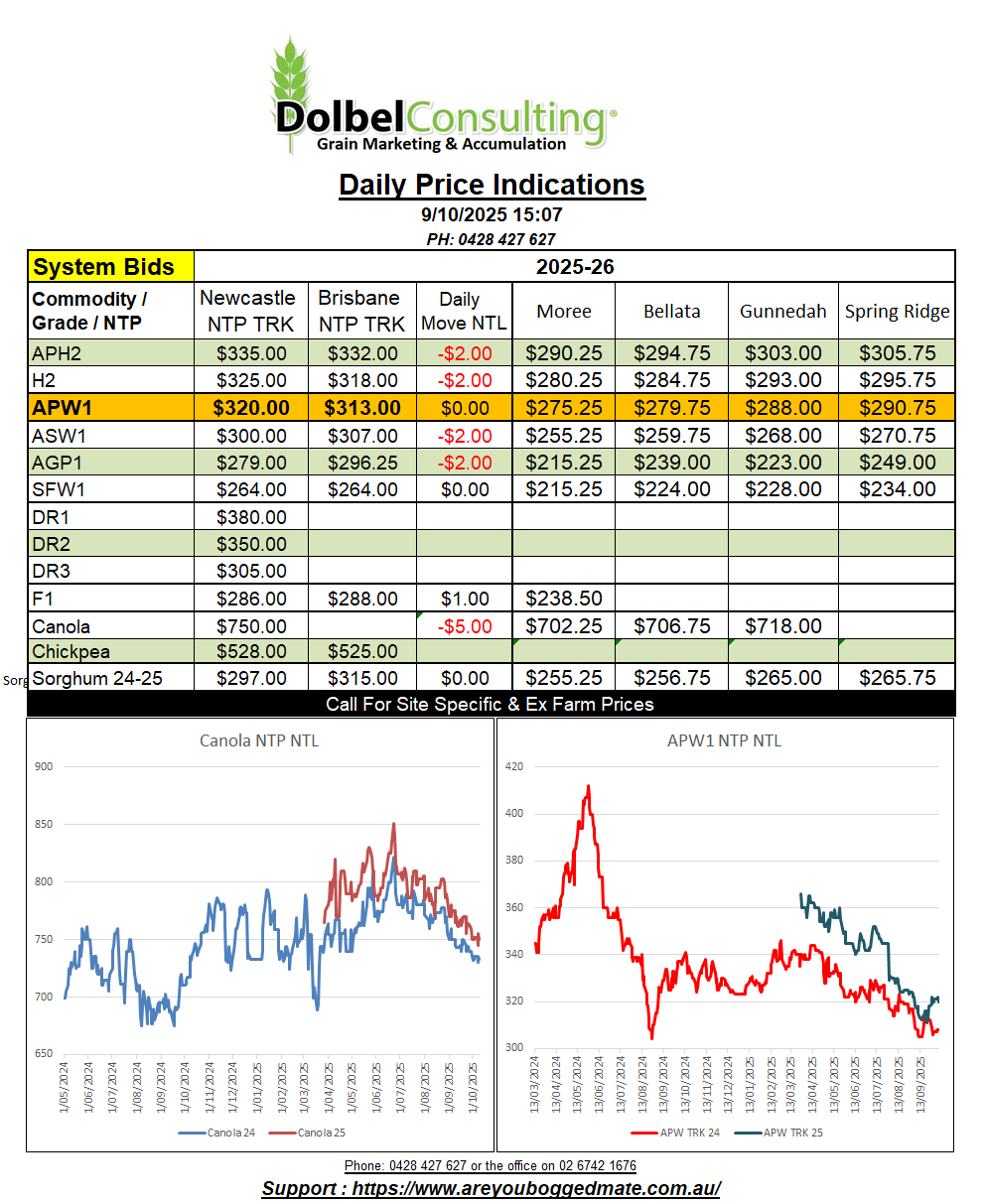

9/10/25 Prices

Trump has announced US$12 – US13 billion in aid to US farmers hurt by the trade war with China. When asked about distribution no details were given. The current US government shut down may delay the distribution of funds.

To put this into perspective, the Australian wheat crop, if valued at AUD$400 / tonne, would add up to roughly US$12.7Bn. All hail the level playing field.

Bangladesh has agreed to purchase 220kt of US wheat under a government to government trade deal which Bangladesh hope will lower trade tensions between the two. Wheat value for this “purchase” was set at US$308 per ton and will be supplied through Singapore based Agrocorp International. On the back of an envelope, a sale price of US$308 C&F would convert to an XF LPP value of something close AUD$375. There’s a lot of fat for the US in that one.

The EU continues to struggle with soft wheat exports. Current export volume is back roughly 25% year on year. Romania is the largest shipper of EU wheat to date, moving roughly 2.26mt. Black Sea values remain very competitive into the traditional EU markets. An ongoing trade disputes with traditional consumer Algeria has done nothing to help French exports.

Durum values out of the French port of La Nouvelle were lower in overnight trade. At US$313 FOB origin it works out at roughly US$338 C&F Italy, compared to Canadian product at US$336 C&F Italy. Using these C&F Italy values we can compare to local new crop bids. We may then determine that local bids are roughly AUD$20.00 lower than they could potentially be, but this depends greatly on the level of trade margin merchants wish to take.

Wheat values out of the US PNW were generally flat to lower, Black Sea values are generally flat to lower and Argentine values are flat to firmer.