18/9/25 Prices

Profit taking dominated the US futures markets last night after a higher close the previous session. Momentum continues to be a thing of the past with commodity futures up one day down the next, wheat futures slowly grinding lower. The Dec SRWW contract is still above the contract low set back on the 5th of September, but at 528c/bu it’s nothing to write home about, unless your a mill owner in Asia telling everyone how cheap you can buy US wheat for. And buying they are.

Overnight cash values out of the US Pacific Northwest were flat to lower, HRWW shedding roughly AUD$2.16/t compared to yesterday’s conversion. White wheat fared a little better, slightly improving, up AUD$1.76, while US spring wheat was up by less than a dollar.

Winnipeg canola futures, and cash canola bids out of SE Saskatchewan, were both lower. A Dec lift ex farm SE Sask slipped roughly CAD$13.37/tonne. On the back of an envelope, comparing Canadian and Aussie canola CnF France we see Aussie canola at current values is some US$70 more expensive than Canadian canola. Nice local basis here which may be pr-empting some Chinese business.

Comparing Aussie canola and Canadian canola into the Chinese market, for the sake of the exercise only. We see current Aussie bids indicate a CnF China price difference of something close to +US$85 / tonne. Great to see tariffs at work. Well this time it is anyway, the barley debacle didn’t serve the local industry here very well. Current local acre estimates for feed barley may well indicate that local growers here on the plains at least never got over it, acres here the lowest they have been in years.

Delhi chickpeas shed more value but are still priced higher than the Minimum Support Price. At 5992 Rs/Q Delhi market vs the MSP at 5650Rs/Q ex farm, a premium of roughly AUD$58/t, one would really need to confirm the “costs to market” to say that local Indian values are not actually below the MSP at the farm gate. Delhi values slipped 21Rs/Q overnight. The slip in the AUD countered this, turning a slight down, into a slight up of AUD$1.27/t.

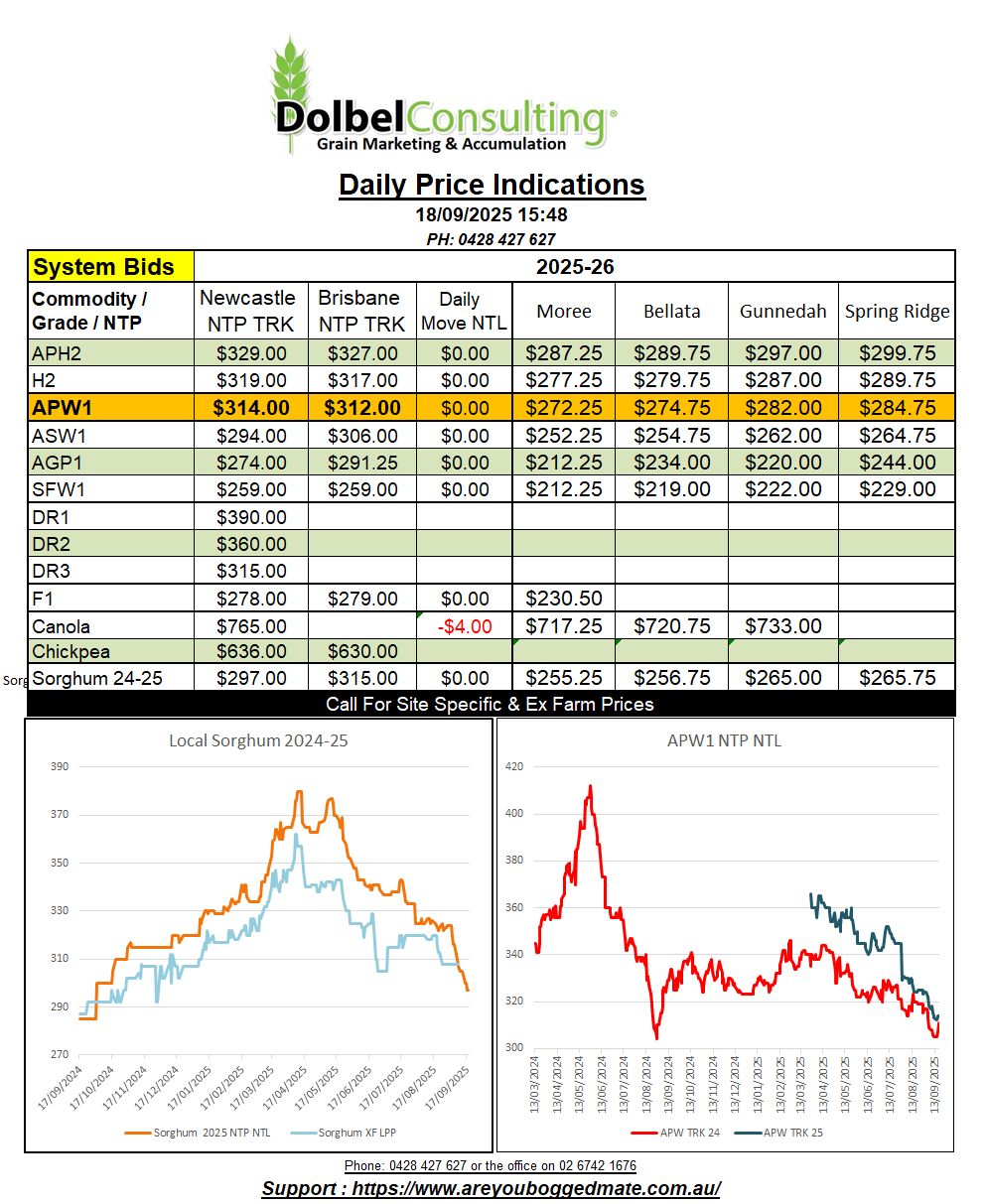

Local cash at silo APW new crop basis to ASX January APW futures is at historically mid to lower levels. At approximately +$15.00/t, at least it’s a premium. If conditions in the south had (or may still) deteriorated we may well have (or could still) seen ASX basis premium here eroded as we move towards harvest. Keep an eye on this as ASX futures are a deliverable fixed grade APW1 if need be. Not a great option but should become liquid enough at some stage to prevent needing to deliver against it before January. This may only come into play if the southern crop goes close to failing, not likely at present.

Just referring back to my rainfall model. It’s basically telling me know we should move through a slightly drier September, between 30mm & 50mm before moving into what could potentially be a very wet Oct / Nov / Dec. October has roughly a 25% chance of being drier than average, and a 75% chance of seeing 60mm+ of rain. November has a 25% chance of being drier than average, and a 75% chance seeing 60mm+ of rain. December is not showing any chance of being drier than average, and is expected to receive higher than average rainfall, the model now predicting an average of 110mm, with a high side of 185mm. This model is using historical data to predict the future. It’s not a climate model or anything fancy, but it does surprise me how accurate it has been in the past. That’s not to say it hasn’t been wrong occasionally too. It’s just interesting, so take away from this what you like.

Currently we see the only “feed” wheat option on the LPP as ASW into the local feed market, bid at $306 end user. That’s not great, and it’s not a feed wheat hedge. A track multi grade value FED1 (true feed wheat) is at………. well it not bid, buyers minimum grade on a multigrade is SFW at $222 Gcorp GDH. What year is it ??? If we do run into a “feed wheat” year, I can not see a lot of nearby marketing getting done.