22/12/25 Prices

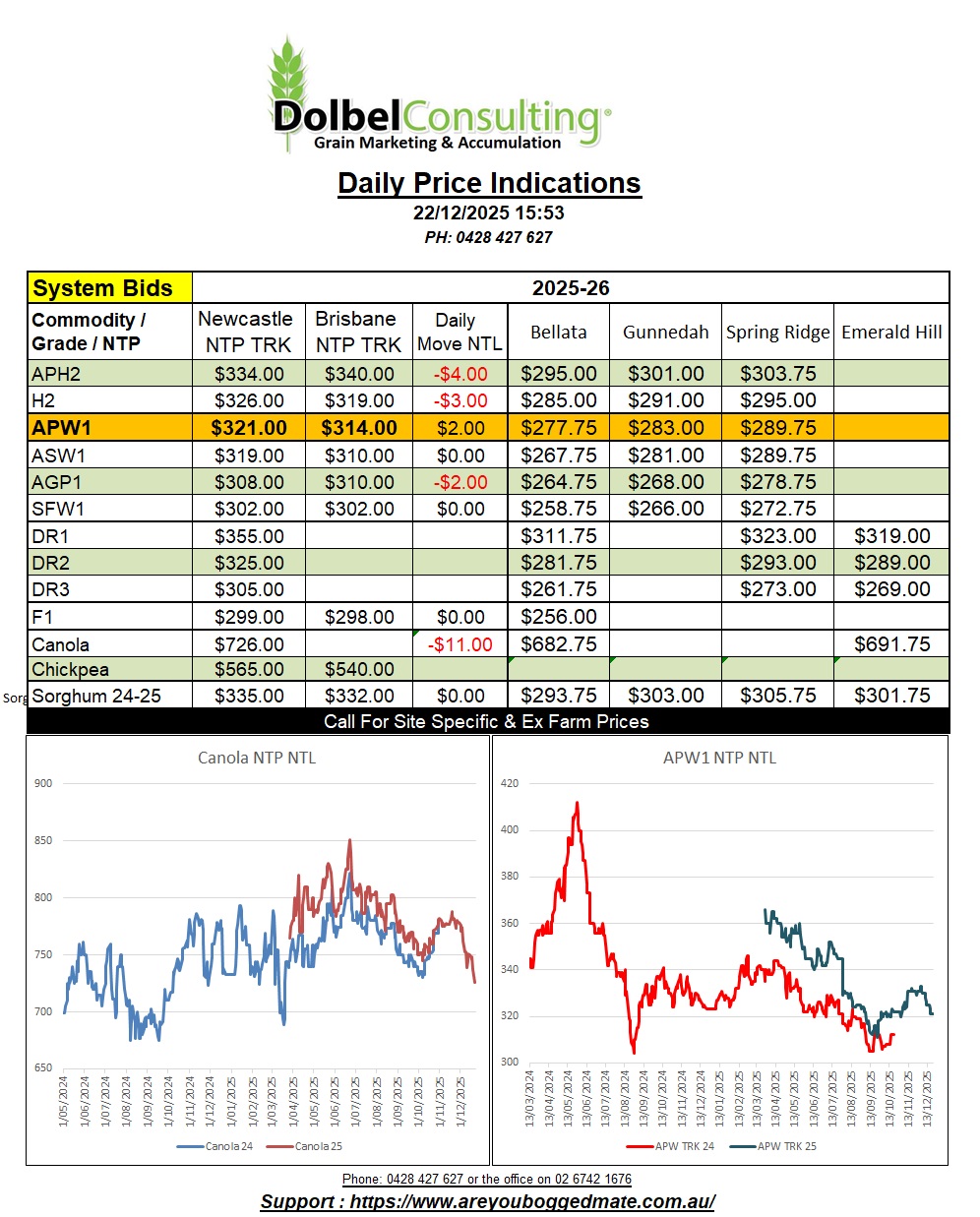

Canola doesn’t appear to be able to take a trick lately. Both Winnipeg canola futures and Paris rapeseed futures saw sharply lower markets again last night. For Paris rapeseed this takes the decline in the February 2026 contract to -€21.50/t since this time last week. At today’s exchange rate with the Euro that’s equivalent to just over -AUD$38.00/t. The outer month contracts were also weaker, the Nov 2026 slot falling €13.25/tonne. Weakness is coming from multiple directions. Higher 2025 production estimates for Australia and Canada. The thought that China will not meet their commitment to purchase 12mt of US soybeans. Crude oil, and softer palm oil. Overnight palm oil futures fell roughly AUD$27.82/t in the March 2026 slot.

The weakness isn’t restricted to the futures market. Canadian cash values out of SE Saskatchewan also softened this week, closing CAD$6.96/tonne lower for a Feb 2026 lift last night. This accumulates to a decline of CAD$37.38/t XF SE Sask since December 11th.

Values into the EU have also fallen. FOB France indicated at roughly US$532 last night, Canadian product C&F France is closer to US$511. Canada continues to try and sell canola after losing access to the Chinese market. For example Australian canola is valued at something like US$580 C&F China, while current Canadian values would indicate they would be closer to US$478 C&F China if it wasn’t for the tariffs. I don’t mind seeing this, it’s just another example of how tariffs often hurt the consumer applying the tariff more than the seller the tariff is applied to. I remember that when China applied tariffs to Aussie barley it simply meant they paid a heap more for barley in the long term.

Looking forward we see canola futures at Paris lower in value for new crop months versus nearby. Canola not only has the nearby issues hurting values, it may also see convergence with lower new crop values as we move through Q1-2 in 2026. This tends to put a lot of hope on a major production issue in the northern hemisphere, if we are to see even a remotely better value for new crop canola here, come harvest 2026.

Alternative crops to winter cereals are starting to struggle. To date we do not see any Indian import tariffs on chickpeas, and faba beans are worth just $300.