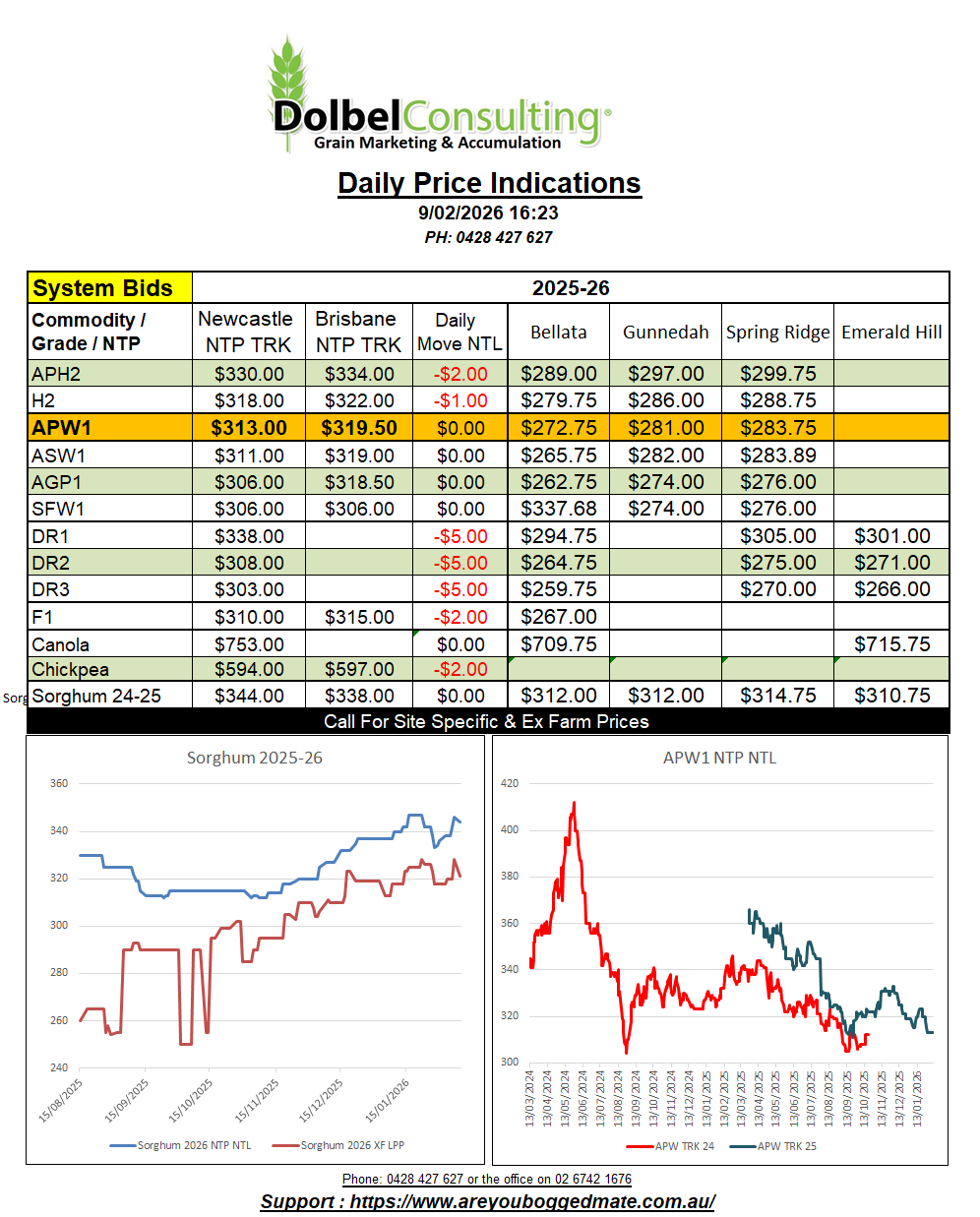

9/2/26 Prices

Algeria was said to have picked up 200-250kt of feed barley this week at values ranging from US$268 to US$270 CiF. On the back of an envelope this would equate to something close to AUD$240 XF LPP. With local bids closer to AUD$305 XF LPP, it’s pretty safe to assume this isn’t going to get filled with east coast barley any time soon. Russian barley would work at these number, as would a few other Black Sea sellers. French barley may struggle, potentially coming in around US$10.00 above the sale numbers.

The Russian number would suggest a C&F China number close to US$294. The sale value converts back to a much higher FOB Russia number than what we are seeing as a public indicator. Possibly around US$246, public numbers had been closer to US$200 to US$210. I’m not 100% sure on what the insurance value is. One might assume insurance would be closer to US$10.00 than US$30.00 though. Currently we see Aussie C&F China values somewhere around US$257. Does this indicate we should sow fence to fence barley in 2026………. not at all.

Negative pressure on US wheat futures came from increased year on year Canadian wheat stocks and slower than expected US weekly export sales. There’s also additional pressure on wheat values being converted from USD/t to AUD/t from the stronger AUD this morning. Hard red winter wheat out of the Pacific Northwest, when compared to yesterdays conversion, is back roughly AUD$6.31/t. Widening the gap between local H2 and US HRWW into the Asian market to more than US$15.00/t, depending on location.

Chicago soybeans had a breather after some solid gains this week. Nearby futures closed higher by 3c/bu (+AUD$1.57/t). This did encourage a higher close for Paris rapeseed futures, but the firmer dollar more than negated the move. Compared to yesterday’s conversion, this mornings conversion is roughly AUD$1.34/t lower. Canadian values were lower, XF SE Sask down about CAD$1.82/t. Palm oil shed AUD$20.20/t. WTI crude oil was steady, +19c/b.