12/9/25 Prices

There were some major corrections in Black Sea wheat values over the last 24-48 hours, downwards. Russian and Ukraine values had been holding on much better than US values, keeping a healthy premium, up until the last couple of session. Day to day changes in Black Sea values are exacerbated by the increasing AUD today. Using Asia as a consumption point we take Black Sea wheat values CnF Asia, and then take that value back to an AUD price here and we see the day to day variation in that number change by as much as -AUD$25.00 for Ukraine milling wheat over the last 48 hours.

The big question is how does the new price stack up against Aussie and US milling wheat into Asia. The Aussie product remains roughly US$9.00 over the US HRWW value. The Ukraine value is roughly US$25 above the Aussie value and Russian milling wheat into Asia is roughly US$13 over the Aussie price. So for now Aussie and US wheat work best for our major consumers.

The big issue this morning for the Australian exporter is the jump in the AUD, or the decline in the USD. However you want to put it, it is hurting the conversions this morning. The move in the AUD is worth about -4c/bu. Dec SRWW futures at Chicago only moved +6.5c/bu. That doesn’t leave much of a move higher to be reflected locally. The housing affordability crisis in Australia continues to drive local inflation higher, smoke and mirrors baby, smoke and mirrors. Combine the Aussie data with the worse than expected US data and bang, 70c AUD here we come….. maybe…. who knows.

US wheat futures saw technical trade ahead of the WASDE report. The market was capped by poorer than expected weekly wheat export sales data. Are the consumers expecting already low prices to drift lower ??? Year on year US wheat sales are ahead of last year, a slight lull isn’t the end of the world.

Egypt picked up 240kt of Black Sea wheat, the bulk from Russia the balance from Romania.

euters reports that China has approved imports of sorghum from Brazil over the next 12 months. The Brazilian sorghum window is very similar to the Australian window. Sowing in Oct / Nov / Dec for the early crop and out as far as March for the later crop. Something like comparing NSW to CQ. Harvest is from April / May through to late July / August for the later crop. Around 65% of the Brazilian crop is grown in eastern Goias and western Minas Gerais. Brazil producers around 4.5mt to 5.0mt of sorghum pa almost all of which is consumed locally (see attached graphic).

The reality of Brazilian / Chinese business being done will, as it does with most importers, depend on the price. Getting cash price data from somewhere like Brazil is not easy, but most reports seem to be pointing at local prices there being comparable to Argentine values. If this is the case then Brazilian sorghum would be close to Argentine sorghum values CnF China as execution and freight costs will be very similar. If this is the case then at current values Australian sorghum would be roughly US$18.00 cheaper than importing Brazilian sorghum for the Chinese. Being a member of BRICS may give Brazil some type of “preferential business” or at least offer China and alternative to the US or Australian sorghum.

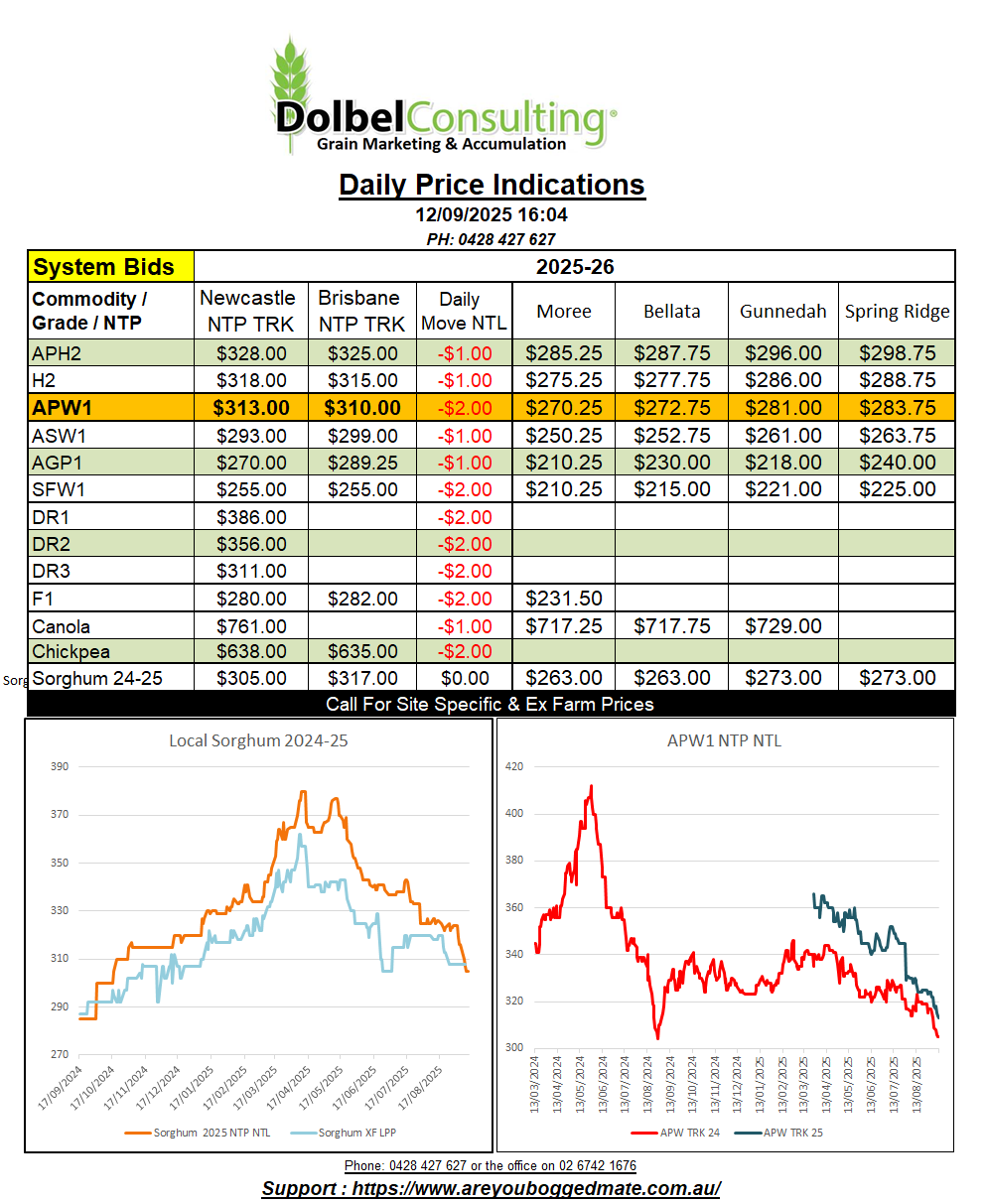

New crop sorghum values here were steady at $333 delivered Newcastle port for April / May 2026, roughly $293/t XF C-LPP equivalent. International values were generally a little firmer last night but the slight move higher in port of origin currency was countered by the increase in the value of the AUD. The net result was a slight decline in AUD/t of the conversion of international values on a day to day comparison.

The China / Brazil move could be considered bearish but the fact is that until we see business being executed from Brazil to China the news is simply a piece of paper. The most difficult part of this is that the Brazilian marketing window will coincide with the Aussie window.