sure how good the border controls would be. Into China Australian canola is roughly US$60 more expensive than Canadian canola out of Vancouver, and US$47 cheaper than Ukraine canola CnF China. The Chinese don’t want Canadian canola and if our trials go OK Aussie canola should replace it. Will ISCC, vanish?