17/9/25 Prices

The AUD continued to push higher against the US dollar overnight, hitting a session high of 66.87 late, after some volatility early in the session. The US FED will meet tonight to announce if, or when, or not, they will increase, decrease, or hold steady, the official US interest rate. The punters are backing a 25pt reduction, hence the strength in the AUD as US and Aussie rates are expected to start to converge. The market anticipates, and to some degree has priced in 3 US rate cuts over the balance of the year. A failure of the US FED to deliver these cuts could be quiet interesting.

The currency punters could be torn between risk on, bullish the AUD, or risk off, bearish the AUD. The risk on scenario greatly depends on exports, thus good data from our major trade partners like China and probably China and the Chinese market too, did I mention that we need to see good Chinese data to sustain a rally in the AUD. It appears that some punters have overlooked the need for this as the interest rates between the USA and Australia became the main focus. This makes one wonder if this will be a buy the rumour / sell the fact session tonight.

As the USD falls against some of the majors it is making US exports a little more attractive, hence we are seeing some strength in US grains. US wheat, corn and soybeans all enjoyed some upside. Strength in US grains rolled across outside markets, encouraging prices higher for both Canada and the EU. This may trigger further purchases by major importers in the short term.

The corn rally has been hard to fathom of late. The US is expected to harvest a huge 425mt corn crop. I remember when they broke 300mt for the first time, that was considered a massive crop at the time. The crux appears to be a combination of the weaker US of late but more so the corn stocks to use ratio is expected to be the lowest its been since 2013-14. This has a lot to do with the changes in consumption since the last time S:U was this low, the use of corn in ethanol production globally. Moves higher for both Paris rapeseed futures and Winnipeg canola futures should roll across new crop oilseeds here today.

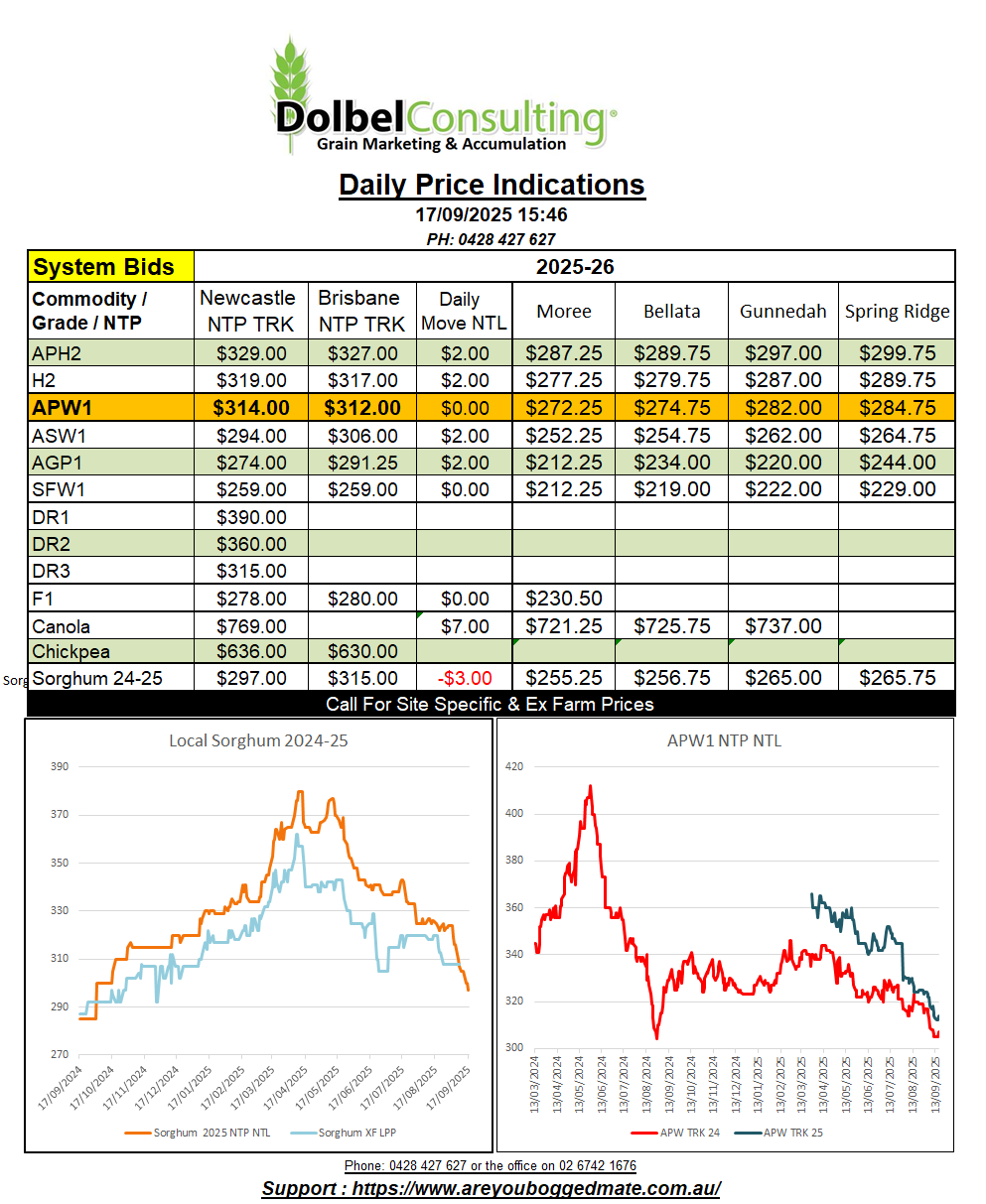

Local markets were dead quiet yesterday, just a few clean ups and some new crop inquiry on segs.

Graincorp advise me that Emerald Hill will be set up to cater for roughly 20kt of durum and 15kt of canola, Gunnedah will be wheat only, Boggabri will be barley and maybe some wheat, Curlewis will be all canola, Premer will be canola and wheat, Spring Ridge will be durum and wheat, Willow Tree wheat only and Quirindi is back with barley. Werris Creek will have all the major grades as per usual.

There is currently no allocation for chickpeas and faba beans to be stored by Graincorp on the LPP.

With most international grain values higher overnight, the major hurdle today will be eroding wheat basis and the AUD.