16/9/25 Prices

The AUD continued to creep higher overnight, topping out at 66.73 US cents before slipping a little into the close. The AUD is higher against most of our major trading partners bar the pound, and is only a smidge higher against the Euro. The strength in the AUD is more to do with weakness in the USD. There is actually some underlying pressure on the AUD coming from poor Chinese Industrial Production and Retail data that was overlooked last night.

The main thing driving the punters is the prediction of a US rates cut. Unless this does not come to be, or the punters think the RBA will meet the US cut with a similar cut here, than we may continue to see the AUD rise a little more in the short to mid term. A portion of this will be revealed on Wednesday US time.

Technically one could argue that last night’s move may have overcooked the AUD a little, but possibly not enough to warrant a full blown technical correction.

International cash wheat values were mixed, generally either side of unchanged, no big moves one way or the other. This left the AUD to do all the work and it failed to do any lifting, left the broom in the corner and knocked off early for a pie and stubby. Looking at yesterday’s conversions and comparing them to this mornings conversions, we see most international milling wheat values are down AUD$1.50 to AUD$3.00 / tonne.

US wheat futures saw a lesser move, the Dec SRWW contract conversion shedding less than a dollar a tonne.

US winter wheat sowing is progressing just a tad slower than the 13% average. At 11% sown it’s not an issue, but it came in a little lower than trade expectations. US spring wheat is 94% harvested and US corn is 7% harvested. The G/E rating for US corn fell 1pt to 67%, still 2pts better than this time last year. US weekly wheat export inspections came in ahead of even the highest end of trade estimates prior to the release of the data. At 755kt it also exceeded last weeks export inspection number of 429kt, and puts the US export loadings at roughly 12% ahead of this time last year.

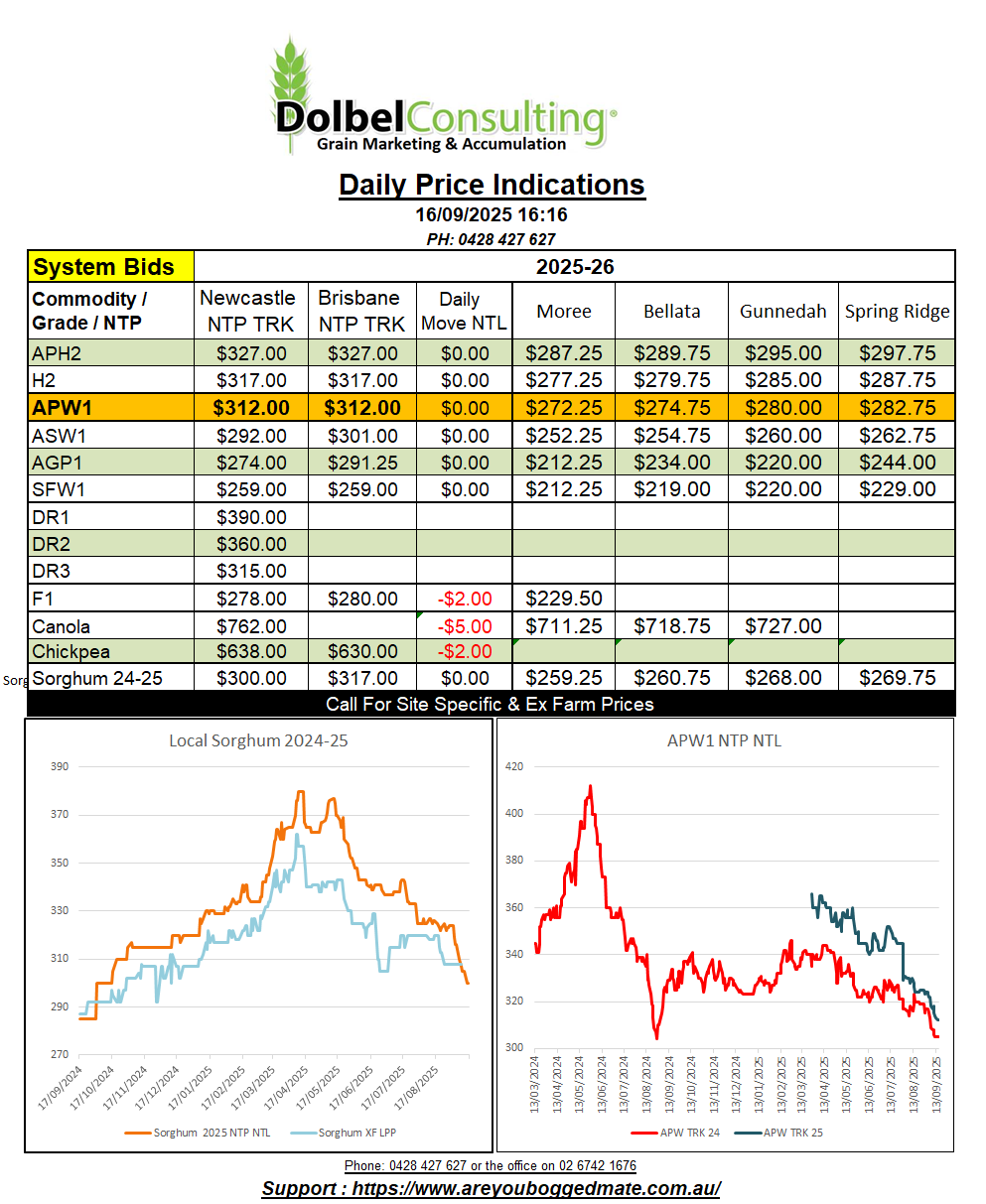

Local markets remained quiet apart from some SFW1 slots into the local feed market. SFW1 into Tamworth for September was bid at $315 delivered while Caroona feed lot shorts through the trade found buying interest at $313 delivered September.

New crop SFW1 remains unbid through the major merchants into the LPP end user market. Most buyers bidding fixed grade ASW at $292 to $300 for the delivered Nov / Dec / Jan / Feb slot.

New crop canola was a touch higher, not tracking the overseas market dollar for dollar but firmer by $6.00/t on the track. International conversions for both Paris rapeseed futures and Winnipeg canola futures are lower this morning. Combine this negativity with a stronger AUD and we have a good chance of handing back a slice of that $6.00 or possibly a bit more.

Old crop sorghum found no support, most merchants have completed their trading in old crop sorghum and are happy to leave what’s left to the box market. New crop sorghum on the track was down $2.00/t to $313 NTP Newcastle, $286 delivered Graincorp Werris Creek. The delivered Newcastle port market, while not being officially bid was indicated unchanged from Friday at $333 delivered April / May. Roughly $293 XF LPP but did not attract the attention of the farmer sellers at this level. International values were a little softer overnight. FOB US values were flat while most other indicators slipped. The USA continue to have a 10% tariff on Chinese imports of sorghum, thus CnF China US values are roughly US$278 +/-. On the back of an envelope that’s comparable to a price XF LPP of something close to AUD$311. Better than current local bids but irrelevant if there are no Chinese bids supporting that number.