27/10/25 Prices

There is little change in international cash and futures values this morning. Black Sea wheat values are the weakest of the major export regions, while wheat values out of the US Pacific Northwest were generally either side of unchanged by less than a dollar.

During the week Algeria picked up roughly 600kt of milling wheat by tender. I say roughly because Algeria do not make their tender results public, so reporting is generally seen as estimates through the trade. The purchase price was said to be about US$258.50 / tonne C&F. Ports of origin is expected to be mostly from the Black Sea, Romania, Ukraine and Bulgaria getting the lions share.

Some punters thought that Argentina may also appear on the supplier list but with the delivery date penned in for November / December this might be pushing it. Argentina or Australia may potentially supply some of the December portion but unlikely.

On the back of an envelope the sale price converts to an ex farm LPP price of something close to AUD$250, not a value that would accumulate much wheat at present, or hopefully in the future.

According to Grainstats Canada the average canola oil content looks pretty good. Samples from Saskatchewan averaging around 43.5% (37.2% to 49%). Alberta comes in around 44.3% and Manitoba closer to 43%.

There’s plenty of speculation in the wheat market at present. Stories range from China is looking to buy wheat in volume, to the funds are about to liquidate their shorts. These could be true or false, but if you are a fundamental trader you would find the former unlikely and the later just slightly more plausible.

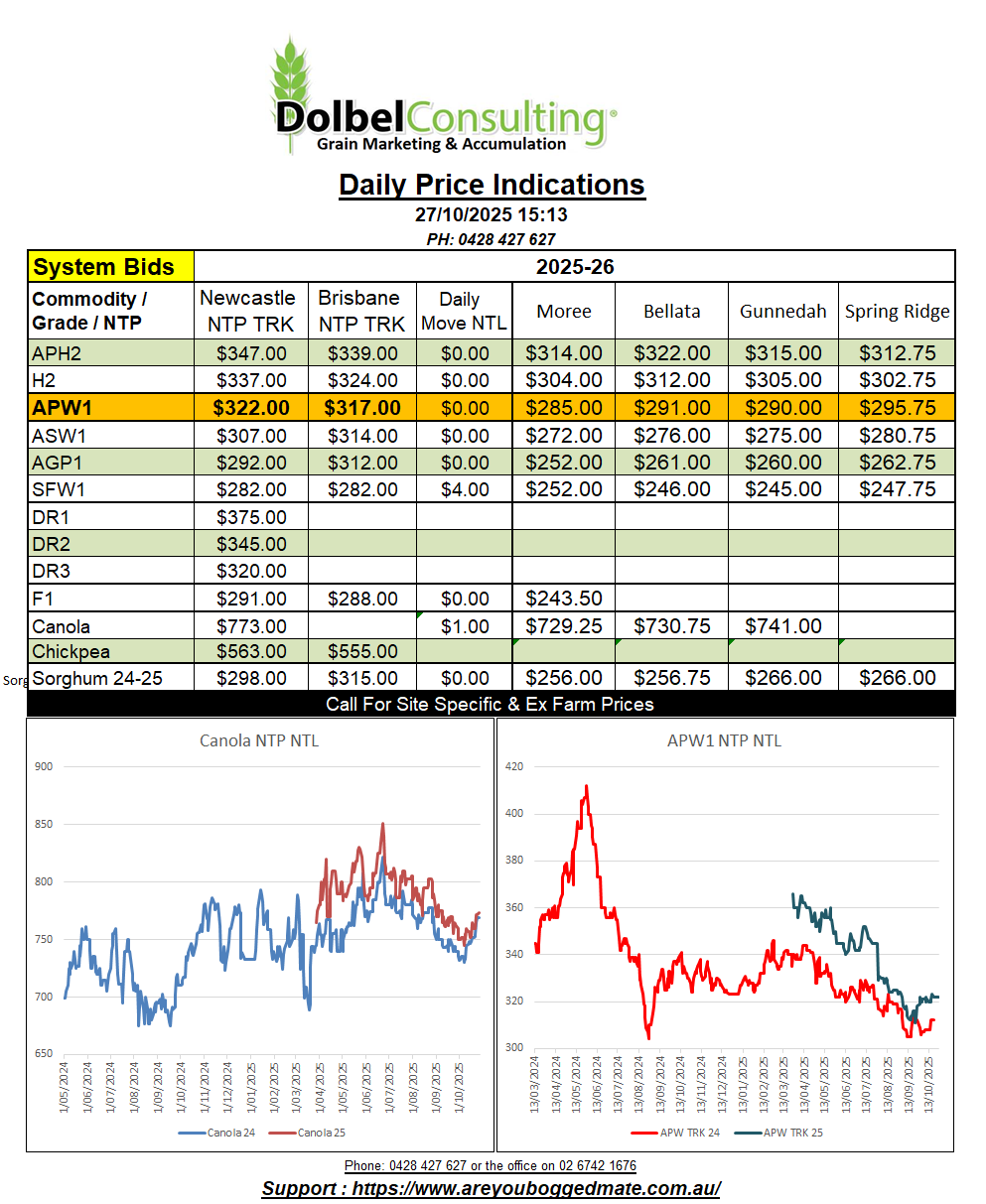

Local track wheat failed to follow the US futures market higher. Trading sideways wheat handed back a significant slice of basis, the premium it had collected above US futures values, over the last few days. The premium APW was pulling above the Dec SRWW contract had increased to +71c/bu (+AUD$40.00/t at today’s exchange rate) on Wednesday. Yesterday basis closed with the premium down to +56c/bu, or +AUD$31.60/t at this mornings AUD rate. A fall in basis of AUD$8.40/t, while cash bids here remained flat.

H2 wheat delivered Graincorp Spring Ridge is bid at $302.75/t, down from the mid week high of $307.75, but still closing a couple of bucks higher than the previous weeks close. If this wheat was to be loaded onto a truck instead of a train and road freighted to a Sydney consumer, it would set them back something close to $385 / tonne. Bids into the Newcastle port have become a little harder to find this week. The trade appear happy to push producers to either the local track or into on farm storage. Merchants are happy to wait this out, well aware that they will see good volume of ex farm stocks offered to them either at the port or ex farm in coming weeks and months.

One might assume that Brisbane values for H2 shouldn’t be too far away from a realistic value for Newcastle port. If this is the case, we see H2 into the Brisbane market bid at $352 yesterday. This would value H2 wheat at roughly US$20 above current C&F values for HRWW of a similar protein into the SE Asian market. Not an unachievable premium for white wheat over red wheat, but not something you’ll hear the trade talking about in detail.

Growers in the north were sellers of canola yesterday. The trade was reluctant to meet higher offers but there were instances where $5.00 / $10.00 above the public bid or CropConnect bid was extracted. Some buyers were trying to widen the discount for non ISCC accredited, unsuccessfully.

A large mass of cloud covers much of NSW / Victoria and South Australia this morning. The radar shows light rainfall between Tullamore, SW of Dubbo, stretching north towards Cunnamulla in the SW QLD. Heavier falls are pushing east across the York Peninsula towards the farming districts north of Adelaide.

The low cell pushing the cloud east is located in the Bight south of the WA / SA border this morning, and is tracking slowly east. The low should push into the SW coast of Victoria tomorrow morning with a barometric pressure of 990hPa, tracking slowly east to be just off the SE NSW coast late Sunday night. The bulk of the impact from this change will be felt across Victoria and the Riverina, but more so across the far SE corner and the high country on Sunday.

Airflow here ahead of the change will be generally from the NE-N, not exactly priming the inland with moisture but there’s a slight chance we’ll see a storm with the passing of the front tomorrow afternoon. Most models do tend to suggest that the NWSP will miss most of the rain from this change. There are expected to be some heavier storms across the Downs but the bulk of the rain will be across Victoria and the Riverina and SE NSW.

Airflow here will swing around a lot over the next few days ahead of a cooler change on Tuesday. The next high cell is expected to be much further south, potentially enhancing the development of a cut off low over NW NSW on Tuesday. Severe storms may develop around Coonamble, tracking NE.