1/12/25 Prices

US grain futures were mixed, corn and soybean futures at Chicago found a little upside while wheat was generally lower by less the AUD$1.50/t. Paris milling wheat was back across all months, December slipping €1.75 / tonne, and March back €2.75 / tonne. London feed wheat was also lower, shedding £1.65/t in the Jan > May slots.

Paris rapeseed futures were unchanged in both the Feb and May slots, and a tad weaker outside those contracts. Winnipeg canola saw minimal losses, cash canola out of SE Saskatchewan was back CAD$0.55/t for a December lift.

International cash wheat values were mixed, no strong lead from US markets. Black Sea values were just over a dollar lower, most of that being generated by the stronger AUD more so than any slippage in FOB values out of Russia. Cash rapeseed FOB Rouen did slip more than the futures side of the European market, back AUD$4.53/t compared to yesterday’s conversion.

The Argentine wheat crop just keeps getting bigger. The Buenos Aires Grain Exchange increased production by 1.5mt to 25.5mt in their latest estimate. Argentina was due for break, and 2025-26 appears to be delivering one. Harvest is progressing well with around 34% of the crop already in the silo. A little slower than last year but nothing to be concerned about. A quick look at Worldagweather.com shows it hasn’t all been plain sailing though with much of the major wheat producing districts seeing 50-100mm of rain over the last 30 days, a lot of that fell in the last 2 weeks, on a ripe wheat crop. Production may yet be determined by test weight, early days. The Argie forecast calls for more of the same, the 7 days model predicting 15-30mm across the major wheat region. Storms may also produce much heavier falls across central Santa Fe late next week.

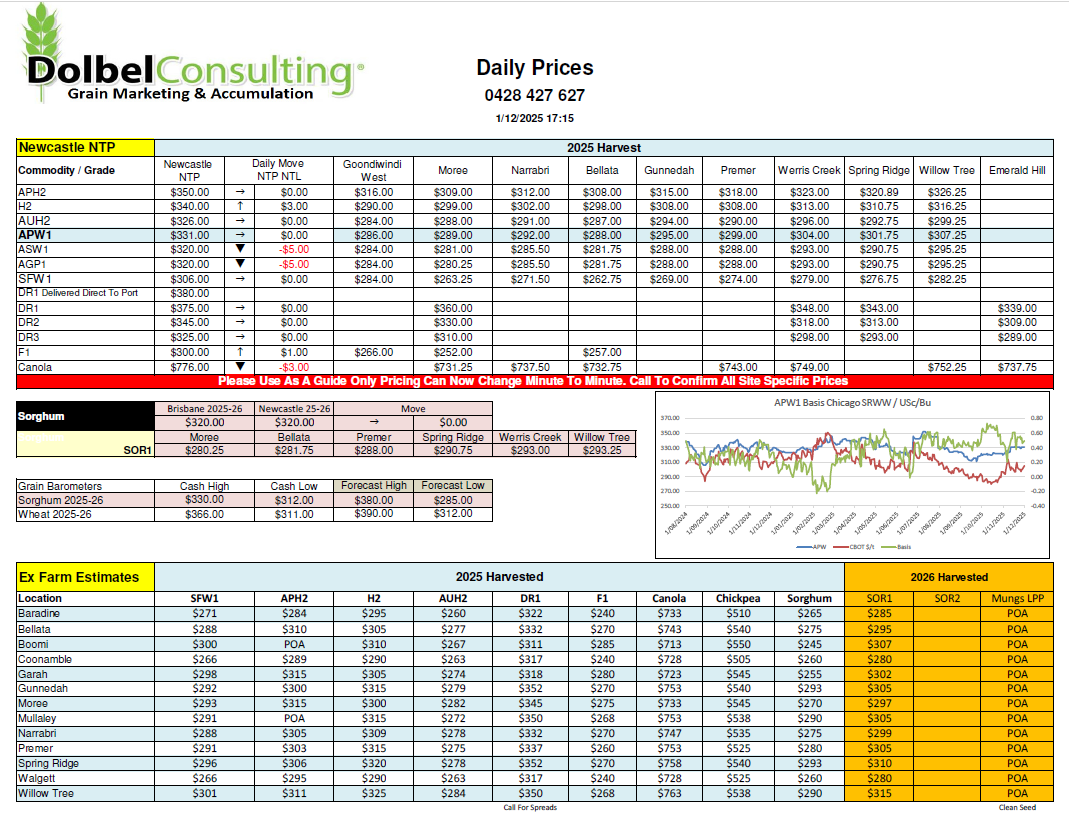

Trade inquiery was limited to the delivered feed markets and, believe it or not, new crop sorghum yesterday. The grower showing little interest in offering either at current values.

New crop sorghum at $350 delivered NAT Newcastle was probably the pick, if I had to sell something. The Argie and US numbers into China are giving us a floor of just under $300 ex farm equivalent, and a cap of about $330 ex farm equivalent.

If China was to remove the 10% import tariff on US sorghum, that cap could fall $20.00 in a hurry though. Is that likely to happen between now and sorghum harvest, you would have to say the odds are against it.

Milling wheat into the port had limited interest. H2 was bid at $360 delivered fist half December. There wasn’t a public bid for APH direct to Newcastle port yesterday, but there was a bid of $390 for APH into the Brisbane port. For budgeting, bench marking, or blending purposes one should be safe to use the Brissy number as a substitute for the Newcastle number for Dec / Jan / Feb.

SFW1 was sort by the trade into the LPP end user market and the Newcastle end user market, bid $336 Newcastle and $315 LPP. ASW was bid at $320 delivered Liverpool Plains end user against an offer to sell of $325, neither buyer nor seller moving on that parcel.

DR1 found a bid of $380 delivered Newcastle port, there were no solid offers to sell at a higher number to test the durum market. Looking at both French and Canadian durum, one comes to the conclusion that local prices may have $20.00 upside in them. The chance of jumping the market $20.00 in one offer is probably remote, but that’s where I’d be starting and persisting at if I was a seller of DR1.

Showers show up on the radar both to our south and to our north this morning. Showers are heavier across the central tablelands and are more active as storms north of Moree.

The showers are building along a trough line associated with a low cell exiting the NSW SE coast this morning. A 996hPa the far SE of the state may experience some serious storm activity with the passing of the system. Here across the NWSP the trough should push through around lunch time, the heavier falls accompanying the passing.

Another low cell is expected to push NE out of the Southern Ocean and across Bass Straight tomorrow, not a great weekend for Victorian farmers with showers across much of the state today through to Tuesday.

The second low is expected to consolidate east of Bass Straight on Monday before deteriorating as it moves east into the Tasman on Tuesday.

A high off the SW coast of WA will move moist SW airflow into Western Victoria feeding the back of the second low cell. This high cell is relatively slow moving and will become the dominant feature of our weather here in the eastern states from Monday. Airflow will initialy be from the SW on Monday and Tuesday morning, turning more SE late Tuesday. Days will be a little cooler next week, Monday a windy 29C and Tuesday 26C. The chance of rain next week is very remote.