20/10/25 Prices

The lack of official USDA data on a daily, weekly or monthly basis is hurting some traders more than others. The futures markets are seeing more directionless trade. From an outsiders perspective this doesn’t look entirely bad, as it does appear to be reducing volatility. Yes that’s also boring and some upward volatility at these numbers would be better, but it is giving the fundamental traders the upper hand at present.

The AUD was up 0.29% last night, negating the small move higher in US soft red winter wheat and hard red winter wheat futures at Chicago. The big mover last night was Paris rapeseed futures, down €4.50 / tonne in the Feb slot, not ideal. Comparing this mornings conversion to yesterday mornings conversion of Paris rapeseed futures this move equates to a fall of roughly AUD$12.32 / tonne.

Canadian canola can land C&F Europe for roughly US$525 / tonne. The Ukraine product is able to move into the EU market for something close to US$585 / tonne, but this could vary a lot depending on the location of the grain and the consumer. Australian canola is more closely priced into the EU market to the Ukraine product and comes in somewhere around US$590. This should be telling us that if the Canadian product is able to compete on quality, then the Aussie product may well be looking a little expensive for future business. But is this the key, the 10 year average oil content for Canadian canola is 42.6% and although the 2025 crop average oil content is not yet available, it is expected to be lower than the 10 year average.

A meeting between Chinese and Canadian officials this week saw China propose that they would reduce the current import tariff on Canadian canola as long as the Canadians reduced the import tariff on Chinese electric vehicles. Confirming what we already suspected, that the canola tariff was indeed in retaliation to the EV tariff. Ottawa showed little interest in submitting to the will of Manitoba and Saskatchewan producers and the tariff proposal was rejected. The Canadian domestic crush rate is expected to hit 12.226mt in 2025-26 up from last years 11.698mt. Around 61% of the Canadian crop will be crushed locally.

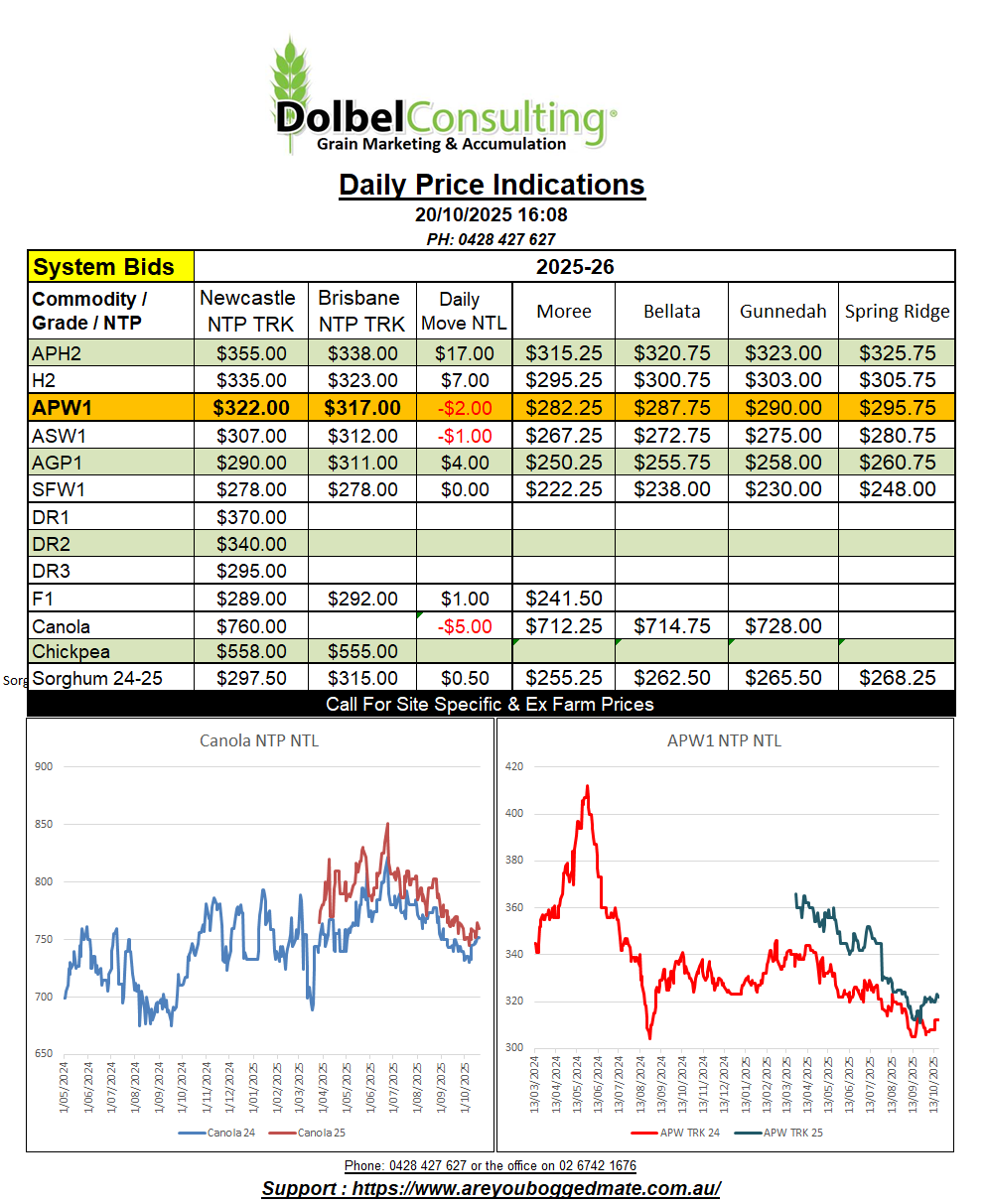

Track milling wheat was generally a couple of dollars firmer yesterday, the lower grades were up a dollar. Feed barley into the Downs consumer was unchanged at $302 while bids for BAR1 into the LPP market were mixed but generally bid firmer by many, closing the day bid at just $275 delivered consumer. And they wonder why they are having trouble buying any.

The results of the Algerian durum tender indicated that current new crop values are a little lower than they could be. This is especially true once you consider the grade of the tender. Being filled with Canadian CWAD3 isn’t indicating it’s a high quality contract. CWAD3 has a minimum vitreous of just 40%, not exactly destined to the pasta market anyway. If the weather damage for Canadian durum is as bad as some analyst are assuming, than we may see more Canadian product being sold into the less discerning markets over the mid to long term. Quality here will be crucial this year.

Local canola bids saw healthy gains yesterday, track closed the day up $12.00 per tonne and nearby crusher bids into Newcastle for October delivery were also firmer at $790 delivered. Currently the crusher market is the place to go, either O/N/D or the outer months of Feb / March, which are paying a $5.00 premium. $5.00 isn’t really a lot of carry, but it does roll the delivery program away from the harvest period. Keep in mind the maximum daily intake capacity into the Newcastle crusher is roughly 1800t, about 47 BDoubles per day, one every 10 minutes. If you think this is a good price and wish to lock a window for delivery in, contracting will be crucial. All prices are quoted as ISCC compliant, and discounts of $10 – $15 will apply to canola producers that have not signed up to the ISCC “scheme”.

Gunnedah picked up another mill or two in a storm last night taking the 24 hour total to 18mm. Falls across the Gunnedah shire ranged from as little as 3mm near Curlewis to 15mm at Carroll. Spring Ridge was light on with 0-8mm, heavier towards Breeza. South of Mullaley picked up 22mm, Boggabri 10mm, Premer less than 5mm. Moree saw 16mm, Gurley 5mm, Rowena 0-15mm. Heavy rain and large hail was reported at Gilgandra and Coona. Some parts of Gilgandra recorded 75mm of rain.

A weak trough line is located from roughly Tamworth NW towards Birdsville this morning. The trough is expected to weaken and move NE across the Downs and CQ by this evening. There’s a slight chance of a storm across the New England and Granite Belt this morning.

Low pressure will dominate the West Australian wheat belt from Sunday. A large area of low pressure will consolidate and track east across WA and into S.Aust on Tuesday morning. A low cell is expected to develop over Kangaroo Island on Tuesday night. A trough line will develop to the east of this area of low pressure, stretching from Hay to Wyndham in NE WA.

Keep an eye on this trough line as we move into Wednesday. There’s a good chance this system will create storms across much of the eastern wheat belt on Wednesday and Thursday next week. Airflow ahead of this trough is generally from the NW, so it will become hot, potentially very hot on Tuesday and Wednesday, maybe 38C. This may produce strong winds within storms as conditions cool with the passing of the trough on Wednesday night.