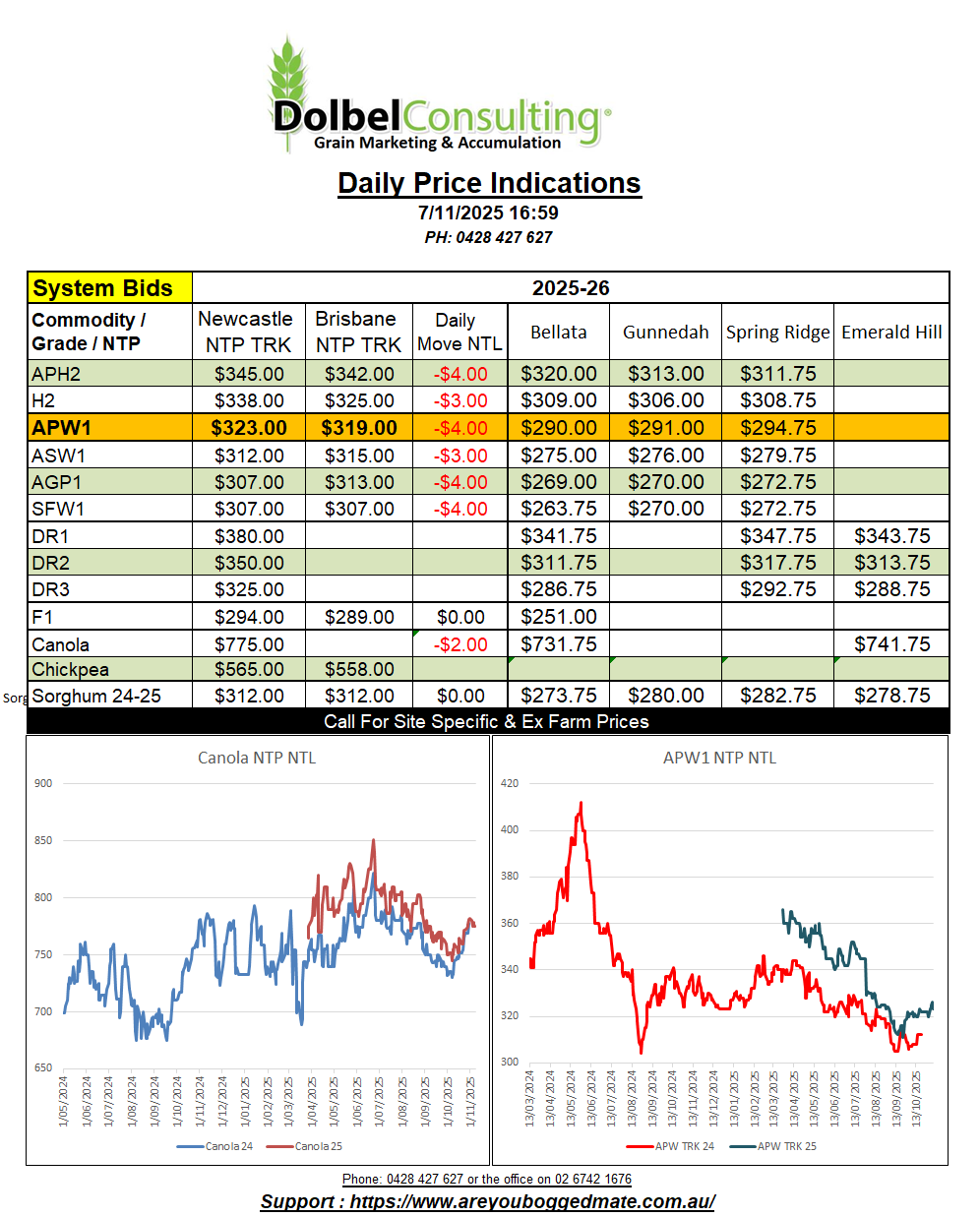

7/11/25 Prices

Some days you wonder if Stephen King, or Stephen Spielberg for that matter, is in charge of writing the script for the US futures market. Seriously, this stuff is hard to make up, and feels like it should be in a fiction section in an obscure library somewhere.

Chicago SRWW and HRWW futures, corn and soybeans all saw some downside last night. A last ditch roll for some profit taking before a proper market correction, possibly.

The wires this morning read that Chicago sold off hard after, yes after, it was confirmed China had bought 120kt of US wheat. Yes you read that right, the market fell after China bought US wheat. Two additional sales opportunities for US wheat totaling 110kt were announced, neither applying the brake to the sell off at Chicago.

China will keep a 13% import tariff on US soybeans, basically pricing US beans out of the Chinese market in the short term. The impact this had on soybean futures was obvious and the Chicago bean contract closed -26.75c/bu (AUD$15.15/t) lower in the January slot. The sell off picked up momentum spilling across corn and wheat futures at Chicago. Spring wheat futures at Minneapolis showed some degree of reality and closed the session +0.75c/bu higher in the December slot. 60kt of the Chinese purchase was said to be spring wheat.

From November 10th the Chinese will scrap the additional import duty applied to US sorghum. Reuters reports a boat load of US sorghum is already on the water heading to China. China bought 5.7mt of US sorghum last year, 66% of Chinese demand came from the USA. The remaining 3mt of Chinese imports made up from Australia and Argentina. China has stated it will however retain the 10% levy imposed on all US goods that was introduced after Trump applied duties to Chinese imports back on April 2nd 2025. The net move in real value keeps Aussie sorghum price competitive against both US and Argie sorghum.

As for wheat we have a 107c/bu wheat / corn spread at Chicago, corn is cheap, US wheat export volume would suggest wheat is cheap, does corn move higher.

It might be a good day to stick your head in the sand after having a look at US futures this morning. Buy the rumour / sell the fact was said to be the key to the sharp decline in US wheat futures. A move worth roughly -AUD$10.91/t. The possible downside in the conversion found some help from a weaker AUD, which countered roughly AUD$1.03/t of the fall.

This still leaves plenty of downside potential for local traders wishing to talk the market lower on the back of US futures. This may ruffle a few feathers though. For those that follow basis, the gap between cash and futures, you would have witnessed a collapse in Newcastle APW to Chicago SRWW basis over the last couple of weeks. Yesterday that basis hit not only a short term low of +21c/bu FOB to Dec futures at Chicago, +21c/bu basis is also the worse basis we’ve seen against the December contract since mid June.

The flat nature of the Aussie market as opposed to the jump in values of the US market had eroded the premium that Aussie wheat was achieving over US wheat. If we were to follow the US market lower today, instead of re-establishing that premium it would simply be discounting the value of Aussie wheat, not trying to extract, and pass on, the premium Aussie wheat deserves.

I’m not convinced we’ll see +40c/bu basis this afternoon with cash prices remaining unchanged from yesterday, but I’d also like to think we’ll see basis much stronger than it was yesterday.

International wheat values were not as sharply lower on average as the US futures market might suggest, but US PNW HRWW values were down roughly -AUD$8.86/t, compared to yesterdays conversion and US white wheat out of the PNW was down -AUD$4.41/t in the day to day conversion comparison.

The BOM synoptic chart shows the low cell pushing across southern Victoria throughout the day. The front associated with this low cell is expected to move across the far west of NSW this morning and across the Riverina today. Here in the north we may not see the change move through until the early hours of Saturday morning.

With airflow ahead of the change generally from the NE-NW we may see some storms develop across the NWSP as the trough passes tomorrow morning and lingers to our east into the evening.

The ECMWF model shows a good chance of a storm developing from about 3.00pm this afternoon. Storms are expected to become active west of the Newell from 2.00pm or 3.00pm before pushing east across the SW of the LPP from 3.00pm or 4.00pm. The ECMWF model predicts the more severe storms to track from Coonamble NE towards Burren Junction, possible becoming severe around sunset, producing falls of 15-30mm around Merah North. This storm is likely to continue to track NE towards Moree, staying west of the Newell but also losing momentum as the heat goes out of the day.

Storms across the LPP as less likely this evening but more likely tomorrow morning. Storms are expected to be more active across the top of the plains and towards the NE around Manilla and Tamworth in the morning. Showers may become more general across the plains as the day progresses and winds move more to the W-SW in the afternoon before clearing to the NE early in the evening. Saturday may see it take all day to record 3 or 4 mills on the LPP, possibly some heavier falls under storms. Next week looks to be mostly dry.