15/9/25 Prices

It’s September USDA World Ag Supply and Demand Estimates day. Was it a case of sell the rumour / buy the facts, you might say so. The wheat data wasn’t bullish, but was generally what most had expected to see. Looking at the data the big picture is 3.98mt more ending stocks, mostly thanks to a large 9.3mt increase in world production to 816.2mt, that’s a lot of wheat. World usage was increased, low prices are good for that, so the ending stocks number could have been worse I guess.

Looking through the data we see increases in production for Russia, from 83.5mt to 85.0mt. Now more in line with most private estimates that have been accepted by the trade for over a month now. Russian exports were reduced 1mt to 45mt, their sales pace has been slow of late. Russian ending stocks increased from 9.39mt to 11.19mt, up 1.8mt, that’s 45% of the total world ending stocks increase.

The EU saw production increased 1.85mt, but saw imports reduced and domestic demand increased, the net result for the EU was a 820kt decrease in carry.

Ukraine production was increased 1mt to 23mt, the increase getting dumped straight onto ending stocks. This number is a little harder to swallow than the Russian increase but shows that 2.85mt, 72%, of the 3.98mt increase in ending stocks resides with Russia and Ukraine.

Canadian wheat production was increased by 1mt, beginning stocks were increased by 470kt and exports were increased by 600kt, the net result and increase of 870kt in carry out. Am I sceptical of the Canadian production number, a little, but yields have been a bit better then expected in the dry spots so I’m thinking if anything the Canadian number might be pushing it.

Australian production was increased 3.5mt to 34.5mt, fair enough. Domestic demand was increased 500kt and exports were increased 2mt to 27mt, exports I can swallow but domestic demand, not sure on that one, we do have an increasing number of mouths to feed, although poppadom’s are made from pulse flour (I’m kidding ok). 3.55mt of the 3.98mt ending stocks increase is in the major exporters, not ideal. SE Asian imports were increased 1mt to 31.7mt.

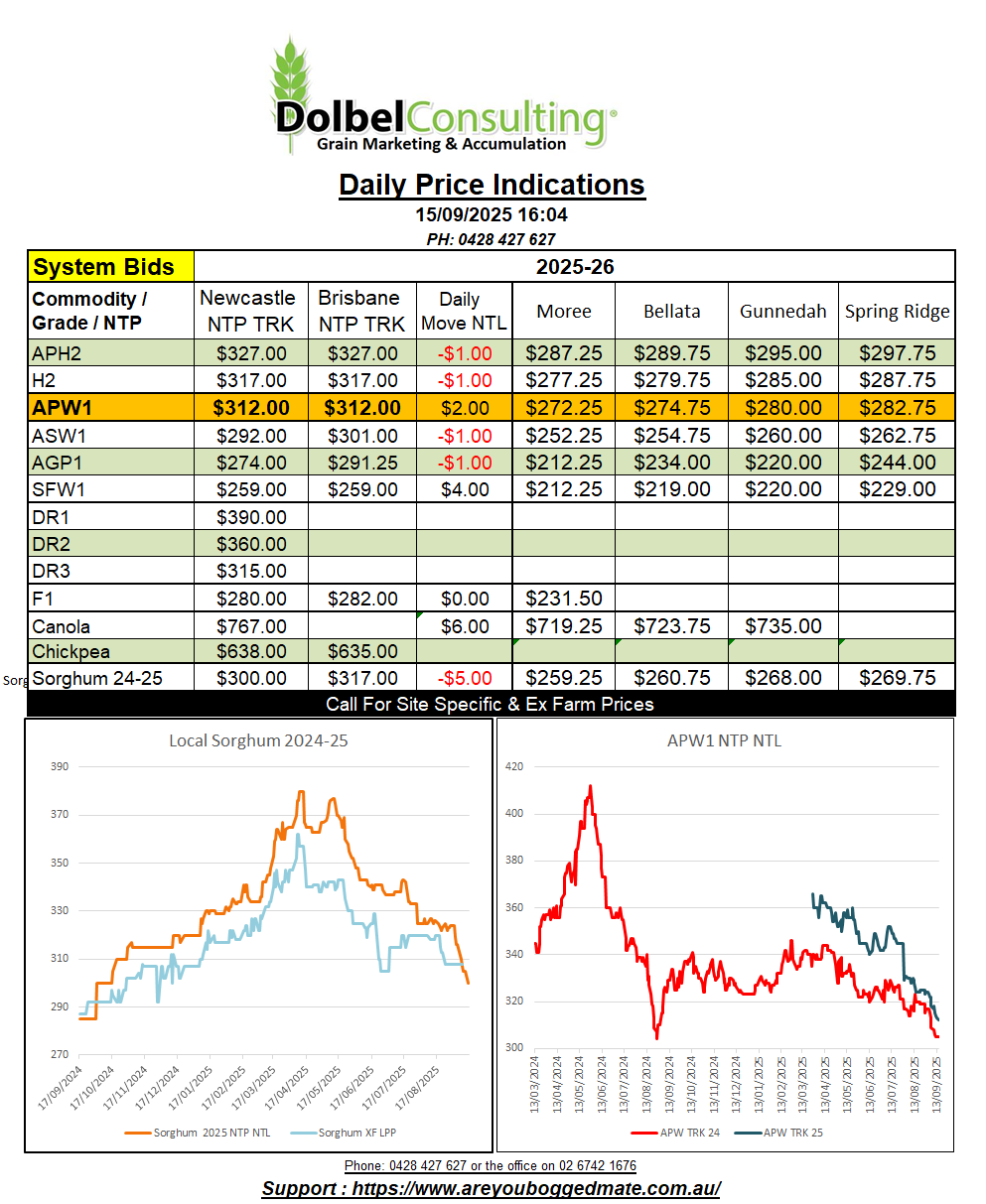

There’s not a lot to work with from a domestic perspective. There are a few producers kicking themselves in regards to not selling canola or chickpeas a couple of months ago. Retrospective analysis is a mugs game, don’t do it. Yes learn from it, but you made or didn’t make a decision at the time for specific reasons. Situations and analysis change, beating yourself up over past marketing decisions is one way of making yourself make the wrong decision in the future.

For those that got it right, i.e. selling sorghum a couple of months ago and not sooner or later, well done. The fact I’m dead quiet at present is a good sign that most managed to get close to the top for sorghum this year. It may be different next year, but currently you should be happy.

In regards to new crop marketing, forward contracting has its risks, from both a price and production perspective. Some producers sleep better at night without compounding those risks, some don’t mind, know what works for you. Just keep in mind a marketing season isn’t a 2 or 3 month window, it can be as wide as you, or your bank, will allow, but usually 4-6 months either side of the harvest window is where you will see the opportunities.

Know the trends, the northern hemisphere usually sets a low during harvest. This may mean an increase in our local basis to US futures during their harvest. It may also mean that prices here, regardless of basis, may also be a bit crappy during their harvest. The Aussie wheat crop is made in Sept / October, and the grade is made in November / December. Buyers take delivery during and shortly after harvest. Q1 the following year is often soft. The local S&D will be known and we can use arbitrage values from SE QLD, NNSW and CW NSW to start to determine local consumer prices, depending on grade. In years of plenty, the opportunities are less, as we’ve seen this year. The cost of carry being worn by the owner, not a year to pay silo’s off. There’s a long way to go before harvest but with world ending stocks not a hell of lot different to last year we might be looking at a very sideways, currency influenced, period ahead.